That gap between intention and preparation is where deals die.

This guide walks through every critical phase of selling your business: knowing when to sell, getting an accurate valuation, cleaning up your financials and operations, assembling the right team, and planning for life after the close.

TLDR

- Start preparing 12–24 months before your target exit. Waiting until you've decided to sell costs you negotiating leverage and valuation points.

- Valuation gaps between buyers and sellers exceed 10% in most failed transactions — know your number before going to market

- Clean financials, documented operations, and reduced owner dependency are what buyers scrutinize hardest

- A qualified business broker is not optional — they protect your valuation, maintain confidentiality, and keep deal momentum from stalling

- Tax and liquidity planning should begin before the deal closes, not after

When Is the Right Time to Sell Your Business?

Internal vs. External Triggers

Owners sell for two categories of reasons. Internal triggers include retirement, burnout, health issues, partnership disputes, and succession needs. IBBA/M&A Source data from Q3 2023 confirms retirement is the top reason across all sectors, with burnout running second in the lower middle market.

External triggers matter just as much: Favorable credit markets, industry consolidation, or a sector running at peak valuations can all create ideal exit windows. Owners who wait for perfect alignment on both dimensions often wait too long.

The Exit Planning Institute estimates that roughly 50% of business exits are involuntary — triggered by death, disability, divorce, or circumstances the owner never anticipated. Waiting for the right moment assumes you'll have one.

Sell From Strength, Not Necessity

Buyers pay premium multiples when revenue and EBITDA are trending upward. A business showing consistent growth commands more competitive buyer interest and better deal terms than one showing a plateau or decline. Once performance peaks and starts softening, your negotiating leverage goes with it.

The faster a company is growing, the more valuable it is to an acquirer. Many owners inadvertently suppress that growth by becoming too conservative as the business matures, which erodes value before they ever go to market.

The Personal Alignment Question

Financial readiness gets most of the attention, but personal readiness is just as likely to derail a deal. Before starting any sale process, answer this honestly: what does your life look like after the sale?

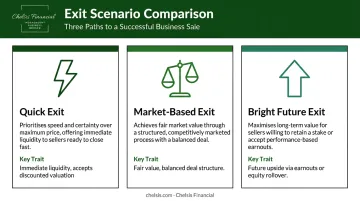

Owners who haven't worked through that question are far more likely to stall negotiations, second-guess decisions, or back out entirely. Buyers sense that ambiguity quickly. Chelsis Financial's framework for this involves identifying which exit scenario fits your situation:

- Quick Exit : prioritize immediate liquidity, accept a discounted valuation

- Market-Based Exit : seek fair value with a balanced deal structure

- Bright Future Exit : participate in future upside via earnouts or equity rollover

Getting clarity here before engaging the market saves months of friction.

Know Your Number: Getting a Business Valuation

Why Guessing Is Expensive

Most owners either overvalue their business based on emotional attachment or undervalue it by ignoring goodwill and growth potential. Neither mistake is neutral. A 2025 summary of Pepperdine's Private Capital Markets Report found that roughly 31% of M&A engagements ended without a transaction — and valuation gaps were responsible for 26% of those failures. Of those gaps, 84% were 11% to 30% wide.

That's a wide miss — and a preventable one.

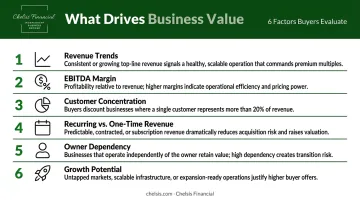

What Drives Business Value

Buyers use EBITDA multiples as their primary benchmark. Two businesses with identical revenue can have very different valuations based on:

- Revenue trends — growing vs. flat vs. declining

- EBITDA margin — how much profit the revenue actually produces

- Customer concentration — no single customer should exceed 10–15% of revenue

- Recurring vs. one-time revenue — predictable cash flow commands a premium

- Owner dependency — the less the business needs you, the more it's worth

- Growth potential — buyers pay for what they believe the business can become

For context on current market benchmarks, GF Data reported in H1 2025 that businesses with $1M–$5M EBITDA averaged 5.5x while the $10M–$25M range commanded 6.2x to 6.7x.

Understanding Adjusted EBITDA and Add-Backs

Raw EBITDA rarely reflects a business's true earning power. In owner-operated businesses, adjusted EBITDA can differ from reported EBITDA by 30% to 50% or more, according to CLA.

Add-backs are legitimate adjustments that normalize earnings for a buyer. Common examples:

- Owner salary above fair market rate for the role

- Personal expenses run through the business (vehicle, travel, insurance)

- One-time legal costs or non-recurring events

- Family member compensation above market

A simple example: if a business shows $400K net income but the owner takes a $300K salary for a role worth $150K on the open market, the adjusted EBITDA is $150K higher than reported — and the valuation changes accordingly.

Those adjustments are why understanding your number before going to market matters.

The Professional Valuation as a Diagnostic Tool

A professional valuation done before going to market is more than a price tag. It identifies gaps you can close, sets realistic expectations, and gives you confidence walking into buyer conversations.

Chelsis Financial offers a Complimentary Assessment of Value: a starting point that examines financial performance, market trends, and industry benchmarks to give owners an honest, defensible number before committing to any timeline or process.

Getting Your Financials and Operations Sale-Ready

Organize Your Financial Records

Buyers and their advisors will request at least three years of financial statements. The quality of those records directly affects buyer confidence and deal velocity.

There's a meaningful spectrum here:

| Financial Statement Type | Buyer Confidence Level |

|---|---|

| Internally prepared | Low — subject to scrutiny |

| CPA-reviewed | Moderate — reasonable for most deals |

| Audited | High — reduces friction significantly |

Beyond the format, two issues consistently create problems:

Cash-basis bookkeeping is a red flag. Buyers want accrual-based financials — revenue recognized when earned, not when received — because it makes your business comparable to industry benchmarks. If you're on cash basis, prepare GAAP-adjusted financials for the trailing three years.

Commingled personal and business expenses create messy adjustments during due diligence. Separate them now. As Chelsis Financial puts it directly: if your P&L and tax return diverge meaningfully, expect scrutiny and delays.

Sell-side Quality of Earnings (QofE) analysis is worth serious consideration for deals above $1M in transaction value. Commissioning a QofE before going to market — typically costing $20,000–$75,000 over three to six weeks — helps sellers identify and resolve financial issues proactively. When buyers discover problems themselves, the result is usually price renegotiation or deal collapse.

Clean financials get buyers to the table. What keeps them there — and protects your valuation — is how well the business runs without you.

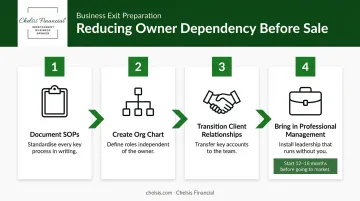

Reduce Owner Dependency Before You List

Buyers apply what's informally called the "hit by a bus" test: if the business struggles without the current owner, perceived risk increases and valuation decreases.

The fix requires deliberate preparation:

- Document Standard Operating Procedures (SOPs) for all critical functions

- Create an organizational chart with clearly defined roles and responsibilities

- Transition client relationships from the owner to other team members

- Bring in professional management — ideally at least 12–18 months before going to market

Chelsis Financial has seen owners who started this process five years out, transitioning from active operator to absentee owner, and added substantial value as a result. The goal is simple: make your absence an event the business can handle, not a crisis.

The sooner you start, the more options you have — both in timing the sale and in commanding a stronger price.

Legal and Structural Cleanup Before Going to Market

Legal issues discovered during due diligence are among the most common deal-killers. Finding and resolving them in advance is far less costly than losing a transaction over them.

Contract Review Priorities

- Check customer contracts for change-of-control clauses that let clients exit after a sale; ensure successor language survives ownership changes

- Confirm vendor and supplier agreements transfer automatically or identify which ones require advance consent

- Verify commercial lease assignability and clarify the landlord's position on an ownership change

- Document and confirm enforceability of non-competes, compensation arrangements, and key-person agreements

Intellectual Property

Trademarks, domain names, proprietary processes, and software must be formally owned by the business — not the individual founder. IP created by employees should be covered by written assignment agreements. Also confirm that all business licenses, permits, and regulatory certifications are current and transferable to a new owner.

Ownership Structure

Minority shareholders, silent partners, and informal equity arrangements create legal uncertainty that delays or kills deals. Complicated cap tables should be resolved, or at minimum fully documented, before a buyer's attorneys start reviewing. The cleaner the ownership picture, the faster a deal can move.

Assembling Your Deal Team

Who Belongs on the Team

A business sale requires specialized expertise that general advisors typically don't have. The core deal team includes:

- Business broker / M&A advisor — manages the entire process, markets the business, vets buyers, leads negotiations, and protects confidentiality

- CPA / tax advisor — cleans up financials, structures the deal for maximum after-tax proceeds, and coordinates on entity-specific tax treatment

- M&A attorney — reviews LOIs and purchase agreements, identifies legal risk, and negotiates protective provisions

- Wealth manager — plans for post-sale liquidity, diversification, and tax treatment of proceeds

A general accountant or family attorney won't cut it here. These are specialized roles, and the wrong advisor at the table costs more than their fee.

According to a 2025 exit-planning summary, 78% of owners lacked a formal transition team despite many actively seeking advice on business transitions. That gap is largely why transitions fail.

Engage Your Broker Early

Bring in a business broker or M&A advisor 12–18 months before your target exit date. Advisors brought in early can stress-test your goals, identify value-building opportunities, and help you avoid the most common deal-killing mistakes.

Managing your own sale is an option — but it typically requires 10–15 hours per week on top of running the business. When owner attention shifts away from operations, business performance slips. And when performance slips mid-process, deals fall apart.

Chelsis Financial handles marketing, buyer qualification, documentation, and negotiation so sellers can keep running their business through closing.

Protecting Confidentiality

A leak can trigger employee turnover, customer anxiety, and supplier instability — all of which hurt valuation and deal momentum. Confidentiality isn't just a preference; it's a financial protection.

Professional brokers manage this through:

- Blind teasers — no identifying details shared until buyers are vetted

- NDAs required before any financial information is released

- Controlled buyer vetting — financial capability confirmed before revealing the business identity

Chelsis Financial operates on a curated buyer model — connecting sellers with financially qualified buyers rather than broadcasting listings broadly. That selectivity reduces leak risk and typically produces better deal terms.

Due Diligence, Closing, and Life After the Sale

Surviving Due Diligence

Buyers typically request:

- 3 years of financial statements and tax returns

- Customer and vendor contracts

- Lease agreements and real estate documentation

- Employee records and organizational charts

- Legal history and pending litigation

- SOPs and operational documentation

- IP ownership records

The best way to survive due diligence without renegotiation is to surface and resolve issues before the buyer finds them. Chelsis Financial notes that organized documentation signals operational maturity to buyers — and compresses the typical LOI-to-close timeline of three to six months considerably.

The Closing Sequence

Understanding the structure prevents surprises:

- Indication of Interest (IOI) — signals buyer curiosity, non-binding

- Letter of Intent (LOI) — establishes proposed terms, triggers exclusivity

- Purchase Agreement — the binding document; this is where legal review matters most

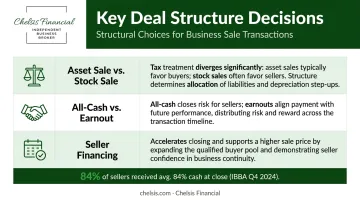

Key structural decisions that affect your net outcome:

- Asset sale vs. stock sale — asset sales are more common in the lower middle market and have significant tax implications. The IRS requires purchase price allocation among asset categories, each taxed differently

- All-cash vs. earnout — sellers who accept earnouts tied to future performance can capture higher total value but take on post-close execution risk

- Seller financing — offering to finance 10–15% of the purchase price typically accelerates closings and can support a higher overall price

IBBA/M&A Source Q4 2024 reported sellers received an average of 84% of total consideration as cash at close, with seller financing accounting for 15% or less in most deals.

Life After the Sale

Many sellers underestimate how much the transition from business owner to investor changes daily life. The financial side alone requires deliberate planning:

- Tax treatment of proceeds — structure matters; consult your CPA before the LOI, not after

- Liquidity management — compare net proceeds (after taxes, fees, and debt payoff) against lifestyle needs and wealth transfer goals

- Portfolio diversification — concentrated wealth moves from a single illiquid asset into investable capital; a wealth manager helps structure this transition

Yale School of Management research on post-sale transitions finds that sellers who plan for purpose, identity, and relationships — not just finances — report significantly better outcomes. The closing table is too late to start that conversation.

Frequently Asked Questions

How long does it take to sell a business?

Most business sales take six months to two years from initial engagement to close, depending on business size, preparation level, and market conditions. Starting preparation 12–18 months early is the single biggest factor in compressing that timeline.

How do I know if it's the right time to sell?

The right time combines personal readiness (clarity on your next chapter) with strong business performance — ideally when revenue and EBITDA are still growing. A professional valuation helps determine whether current market conditions support your goals.

What documents do I need to prepare when selling my business?

Buyers expect: three years of financials and tax returns, customer and vendor contracts, commercial leases, employee agreements, SOPs, and IP documentation. Having these organized before going to market accelerates every stage of the process.

How is a business valuation determined?

EBITDA multiples are the primary benchmark, adjusted for industry, growth rate, customer concentration, and owner dependency — applied to your adjusted EBITDA after normalizing add-backs. Comparable recent transactions in your sector also factor into the final range.

What is the difference between a strategic buyer and a financial buyer?

Strategic buyers — competitors and industry players — seek synergies and often pay a premium to expand into new markets or eliminate competition. Financial buyers, such as private equity firms and independent investors, focus on return on investment and typically run the business as a standalone operation.

How do I keep my business sale confidential?

Working through a business broker protects confidentiality via blind teasers, NDAs before sharing financials, and controlled buyer vetting — so employees, customers, and competitors don't learn about the sale prematurely. Chelsis Financial structures every engagement this way, with confidentiality protocols in place before the first buyer conversation.