Here's the harder truth: by the time a buyer makes an offer, the valuation is largely determined by decisions made years earlier. This guide covers what exit valuation actually means, the three gaps that reveal where you stand today, the factors buyers scrutinize most, the methods used to calculate value, and the practical steps that move the needle before you go to market.

TL;DR

- Exit valuation is shaped by decisions made years before a sale — not weeks

- Three planning gaps — Wealth, Value, and Profit — reveal whether your business can actually fund the exit you want

- Five factors drive what buyers will pay: financial performance, growth potential, market position, management independence, and industry timing

- Income-based, market-based, and asset-based approaches each suit different business types

- Reducing owner dependency, cleaning up financials, and diversifying revenue are the highest-impact pre-sale improvements

Why Business Valuation Is the Foundation of Your Exit Strategy

According to the Exit Planning Institute, only 20–30% of businesses put on the market actually sell. The reasons are predictable — and mostly preventable. Unrealistic pricing expectations, poor financial records, and deals that fall apart in due diligence account for the majority of failed transactions.

A formal valuation addresses all three at once. It replaces gut estimates with a data-backed picture of what buyers will actually pay — grounding expectations before they harden into deal-breakers.

Valuation as a Strategic Compass

Most owners treat valuation as a pre-sale formality. That's a costly framing. A valuation used as a running metric — tracked annually, not just once — informs decisions that compound over time:

- When to hire and how to structure leadership

- Which revenue streams deserve investment

- Whether customer concentration has become a liability

- How close you are to an exit-ready financial profile

Owners who track this number annually make different decisions — and arrive at the sale table in a stronger position because of it.

The Cost of Waiting

Business Enterprise Institute data shows that closing a value gap can take 5–10 years, and tax planning often requires 3–10 years of lead time. If an unexpected trigger forces a faster exit — a health event, burnout, or an unsolicited offer — owners without a current valuation are forced into reactive decisions on someone else's timeline.

Getting ahead of that timeline starts with knowing where you stand. Chelsis Financial's Complimentary Assessment of Value gives Midwest business owners a data-backed baseline — what the business could realistically command — without any commitment to a sale process.

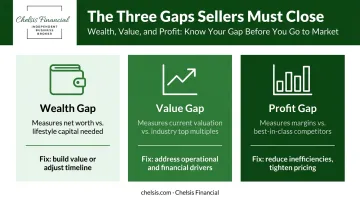

Understanding the Three Gaps That Shape Your Exit Readiness

Exit planning professionals use a three-gap framework to show where a business owner stands today versus where they need to be at exit. Each gap demands a different response.

The Wealth Gap

The Wealth Gap is the difference between your current net worth and the capital required to sustain your desired post-sale lifestyle. It answers a specific question: is the business, at its current value, worth enough to fund your next chapter?

A large gap means more value must be built before exiting. A small gap gives the owner more flexibility on timing and deal structure.

The Value Gap

The Value Gap measures the distance between your company's current valuation and the multiples that top-performing businesses in your industry command. It tells you how much runway exists for improvement — and what specific operational changes would close it.

That disconnect has real consequences. IBBA data shows 23% of advisors cite unrealistic seller value expectations as the top reason deals fail to close. Owners who haven't tracked their Value Gap often carry a number in their head that the market won't support.

The Profit Gap

The Profit Gap is the difference between your current profit margins and those of top-performing competitors. This gap often signals pricing weaknesses or operational inefficiencies that suppress both profitability and the multiple a buyer will apply.

Closing the Profit Gap before going to market doesn't just improve earnings — it improves the multiple applied to those earnings. A business moving from a 3x to a 4x multiple on $500K in EBITDA adds $500K to the sale price without changing revenue at all.

Quick Reference: The Three Gaps

| Gap | What It Measures | Primary Fix |

|---|---|---|

| Wealth Gap | Net worth vs. lifestyle capital needed | Build value or adjust timeline |

| Value Gap | Current valuation vs. industry top multiples | Address operational and financial drivers |

| Profit Gap | Your margins vs. best-in-class competitors | Reduce inefficiencies, tighten pricing |

Key Factors That Drive Your Business Exit Valuation

Buyers aren't paying for what your business earns today. They're paying for what they expect it to earn under their ownership — adjusted for every risk they can identify. Five factors shape that calculation.

Financial Performance and Consistency

Historical revenue, profit margins, cash flow stability, and debt levels form the quantitative core of any valuation. Consistency matters as much as scale.

Per IBBA's Q4 2022 data, poor financials were the top reason deals under $500K failed to close, at 43%. Buyers and their lenders must verify every material claim — and when the numbers tell an unclear or inconsistent story, confidence erodes and offers compress.

Chelsis Financial requires sellers to have three years of P&Ls, balance sheets, and tax returns fully reconciled before going to market, with clear explanations for any anomalies or add-back adjustments.

Growth Potential

A business trending upward, with reliable forecasts and a clear expansion plan, commands stronger multiples than one that's plateaued. Buyers in growth industries often pay for future earnings — meaning a smaller but faster-growing business can command a higher multiple than a larger stagnant one.

Market Position and Competitive Advantage

How buyers perceive your strategic value depends on several positioning signals:

- Differentiated offerings that competitors can't easily replicate

- Pricing power — the ability to raise rates without losing customers

- Brand reputation and recognizable market presence

- Recurring revenue from contracts, subscriptions, or repeat customers

- Customer loyalty reflected in low churn and high retention rates

Companies with defensible positioning secure higher multiples. Those that look interchangeable with competitors do not.

Management Strength and Operational Independence

If the business can't function without the owner's daily involvement, buyers discount the purchase price to account for transition risk. This is key-person risk — and it's one of the fastest ways to suppress a valuation or lose buyer interest entirely.

Signs that key-person risk is under control include:

- A management team that handles daily operations without owner input

- Documented processes and systems that don't live in one person's head

- Key employees willing to stay through and after closing

Chelsis Financial is direct on this point: the firms that attract the broadest buyer interest are those where a capable team will stay post-closing.

Industry Conditions and Market Timing

Even after addressing every internal factor, external conditions set the ceiling. Sector trends, regulatory shifts, buyer demand, and economic cycles all shape the benchmark multiples in any given industry.

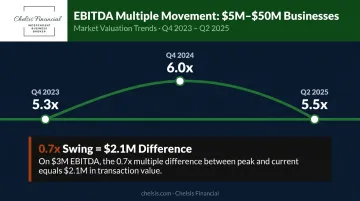

IBBA's Market Pulse data illustrates the volatility: $5M–$50M businesses averaged 5.3x EBITDA in Q4 2023, moved to 6.0x in Q4 2024, then settled at 5.5x in Q2 2025. That 0.7x swing on a $3M EBITDA business is a $2.1M difference in outcome — driven entirely by timing, not by anything the owner did.

Valuation Methods and How to Calculate Your Exit Value

Professionals typically use multiple methods in combination to cross-validate results. The right primary method depends on the nature of the business and the industry.

Income-Based Approach (DCF)

The Discounted Cash Flow method projects free cash flows over a 3–5 year forecast period, then discounts them to present value using a rate that reflects business risk. A terminal value — representing all cash flows beyond the forecast window — is calculated in the final year, typically by applying an industry-comparable exit multiple to projected EBITDA.

Terminal value typically represents 60–80% of total implied company value in DCF models, which is why selecting the right exit multiple matters as much as the cash flow projections themselves.

This approach works best for businesses with predictable, recurring earnings — and it's the primary method used for most operating businesses in:

- Manufacturing and industrial services

- Technology and SaaS platforms

- Healthcare and professional services

- Distribution businesses with contracted revenue

Market-Based Approach

Where DCF projects what a business should be worth based on its own cash flows, market comps ground that estimate in what buyers are actually paying. This method applies an industry-specific multiple — commonly to EBITDA, EBIT, or revenue — based on comparable recent transactions. Multiples vary by deal size and sector.

IBBA's private-market data provides useful context:

| Deal Size | Metric | Average Multiple | Period |

|---|---|---|---|

| Under $500K | SDE | 2.8x | Q4 2023 |

| $1M–$2M | SDE | 3.0x | Q4 2023 |

| $5M–$50M | EBITDA | 5.3x | Q4 2023 |

| $5M–$50M | EBITDA | 6.0x | Q4 2024 |

| $5M–$50M | EBITDA | 5.5x | Q2 2025 |

These are private-market transaction benchmarks — not public-company figures, which run considerably higher and shouldn't be used as sale-price targets.

Asset-Based Approach

The asset-based approach calculates fair market value by adding up tangible and intangible assets, then subtracting liabilities. It's the right primary method for two specific situations:

- Asset-heavy businesses — real estate holding companies, equipment-intensive operations, or capital-heavy manufacturers where physical assets drive value

- Wind-down or liquidation scenarios — where ongoing earnings power is limited or irrelevant to the transaction

For service-based businesses, this method typically understates value. Cash flow, customer relationships, and operational systems don't show up on a balance sheet — but they're often what buyers pay for.

How to Maximize Your Business Value Before You Sell

Value-building requires time. Last-minute improvements rarely move a multiple. The owners who exit on their terms are almost always the ones who started working on the business years before going to market.

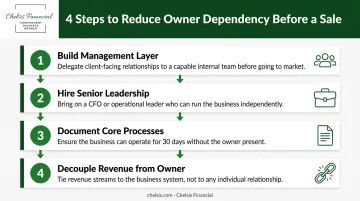

Reduce Owner Dependency

This is the single most impactful change most owners can make. Practical steps:

- Build a capable management layer and delegate client-facing relationships

- Bring in a CFO or experienced operational leader if the business can support it

- Document core processes so the business can run without you for 30 days

- Demonstrate that revenue is tied to the business, not to you personally

Buyers will probe for key-person risk during due diligence. A capable team that stays post-closing is one of the clearest signals that a business can operate without its founder.

Diversify Revenue and Customer Base

Chelsis Financial applies a specific threshold: no single customer should represent more than 10–15% of total revenue. Above that level, buyers raise concerns — and lenders may impose stricter terms, require higher equity, or decline financing altogether.

In one transaction, customer due diligence revealed that nearly 50% of revenues were tied to four key accounts. The result was a **30% reduction in the offer price**. Spreading revenue across more customers and introducing recurring or contracted revenue streams reduces this risk and strengthens your position at the negotiating table.

Strengthen Financial Records

Clean, well-organized financial statements covering at least three years are non-negotiable. Specifically:

- P&Ls, balance sheets, and tax returns must be fully reconciled

- Unexplained expenses or owner perks run through the business trigger scrutiny

- A Statement of Seller's Discretionary Earnings (SDE) is the basis for sale pricing

Migrating to cloud-based accounting like QuickBooks Online before going to market also helps — when a buyer's CPA can verify numbers in hours instead of days, confidence increases and deal friction decreases.

Build Operational Systems

Documented processes, scalable workflows, and clear organizational structures signal that the business can run independently. Buyers want to see that knowledge isn't locked in the owner's head. That means:

- An org chart with defined roles and reporting lines

- Documented standard operating procedures for key functions

- A transition framework that survives the ownership change

EPI data indicates that up to 80% of business value can be attributed to intangible capitals — human, customer, structural, and social. Businesses that command premium valuations build these systems intentionally, well before a sale is on the horizon.

Time the Exit Strategically

Exiting during strong financial performance, active buyer demand, and favorable conditions yields materially better outcomes than selling under pressure. IBBA's data shows multiples can shift by nearly a full turn within two quarters. Owners who track their valuation as an ongoing metric — rather than checking it once — are positioned to recognize when conditions have aligned for an optimal exit.

Working with an experienced business broker gives sellers access to a qualified buyer network and structured support from valuation through closing — reducing the risk that a strong business sells for less than it's worth simply due to poor timing or preparation.

Common Exit Planning Mistakes That Hurt Your Valuation

Most sellers don't lose value in the negotiation — they lose it long before a buyer ever appears. These are the mistakes that show up most often:

- Starting too late. Owners who begin exit preparations only when they're ready to sell are forced to take whatever value currently exists. Closing a value gap takes 5–10 years. Tax planning takes 3–10 years. There's no shortcut.

- Accepting a single-buyer deal. One of the most costly mistakes Chelsis Financial observes is owners who negotiate with one buyer — no competitive process, no leverage. When a buyer knows there's no competition, offers weaken and terms get punitive. A proper sale process creates competitive tension that protects the seller.

- Using an outdated valuation. Owners without current data routinely overprice or underprice their businesses. Overpricing drives away qualified buyers. Underpricing leaves significant money on the table — neither outcome works when those proceeds are meant to fund retirement.

- Going it alone. M&A advisors, business brokers, attorneys, and CPAs each bring specialized knowledge to the table. Without them, legal, financial, and tax decisions get made in isolation — often with consequences that only become visible at closing.

Frequently Asked Questions

What is an exit valuation?

An exit valuation estimates the worth of a business at the point of a sale, merger, or acquisition. It incorporates buyer perspective, market multiples, and transition risk — making it more transaction-specific than a general business valuation used for financing or planning.

How do you calculate the exit value of a company?

The most common approach uses the Discounted Cash Flow method. Project future free cash flows and estimate a terminal value using an industry-comparable EBITDA multiple. Then discount everything to the present using a risk-adjusted rate — the result is your estimated enterprise value.

How far in advance should I get a business valuation before selling?

Plan to get a formal valuation at least five years before your target sale date. That lead time lets you close value gaps, clean up operations, and make changes that meaningfully improve your final sale price.

What factors most increase a business's exit valuation?

The top drivers: reducing owner dependency, diversifying the customer base, demonstrating consistent and growing cash flow, building a management team that operates independently, and operating in a sector with active buyer demand.

What's the difference between a business valuation and an exit valuation?

A business valuation is a general assessment of worth for any purpose — financing, benchmarking, or planning. An exit valuation specifically estimates what a business could sell for in a transaction, incorporating buyer expectations, current market multiples, and the risks a new owner would inherit.

Do I need a business broker to sell my business?

Technically, yes — you can sell independently. But brokers bring a qualified buyer network, negotiation experience, and confidentiality management that most owners can't replicate on their own. Without a competitive buyer process, sellers typically face weaker offers, harsher terms, and a much higher risk of the deal collapsing.