Introduction

Most business owners focus on the selling price. The multiple is what actually determines how much they walk away with.

Here's the math: a business generating $1M in adjusted EBITDA sold at 4x returns $4M. The same business at 6x returns $6M. That's $2M in additional proceeds—from the same earnings, same customers, same operation. The only thing that changed was buyer confidence.

The multiple isn't fixed. It reflects how much risk a buyer perceives in owning your business after you leave. Reduce that risk, and the multiple climbs. Leave it unaddressed, and buyers apply a discount—sometimes a steep one.

The data backs this up. According to IBBA/M&A Source Q2 2024 data, EBITDA multiples ranged from 3.5x for $2M–$5M businesses to 5.3x for $5M–$50M businesses—a gap that preparation can meaningfully close.

The 15 factors covered here are within your control—and starting 12 to 24 months before going to market gives you enough runway to address them in ways buyers will actually credit.

TL;DR

- Buyers pay higher multiples for businesses with lower perceived risk and clearer post-acquisition earnings certainty.

- The 15 ways fall into four areas: financial health, operational independence, revenue quality and market position, and brand and asset value.

- Most meaningful improvements take 12–24 months to show up in the financial record buyers actually review.

- A professional valuation baseline helps identify which levers will move your specific multiple most — Chelsis Financial's complimentary Assessment of Value is a practical starting point.

Why the Multiple—Not Just the Price—Is the Real Measure of a Great Sale

Purchase prices are calculated by applying a multiple to adjusted earnings—typically EBITDA for businesses above $2M, or Seller's Discretionary Earnings (SDE) for smaller owner-operated companies. SDE adds back owner compensation, interest, depreciation, amortization, and discretionary expenses to pre-tax net income, making it the primary pricing basis for Main Street deals.

That multiple is not a formula. It's a buyer's direct risk assessment of your specific business.

What the Market Actually Looks Like

Axial's June 2025 analysis showed wide variation by industry:

| Sector | Median EBITDA Multiple |

|---|---|

| Technology | ~9x |

| Business Services | ~8x |

| Healthcare | ~6x |

| Industrials | ~5x |

Size matters just as much as sector. IBBA/M&A Source data shows Main Street deals (under $2M) trading at 2.0x–3.3x SDE, while lower-middle-market deals ($5M–$50M) reached 6.0x EBITDA average in Q4 2024.

Two Levers That Move the Multiple

Every preparation activity you undertake before going to market works through one of two mechanisms:

- Reducing business risk — cleaning financials, building a management team, diversifying customers

- Activating growth signals — demonstrating scale, market position, and expansion potential

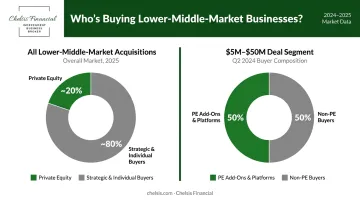

Private equity buyers are increasingly relevant even for founder-led businesses approaching lower-middle-market size. IBBA/M&A Source reported that PE represented roughly one-fifth of lower-middle-market acquisitions in 2025, with PE add-ons and platforms accounting for 50% of buyers in the $5M–$50M segment in Q2 2024.

These buyers assess risk methodically. That's precisely why the 15 factors below have a direct impact on their offer.

Strengthen Your Financial Foundation (Ways 1–4)

Way 1: Clean Up Your Financials

Recasting—adding back owner expenses to show true earnings—is something your advisor handles. Cleaning up is your job.

This means:

- Removing personal or non-business expenses from the income statement

- Reconciling physical inventory and assets with what's on the books

- Strengthening working capital ratios and reducing unnecessary debt

- Ensuring your P&Ls, balance sheets, and tax returns tell a consistent story across all three years

Tax minimization strategies that reduce reported income may save money today, but they directly compress the multiple a buyer will pay. Chelsis Financial requires sellers to have three years of financial statements fully reconciled before going to market—because buyers and their lenders scrutinize exactly this material.

Way 2: Document Your Operations

Buyers aren't just purchasing earnings—they're purchasing a system they can operate without you. Written SOPs, job descriptions, and a current org chart tell them the business is replicable.

Well-organized records also reduce friction in due diligence. When a buyer's CPA can verify numbers in days rather than weeks, confidence rises and deal momentum holds.

Chelsis Financial recommends migrating to cloud-based accounting (such as QuickBooks Online) before going to market—it's not cosmetic, it materially speeds diligence.

Way 3: Improve Cash Flow

Buyers are purchasing future cash flows. Everything that improves net income—tighter margins, reduced owner perks, disciplined expense management—makes the business more valuable.

Unpredictable cash flow forces buyers to apply a higher discount rate to projected earnings, which directly compresses the multiple. Steady, upward-trending cash flow has the inverse effect—it signals lower risk and justifies a higher price.

Way 4: Clean Up Physical and Administrative Presentation

How a business looks—physically and on paper—signals operational discipline.

Practical steps:

- Dispose of idle or unproductive assets

- Remove personally-used business assets from the books

- Ensure the facility is well-maintained

- Resolve outdated contracts, unaddressed liabilities, and disorganized vendor files

Every unresolved loose end is a red flag that chips away at buyer confidence during due diligence.

Build a Business That Doesn't Depend on You (Ways 5–8)

Way 5: Build an Independent Leadership Team

Owner dependency is one of the fastest ways to suppress a valuation multiple—or lose buyers entirely.

Advisory data from Strategic Exit Advisors suggests founder-dependent businesses often receive valuations 30–50% below comparable peers, while independent lower-middle-market businesses can achieve 7x–8x EBITDA versus the 3x–4x that highly dependent businesses struggle to reach.

Chelsis Financial has seen this dynamic play out directly. In one documented case, a Wisconsin commercial millwork manufacturer brought in professional management five years before his exit. The result was a highly competitive transaction process—specifically because buyers didn't need to find an operator to take over.

Building independence means:

- Assembling a leadership team with defined roles and decision-making authority

- Including non-compete and confidentiality agreements for key personnel

- Having at least two outside voices on a board or advisory committee

- Ensuring managers can speak to company objectives without the owner present

Way 6: Put Your Business Plans in Writing

Once you have a leadership team in place, documentation proves they're operating from a shared direction — not just following the owner's instincts. Buyers model future performance under their ownership, and formal plans give them something concrete to work from.

At minimum, that documentation should include:

- Three-year financial forecasts with underlying assumptions

- An org chart showing roles, responsibilities, and succession paths

- Documented operating procedures for sales, fulfillment, and finance

If every senior leader can articulate the company's major objectives clearly and consistently, buyers see a business that can be scaled. If they can't, buyers see a dependency problem in disguise.

Way 7: Demonstrate Agility

Small businesses have a structural advantage: they can pivot faster than large competitors. Document it.

Collect specific examples of how the business has:

- Recognized and captured new market opportunities

- Adapted to regulatory or supply chain shifts

- Changed course successfully in response to competitive pressure

Buyers applying a risk discount assume the future will be rocky. Specific examples of past pivots — with outcomes — push back against that assumption directly.

Way 8: Show a Consistent Track Record

Volatility requires buyers to apply a higher risk discount. Consistency does the opposite.

Due diligence standards typically require three to five years of financial history—income statements, balance sheets, cash flow statements, and interim year-to-date figures. Sellers should have at minimum three years of clean records ready before buyer outreach begins.

Steady revenue growth and consistent margins give buyers confidence in their earnings projections. Unexplained swings, missing years, or inconsistencies between tax returns and P&Ls raise questions that erode offers.

De-Risk Revenue, Market Position, and Growth (Ways 9–12)

Way 9: Broaden Your Customer Base

The 10% rule: no single customer should represent more than 10% of revenue.

High customer concentration is one of the most common value suppressors in small business transactions. Chelsis Financial documented a packaging company acquisition where nearly 50% of revenues were tied to four accounts. After customer due diligence revealed vulnerability in those relationships, the buyer reduced the offer by 30% and restructured additional deal terms.

CT Acquisitions notes that the 10%–20% range begins triggering scrutiny and potential multiple reductions. Above 20%, expect earnouts, escrows, or retention-based deal protections to become part of the structure.

Supplier concentration carries the same weight. Single-source dependencies create parallel risk that buyers will price into the deal just as aggressively.

Way 10: Reach Scale Before Going to Market

Below certain thresholds, the buyer pool shrinks significantly. Axial's 2025 buyer demand analysis found that PE demand concentrates heavily in the $3M–$10M EBITDA range, while individual buyers and search funds cluster below $3M.

GF Data confirms a size premium: sub-$10M deals trade at lower multiples than the $10M–$25M tier. If you're close to a meaningful threshold, organic or strategic growth before going to market can expand the buyer pool and shift the conversation from SDE multiples to EBITDA multiples—a framing that consistently favors sellers of profitable businesses.

Way 11: Grow in Scope Strategically

Expanding into adjacent products, services, or geographies increases perceived potential. More importantly, it gives buyers evidence of execution—not just ambition.

- Niche players should consider adjacent revenue verticals that leverage existing relationships

- Generalist businesses should evaluate whether specialization could attract higher-value clients

Whatever the direction, document it with clear strategy and results. A revenue line that appeared two years ago and has scaled consistently tells a far better story than a new initiative launched three months before going to market.

Way 12: Know and Own Your Market Position

Execution alone isn't enough — sellers also need to own the narrative around their market. Buyers will ask hard questions, and sellers who arrive with clear answers build confidence that pure financial metrics can't capture. That means being able to articulate:

- Market size and growth direction

- Your specific niche within the competitive landscape

- Barriers to entry that protect your position

- Why your market share is defensible

Axial's transaction data showed multiples ranging from 4.93x to 8.84x within the same sector—the difference driven largely by company-specific attributes including scale and market position.

Maximize Cash Flow, Hidden Assets, and Presentation (Ways 13–15)

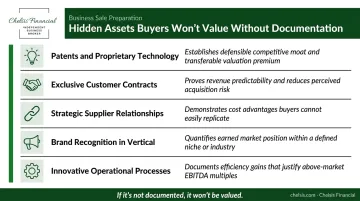

Way 13: Recognize and Document Hidden Assets

Value extends beyond revenue and profit. Buyers won't assign value to assets they can't see.

Intangibles worth documenting:

- Patents and proprietary technology

- Exclusive or long-term customer contracts with successor clauses

- Strategic supplier relationships and preferred pricing arrangements

- Brand recognition within your specific vertical

- Innovative operational processes that competitors haven't replicated

Chelsis Financial has seen proprietary systems—such as unique routing technology in a call-handling operation—cited as differentiating a business from its industry peers and driving higher valuations. If it's not documented, it won't be valued.

Way 14: Trim Non-Core Operations

Once hidden assets are documented, the next question buyers ask is: how much of this depends on you? Lean, focused operations are easier to acquire and integrate. Outsourcing non-core functions signals that the business runs on systems—not on the owner's personal involvement.

Common functions worth outsourcing before a sale:

- Payroll and HR administration

- Logistics and freight management

- IT support and infrastructure maintenance

- Facilities management

It also demonstrates that individual vendor relationships—not the owner—handle peripheral functions. For buyers, this reduces post-acquisition complexity and makes the transition cleaner.

Way 15: Build Your Brand Within Your Industry

Buyers are drawn to businesses with strong reputations in their vertical. Public brand recognition is less important than being known and respected by the right audience.

Targeted actions with measurable impact:

- Active participation in trade associations

- Thought leadership content in industry publications

- Community presence in your region

- Consistently visible among qualified prospects and referral partners

Buyers regularly pay a higher multiple for businesses with established niche authority—it shortens due diligence, reduces perceived risk, and often eliminates competing offers entirely.

How Long Before a Sale Should You Start Preparing?

Meaningful preparation is not a 60-day project. Kreischer Miller advises that preparing a privately held business for sale can take 12 to 24 months or more—and for businesses with significant operational gaps, the timeline may extend to three years. Improvements need to show up in the historical financial record buyers review. A management hire made last month doesn't carry the same weight as one made two years ago.

Quick Wins vs. Long-Term Plays

Within 90 days:

- Reconcile three years of financials and tax returns

- Migrate to cloud-based accounting if not already there

- Prepare a clean org chart and key roles documentation

- Organize customer contracts with successor clauses

- Identify and document intangible assets

12+ months of sustained effort:

- Build and stabilize a leadership team

- Diversify the customer base below the 10% threshold

- Grow toward meaningful EBITDA scale thresholds

- Establish a consistent track record of margin and revenue growth

The earlier you start, the more credibly the improvements show up when buyers open the books. That's exactly the kind of clarity Chelsis Financial's complimentary Assessment of Value is designed to provide. It reviews three years of financial statements, evaluates tangible and intangible assets, and identifies which of these 15 levers will have the greatest impact on your specific multiple—so your preparation has a clear target from day one.

Frequently Asked Questions

What drives higher valuation multiples?

Higher multiples reflect lower perceived buyer risk. Clean financials, a management team that doesn't depend on the owner, diversified revenue, a defensible market position, and a consistent earnings history all reduce risk—and buyers pay a premium for businesses that demonstrate all of them together.

What is the Rule of 40 for valuation multiples?

The Rule of 40 applies specifically to SaaS and high-growth software companies: if revenue growth rate plus profit margin equals or exceeds 40%, buyers in the tech space use it to justify higher revenue multiples for companies not yet highly profitable. It doesn't apply to manufacturing, services, or most traditional SMBs.

What is a good EBITDA multiple for a small business?

It depends heavily on size and sector. Main Street businesses (under $2M) typically transact at 2.0x–3.3x SDE. Lower-middle-market businesses ($2M–$5M) average around 3.5x EBITDA, while the $5M–$50M range reached 6.0x EBITDA in Q4 2024. Industry matters too—technology and business services command higher medians than industrials.

How long does it take to improve a business valuation multiple?

Building a management team, diversifying customers, and cleaning up financials typically require 12 to 24 months to appear credibly in the historical record buyers review during due diligence. Surface-level cleanup can happen faster, but the factors that actually move multiples need time to stick.

What is the difference between an EBITDA multiple and a revenue multiple?

EBITDA multiples are applied to earnings and are standard for established, profitable businesses; revenue multiples are used for early-stage or high-growth companies where profitability isn't yet the primary metric. For most sellers, EBITDA multiples are more favorable—they're applied to a smaller number with a higher multiplier attached.

Can I improve my valuation multiple without growing revenue?

Yes. Many of the highest-impact factors—building a management team, documenting operations, diversifying customers, cleaning up financials—improve buyer risk perception without requiring top-line growth. A business with flat revenue and strong operational independence will often command a higher multiple than a growing business that depends entirely on its owner.