Introduction

You've spent years — maybe decades — building your business. But when the time comes to sell, most owners discover they have no clear idea what their company is actually worth. That uncertainty is expensive.

According to CNBC and M&T Bank research, 98% of small business owners didn't know the value of their companies. That gap shows up at the negotiating table: unrealistic asking prices scare off qualified buyers, while underpricing leaves years of earned value behind.

This guide is for small-to-mid-sized US business owners who are preparing to sell — or beginning to think about it. Whether your timeline is six months or three years out, understanding how valuation works before entering negotiations is one of the most valuable things you can do.

The sections ahead cover what business valuation actually is, the three core methods used, what drives value up or down, how to prepare your financials, and when professional help is worth the cost.

TL;DR

- Business valuation uses documented financial methods — not gut instinct — to determine what a private company is worth

- The three main approaches are income-based, market-based, and asset-based — accurate valuations typically draw from all three

- Consistent cash flow, diversified customers, and owner independence are the value drivers that move the price most

- Starting preparation 1–3 years before your target sale date gives you time to move the needle on each of those factors

- A professional assessment sharpens your pricing and improves deal outcomes — many brokers, including Chelsis Financial, offer this at no cost

What Is Business Valuation — and Why Does It Matter Before Selling?

Business valuation is the process of determining the economic value of a privately held company using documented financial analysis. Public companies have a market price visible by the second. Private businesses require structured analysis to establish what a willing buyer would reasonably pay a willing seller.

That standard comes directly from IRS Revenue Ruling 59-60, which has defined fair market value for private companies since 1959.

Why Valuation Matters Before You List

A formal valuation does three concrete things for a seller:

- Sets a defensible asking price — one you can back up when buyers push back

- Prepares you for due diligence — buyers will conduct their own analysis; knowing your numbers means no surprises

- Reveals value gaps — weaknesses you can fix before going to market rather than watching them compress your offer

These three benefits assume one thing: that you understand what your valuation actually represents. Valuation and final sale price are not the same number. A valuation establishes a methodology-based foundation. Where the deal lands depends on buyer competition, strategic fit, deal structure, and market conditions — all of which can push the price higher or lower than that foundation.

The 3 Core Business Valuation Methods

No single method tells the complete story. Professional valuations typically use all three approaches to triangulate a defensible range — then weight them based on the business type. Asset-heavy companies lean on the asset approach; service businesses with strong cash flow lean on income-based methods; all benefit from market comparisons.

Before walking through each method, it helps to understand the two earnings metrics you'll encounter most:

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) — strips out financing and non-cash items to show operational profitability; used for mid-market businesses with professional management

- SDE (Seller's Discretionary Earnings) — starts with net profit and adds back owner compensation and discretionary expenses; the standard metric for owner-operated small businesses

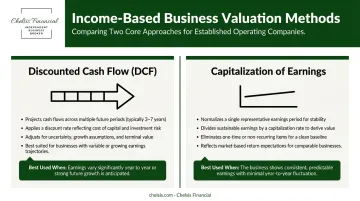

Income-Based Approach

This method values the business based on its capacity to generate future cash flows. The two primary versions are:

- Discounted Cash Flow (DCF): Projects future earnings over multiple periods, then discounts them back to present value using a rate that reflects the risk of those cash flows materializing. The discount rate represents the return a buyer demands for bearing that uncertainty — higher risk means a higher rate, which means a lower present value.

- Capitalization of Earnings: A simpler version suited to stable, mature businesses with consistent, predictable cash flow. Rather than projecting multiple years, it divides normalized earnings by a capitalization rate.

This is the most widely accepted approach for operating businesses with positive cash flow. Its accuracy depends on how well-supported the assumptions about growth rate and risk are — which is why buyers scrutinize those assumptions closely in due diligence.

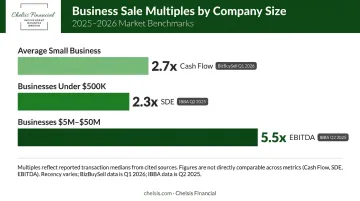

Market-Based Approach

This method estimates value by comparing the business to similar companies that have recently sold. Valuation multiples derived from those comparable transactions are then applied to the subject company's own financial metrics.

Recent transaction data gives a useful benchmark:

- BizBuySell (Q1 2026): average cash-flow multiple for sold small businesses — 2.7x

- IBBA Market Pulse (Q2 2025): businesses under $500K selling at a median 2.3x SDE

- Same report: businesses in the $5M–$50M range at a median 5.5x EBITDA

One practical challenge: truly comparable public companies are usually much larger than most small businesses, so a skilled advisor applies a size discount . Recency also matters — multiples from 2019 tell you very little about what buyers will pay in 2025.

Asset-Based Approach

This method calculates value as the net fair market value of all assets minus liabilities. Assets include both tangible items (equipment, property, inventory) and intangible ones (intellectual property, customer lists, brand goodwill).

The asset-based approach tends to produce the lowest valuation and is most appropriate for asset-intensive businesses, holding companies, or distressed operations.

A note on goodwill: Goodwill is the premium buyers pay above hard asset value — it represents operational strength, customer relationships, reputation, and documented systems.

The critical distinction for sellers is whether that goodwill is enterprise goodwill (transferable to a new owner) or personal goodwill (tied to you specifically). A business where relationships, referrals, and reputation live entirely in the owner's head carries significantly less transferable value than one where those elements are embedded in systems and a team.

Key Factors That Influence Your Business's Value

The valuation methods above produce a number. These factors determine whether that number is high or low.

Financial Performance

Buyers examine 3–5 years of financial history and look for clean, stable, upward-trending numbers. Revenue trajectory, profitability margins, and cash flow consistency form the quantitative backbone of any valuation. Unexplained dips, inconsistency between tax returns and P&Ls, or missing documentation all create doubt, and that doubt compresses multiples.

Customer Concentration

A business where one or two clients represent a disproportionate share of revenue carries meaningful risk. If a single customer walks out the door, so does a large chunk of earnings.

Chelsis Financial flags customer concentration above 20–30% with a single client as a major underwriting concern, one that affects both valuation and deal structure. A diversified customer base signals resilience and gives buyers confidence that future cash flows are stable.

Owner Independence

When the owner is the business — the primary salesperson, the key relationship-holder, the only one who knows how things work — buyers see risk. This "key-man" dependency is one of the most common value suppressors in small business sales. Companies with documented processes, a capable team, and operations that function without the owner's daily involvement command noticeably higher multiples.

Industry and Growth Conditions

A business operating in a growing sector commands higher multiples than one in a contracting market. BizBuySell industry data shows Online and Technology businesses averaging 3.33x earnings versus Manufacturing at 3.03x — and those differences compound as business size increases. The sector you're in sets the ceiling for what multiples buyers are willing to pay.

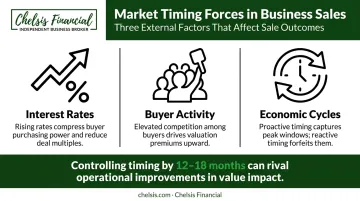

Market Timing

Three external forces shape the market you're selling into:

- Interest rates — higher borrowing costs reduce buyer purchasing power and compress multiples

- Buyer activity — more qualified buyers competing for deals drives prices up

- Economic cycles — sellers who choose their timing rather than react to personal pressure consistently see better outcomes

Controlling when you sell, even by 12–18 months, can be worth as much as the operational improvements you make in the meantime.

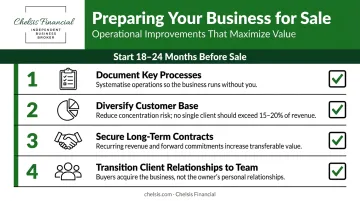

How to Prepare Your Business for a Higher Valuation

The US Chamber of Commerce recommends starting preparation 18–24 months before going to market, with the sale process itself typically taking another 10–12 months. That timeline isn't arbitrary — it reflects how long it takes to meaningfully move the factors that buyers care about.

Use that window deliberately. Every improvement you make before going to market translates directly into higher cash flow, lower perceived risk, or both — and buyers price those factors into their offers.

Financial Housekeeping

- Organize 3–5 years of P&Ls, balance sheets, cash flow statements, and tax returns

- Remove personal or non-business expenses from company books

- Ensure consistency across all financial documents — if your P&L and tax return tell different stories, expect scrutiny

- Consider migrating to cloud-based accounting software (QuickBooks Online, for example) if you're still running spreadsheets

Chelsis Financial's Assessment of Value reviews all four core financial statements — income/P&L, cash flow, balance sheet, and SDE statement — for the current year and the prior three years. Organized records shorten the review timeline and give buyers fewer reasons to discount their offer.

Operational Improvements

- Document key processes so they don't live only in your head

- Diversify your customer base before going to market, not after

- Secure or renew long-term contracts that give buyers confidence in future revenue

- Transition key client relationships from you to a team member

Chelsis Financial works with sellers specifically on reducing owner dependence before a sale — including bringing in professional management and shifting from day-to-day operator to a more removed role. Business owners who start this work 18–24 months out consistently command stronger offers than those who enter the process unprepared.

Common Mistakes Business Owners Make When Valuing Their Business

Emotional Overvaluation

Owners who've built a business over 20 years naturally attach personal meaning to it. That's understandable , but buyers evaluate future earnings potential, not historical sacrifice. An asking price anchored to sweat equity rather than financial fundamentals will collapse in due diligence. The Q4 2022 Market Pulse survey found that 23% of advisors cited unrealistic seller value expectations as the primary reason deals failed to close.

Relying on Rule-of-Thumb Multiples

"Businesses sell for 2–3× profit" gets repeated so often that owners treat it as fact. NACVA's training materials explicitly state that rules of thumb should only be used as a "sanity check" because they presume an average business and frequently misstate actual equity value.

The right multiple depends on factors specific to your business:

- Industry and sector risk

- Revenue size and growth trajectory

- Customer concentration

- Owner dependency and management depth

The result of using the wrong multiple is either a deal that never closes or money left on the table.

Skipping a Formal Valuation Before Negotiations

Owners who enter sale discussions without a professional valuation lose leverage. When a buyer presents their own (lower) valuation, you need an objective basis to push back. Without one, you're negotiating on instinct against someone who has the data. Disorganized financials make this worse — they hand buyers a concrete reason to cut their offer during due diligence.

Should You Value Your Business Alone or Work With a Professional?

Online calculators and rule-of-thumb estimates can give you a rough directional number — useful for a sanity check, not useful for an actual sale. A professional valuation holds up under buyer scrutiny, lender review, and legal examination. DIY tools don't.

Understanding the Different Credentials

| Role | Credential | Primary Function |

|---|---|---|

| Certified Valuator | CPA/ABV, CVA, ASA | Formal, credentialed opinion of value for legal, tax, or transactional use |

| Business Broker | IBBA-affiliated | Positions the business, identifies buyers, and manages the transaction |

Both add value — at different stages. A certified valuator is most useful when you need a number that will hold up in court or satisfy a lender. A business broker is most useful when you're ready to actually sell, because their job is to translate that number into a closed deal.

Where Chelsis Financial Fits

Chelsis Financial offers a Complimentary Assessment of Value for business owners considering a sale — a no-cost, no-commitment starting point that reviews your financials, assesses market comparables, and gives you a professional perspective on what your business is worth and what factors could improve it before going to market.

The assessment reviews income statements, cash flow, balance sheets, and SDE going back three years, incorporating industry benchmarks and comparable transaction data — the same foundation used to set defensible asking prices and support lender discussions.

If you're thinking about a sale — even if the timeline is 2–3 years out — starting that conversation early gives you time to act on what you learn. Reach Chelsis Financial at +1 866-842-5151 to get started.

Frequently Asked Questions

How do you calculate what a business is worth when selling?

Business value is determined using three approaches — income-based, market-based, and asset-based — with the most accurate valuations combining all three. The result is a range, not a single number, and a qualified professional determines which method carries the most weight based on your specific business type, size, and industry.

Is a business typically worth three times its profit?

"3× profit" is an oversimplification that may roughly apply to certain small, stable businesses, but it's far from universal. Actual multiples vary significantly by industry, growth rate, customer concentration, and size — BizBuySell data shows the current average at 2.7x, while larger mid-market businesses regularly exceed 5x EBITDA.

What documents do I need for a business valuation?

Core requirements include 3–5 years of P&Ls, balance sheets, cash flow statements, and tax returns, plus a current SDE statement. Buyer and lender due diligence also typically requires operating agreements, customer contracts, equipment lists, and employee information — organized, reconciled records move the process faster and support a stronger valuation.

What is the difference between EBITDA and SDE in business valuation?

SDE adds back the owner's salary and personal benefits to net profit, making it the standard metric for owner-operated small businesses where the owner's compensation is part of the earnings picture. EBITDA normalizes operating earnings without owner add-backs and is used for mid-market businesses with professional management in place.

How far in advance should I get a business valuation before selling?

Get a valuation 1–3 years before your intended sale date. That window gives you time to address weaknesses the valuation surfaces, strengthen your financials, and time the sale to favorable market conditions rather than personal necessity.

What is the difference between a business valuation and the final sale price?

A valuation establishes an evidence-based, methodology-backed estimate of fair market value. The final sale price is what a buyer actually pays — which can be higher due to buyer competition or strategic synergies, or lower due to negotiation, contingencies, or deal structure. Understanding that gap is why skilled deal structuring matters as much as the number itself.