The gap between a successful transaction and a costly mistake rarely comes down to luck. It comes down to preparation, clarity, and the quality of advice you surround yourself with.

This guide walks through the most critical considerations for both buyers and sellers — from valuation and business preparation to deal structure, due diligence, and choosing the right advisory team.

TL;DR

- Define your exit objectives before going to market — sellers with clear goals consistently close on better terms

- Only 20–30% of businesses that go to market actually sell — preparation is what separates the successful minority

- Get a professional valuation early; most owners overestimate their value, and knowing the real number gives you time to close the gap

- Buyers must scrutinize financials, customer concentration, owner dependency, and hidden liabilities before making any offer

- Deal structure, the LOI, and your advisory team are what ultimately determine whether a transaction reaches the closing table

Clarify Your Motivations and Set Clear Objectives Before You Sell

Most sellers spend more time planning a product launch than they do planning their exit. That's a costly oversight.

Understanding why you're selling shapes every decision that follows — pricing strategy, timeline, deal structure, and who you're willing to sell to.

Want to Sell vs. Need to Sell

The distinction matters more than most owners realize:

| Motivation Type | Common Drivers | Impact on Strategy |

|---|---|---|

| Want to sell | Retirement, burnout, new challenge, liquidity | Time to plan, optimize, and negotiate from strength |

| Need to sell | Health crisis, debt pressure, competitive decline, divorce | Speed becomes priority, often at the cost of price |

Chelsis Financial refers to crisis-driven scenarios as the "Dismal D's": divorce, debt, disaster, disinterest, or declining performance. Each one is manageable, but all of them compress timelines and reduce your negotiating leverage.

Three Exit Scenarios

Chelsis Financial identifies three exit structures based on seller priorities:

- Quick Exit : Prioritizes immediate liquidity. Speed matters most, which typically means accepting a discounted valuation. For some owners, certainty today outweighs potential upside tomorrow.

- Market-Based Exit : Focuses on fair value supported by data, with balanced deal structure and performance alignment.

- Bright Future Exit : Allows sellers to participate in future upside through earnouts, seller notes, or equity rollovers. Highest potential long-term value, but requires trust and alignment with the buyer.

What a Real Exit Strategy Looks Like

Deciding to sell isn't an exit strategy. A proper plan includes:

- A target exit date with realistic preparation milestones

- A plan to maximize business value before listing

- Tax-efficiency considerations built in from the start

- Post-sale financial planning for the proceeds

- Clear priorities: price, employee welfare, business continuity, legacy

Not all of these goals are compatible. Knowing which ones are non-negotiable before negotiations begin prevents last-minute concessions.

One more factor worth getting right: timing. The best time to sell is when the business is in a visible growth phase — trending clearly upward, not yet at peak. Buyers pay a premium for momentum. Selling during a decline limits your options and often forces concessions that a better-prepared seller would never accept.

Know What Your Business Is Actually Worth

Here's an uncomfortable truth: most business owners don't know what their company is worth. A 2022 CNBC report citing an M&T Bank survey found that 98% of polled small business owners didn't know the value of their companies. Many who do have a number in mind are working from emotional attachment rather than market data.

The Three Core Valuation Approaches

Per SBA guidance, the three standard methods are:

- Income approach — Based on projected cash flow and risk; most common for profitable operating businesses

- Market approach — Compares recent sales of similar businesses; useful for benchmarking

- Asset approach — Total assets minus liabilities; most relevant for asset-heavy or distressed businesses

In practice, most small to mid-market transactions use a combination. For businesses under $2M in value, Seller's Discretionary Earnings (SDE) is the primary metric. Above $5M, EBITDA multiples take over.

What the Numbers Actually Look Like

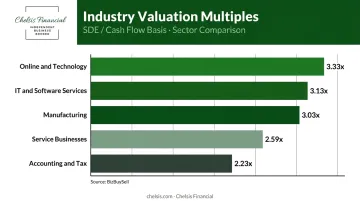

BizBuySell industry data shows the range across sectors:

| Sector | SDE/Cash Flow Multiple |

|---|---|

| Manufacturing | 3.03x |

| Online & Technology | 3.33x |

| IT & Software Services | 3.13x |

| Service Businesses | 2.59x |

| Accounting & Tax | 2.23x |

These are market benchmarks, not guaranteed outcomes. A business with high customer concentration, owner dependency, or erratic financials will price at the low end — or not sell at all.

Get Your Valuation Early

Valuation is partly math, partly judgment. The financial model gives you a range — but what moves you within that range, or above it, are subjective factors:

- Brand strength and competitive positioning

- Management depth (does the business run without you?)

- Customer loyalty and concentration risk

- Growth trajectory and recurring revenue

An early professional valuation isn't just useful for pricing — it's a diagnostic. It tells you where the gaps are while you still have time to close them. Chelsis Financial offers a complimentary Assessment of Value that gives business owners a market-informed starting point: what the business is worth today, and what specific improvements could increase that number before going to market. Some owners who engage years ahead of a planned sale have seen value increases of up to 73% by addressing the gaps the assessment reveals.

Prepare Your Business to Attract the Right Buyers

Buyers evaluate businesses across five dimensions: profitability, solvency, market position, management capability, and customer base. Weaknesses in any one of these will either kill a deal or force price concessions.

The Owner Dependency Problem

If a business only functions because the owner is present, buyers will see a liability — not an opportunity.

Owner dependency is one of the most common value suppressors in small to mid-market transactions, and Chelsis Financial consistently identifies it as a preparation gap. The solution takes time.

One client began planning five years before his target exit at 65, brought in professional management, and transitioned from active operator to absentee owner. That transition "added a lot of value to the business" and made the eventual sale highly competitive.

Steps to reduce owner dependency:

- Hire a CFO or COO well before listing — buyers need to see that operations don't depend on the founder

- Document all core processes so the business runs without the owner in the room

- Transfer key customer and vendor relationships to other team members

- Add outside board members if you have two or more years before your target exit date

Financial and Legal Readiness

Before going to market, sellers should have:

- Three years of clean, fully reconciled financial statements (P&L, balance sheet, tax returns)

- Customer revenue breakdown — anything above 20–30% concentration in a single client needs to be addressed or disclosed

- Updated contracts with "successor" clauses ensuring obligations survive ownership change

- Resolved legal, regulatory, or IP issues

- An organized diligence-ready file before the first offer arrives

Confidentiality Is Non-Negotiable

Even a rumor of a pending sale can unsettle employees, alarm customers, and damage the business value you're trying to protect. Confidentiality should be treated as a discipline, not an afterthought:

- Require signed NDAs before sharing any business information with prospective buyers

- Work through a broker who pre-screens buyers before names or details are disclosed

- Limit internal knowledge to those with an absolute need to know

What Buyers Should Evaluate Before Making an Offer

Clean financials don't guarantee a sound acquisition. The real question is whether those numbers tell the full story — and thorough due diligence is how you find out.

Financial Verification

Don't just review the numbers. Validate them. Key questions:

- Do the P&L statements align with tax returns? Flag any meaningful divergence and require explanation.

- Are revenue trends consistent, or were recent years unusually strong (or weak)?

- Are add-backs and owner benefits clearly documented and defensible?

Customer Concentration Risk

Revenue tied to a handful of clients is one of the most common deal risks buyers underestimate. Kreischer Miller defines concentration as any customer representing 8% or more of total revenue, while Morgan & Westfield notes that concentration above 30–50% may make a business unsalable without deal structure adjustments.

In one transaction Chelsis Financial managed, a packaging company had nearly 50% of revenues tied to four accounts — and a Net Promoter Score of just 7%. That discovery drove a 30% reduction in the offer price.

Owner Dependency — The Buyer's View

Customer concentration isn't the only concentration risk. If the seller is the business, the transition itself becomes a liability. Buyers should assess:

- Whether the management team can sustain performance post-close

- Which customer relationships are tied to the seller personally

- What a realistic transition period looks like, and whether the seller is willing to support it

Market Position and Growth Potential

Understanding where a business sits in its lifecycle shapes how you price and structure the deal. A company at a genuine growth inflection point may justify a premium — one that has already peaked may carry risks the current financials don't capture. Key questions to ask:

- Is the competitive position defensible, or are margins being squeezed by new entrants?

- Are growth projections supported by pipeline, contracts, or market trends — or just optimism?

- Has the business already captured most of its addressable market?

Deal Structure, Negotiation, and Legal Considerations

Asset Sale vs. Stock Sale

The structure of the transaction has major tax and liability implications for both sides:

- Asset sale — Buyer purchases specific assets and assumes designated liabilities only. Buyers typically prefer this because they avoid inheriting unknown liabilities and can step up the tax basis on acquired assets.

- Stock sale — Buyer acquires the entire entity, including all existing liabilities. Sellers often prefer this for simpler transfer treatment and potential tax advantages.

Address this negotiation point early. Waiting until late in the process to surface a disagreement on structure wastes legal fees and risks the deal entirely.

The Letter of Intent

The LOI is a non-binding roadmap that outlines key deal terms before significant resources are committed. It should cover:

- Purchase price and structure

- Earnout provisions (if any)

- Exclusivity period

- Treatment of employees

- Due diligence timeline and access

The LOI is also the right moment to surface deal-breakers. Attempting to renegotiate structural issues after signing the LOI — when the seller has agreed to exclusivity — dramatically weakens the seller's position.

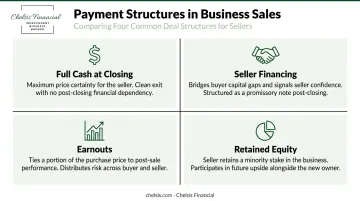

Payment Structures and Protecting Yourself

Once the LOI is signed, how the deal gets paid becomes the next pressure point. The IBBA/M&A Source Q2 2025 Market Pulse reported sellers received 78–92% cash at closing across deal sizes, with seller financing ranging from 6–15% depending on deal size.

Common payment structures include:

- Full cash at closing — Maximum certainty for the seller

- Seller financing — Bridges buyer financing gaps and signals seller confidence; Chelsis Financial recommends featuring it prominently in listing materials

- Earnouts — Ties part of the purchase price to post-sale performance, distributing risk but adding complexity

- Retained equity — Allows sellers to participate in future upside

When financing any portion of the deal, sellers should negotiate specific protections: personal guarantees, a security interest in business assets, and clear default provisions. Goodwill isn't a substitute for documented collateral.

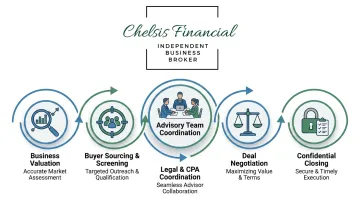

Build the Right Advisory Team for a Successful Transaction

Attempting to navigate a business sale alone — while also running the business — is a setup for a poor outcome. The process is too complex, too time-consuming, and too emotionally charged for a solo approach.

The Four Advisors Every Party Needs

| Advisor | Role |

|---|---|

| Business Broker / Intermediary | Manages the full process, buyer outreach, qualification, negotiation, and confidentiality |

| Transaction Attorney | Reviews and enforces all legal documents, including the purchase agreement and representations |

| Accountant | Structures the deal for tax efficiency; reconciles financials for buyer scrutiny |

| Financial / Wealth Advisor | Helps plan post-sale wealth management and investment strategy for proceeds |

What Chelsis Financial Manages on Your Behalf

Chelsis Financial handles the full transaction lifecycle for sellers — from the complimentary Assessment of Value through closing. Specific responsibilities include:

- Independent, market-informed business valuation

- Buyer sourcing from a network of over 2,000 businesses across the Midwest

- Buyer screening and qualification before any business information is shared

- Coordination with attorneys, CPAs, lenders, and escrow agents

- LOI advisory and deal structure negotiation support

- Confidentiality management throughout every stage

Sellers stay focused on running their business while Chelsis Financial manages the transaction. That division of focus protects business performance during due diligence — one of the most critical factors in whether a deal closes at full price.

Contact Chelsis Financial at 866-842-5151 to schedule a complimentary Assessment of Value, or book a confidential discovery call to get started.

Frequently Asked Questions

How long does it typically take to sell a business?

Most business sales take between 6 and 12 months from initial preparation to closing. The IBBA Q2 2025 Market Pulse reported engagement-to-close timelines of 6–9 months, with LOI-to-close ranging from 2–4 months depending on deal size. Well-prepared businesses with clean financials consistently close faster.

What are the most common methods used to value a business?

The three standard approaches are income-based (projected cash flow), market-based (comparable sales), and asset-based (total assets minus liabilities). Most small to mid-market transactions use a combination, weighted toward income-based methods. Professional valuation is strongly recommended before setting an asking price.

What is the difference between an asset sale and a stock sale?

In a stock sale, the buyer acquires the entire company, including all existing liabilities. In an asset sale, only specific assets and designated liabilities transfer. Tax and liability implications differ significantly — buyers typically favor asset sales to avoid unknown liabilities, while sellers often prefer stock sales for tax treatment.

How do I keep my business sale confidential?

Require signed NDAs before sharing any business information with prospective buyers. Work through a business broker who screens and qualifies buyers before introductions are made, and limit internal knowledge of the sale to only those with an absolute need to know.

Do I need a business broker to sell my business?

Technically no, but the process is extremely complex. A qualified broker manages buyer outreach, qualification, negotiation, and confidentiality — functions that are difficult to execute while also running a business. Represented sellers consistently achieve better closing rates and final prices than those who go it alone.

What should a buyer look for when evaluating a business to purchase?

Start with these five areas:

- Multi-year financial trends

- Customer concentration and revenue dependency

- Owner dependency and management team depth

- Existing contracts, liabilities, and lease terms

- Any undisclosed legal or regulatory exposure

Always engage a transaction attorney and accountant before making an offer — what you find during due diligence will either validate the price or give you grounds to renegotiate.