Introduction

Most business owners spend years — sometimes decades — building something valuable, then hit a wall when it's time to exit. The buyer search feels opaque. Listings go stale. Deals fall apart in due diligence. And more often than not, the business sells for less than it's worth because the process wasn't structured properly from the start.

This guide is specifically about finding investors who want to acquire your business outright — not fund it, not take a minority stake, not partner for growth. That distinction matters, because acquisition buyers are an entirely different pool with different motivations, deal criteria, and search behaviors.

What follows covers the four things that determine whether your exit succeeds:

- Who acquisition buyers actually are and what drives them

- How to prepare your business before any outreach begins

- Where to find qualified acquisition investors

- How to approach them without compromising confidentiality or deal value

TLDR

- Know your buyer type before you start — individual acquirers, private equity, strategic buyers, and family offices each have distinct deal criteria

- Clean financials, a defensible valuation, and documented operations are prerequisites, not afterthoughts

- Run multiple channels at once: broker relationships, business marketplaces, and industry networks work best in combination

- Never share financials or identify your business by name without a signed NDA in place

- Working with a broker who maintains a vetted buyer network closes deals faster and reduces risk compared to searching solo

Who Actually Buys Businesses (And What They're Looking For)

Acquisition investors are not startup investors. They aren't looking for a compelling vision or early-stage potential — they want proven cash flow, operational stability, and a clear path to return. Understanding who's actually in the market shapes everything about how you search.

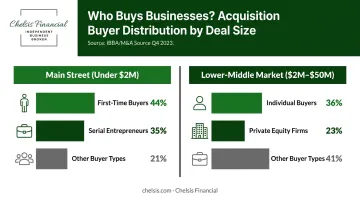

According to IBBA/M&A Source Q4 2023 data, individual buyers dominated Main Street transactions (deals under $2M): first-time buyers accounted for 44% of acquisitions and serial entrepreneurs 35%. In the lower-middle market ($2M–$50M), individual buyers made up 36% and private equity firms 23%.

Individual Acquisition Entrepreneurs

This is a growing and often underestimated buyer category. These are professionals — frequently from corporate or trades backgrounds — who have chosen to buy an existing business rather than build one from scratch. BizBuySell's Q1 2026 Insight Report found that 49% of small-business buyers identified as "corporate refugees," up from 44% the prior quarter.

What they want:

- Consistent, documented revenue with owner-operator systems in place

- A business that can run without the current owner present day-to-day

- Financing that works — typically a mix of personal capital, SBA loans, and occasionally seller financing

Private Equity and Search Funds

PE firms and search funds — particularly those focused on the lower-middle market — look for businesses with EBITDA above a defined threshold, scalable operations, and a clear growth thesis. They move quickly once interested, but expect organized financials and professional representation from the start.

Stanford GSB's 2024 Search Fund Study and IESE's 2024 international data show that 79% of concluded international search funds successfully acquired a company, with a median purchase price of $11.7M — signaling a real and active buyer class at the lower-middle-market level.

Strategic Buyers

Strategic buyers are companies in the same or adjacent industry looking to acquire for market share, talent, customer lists, or shared efficiencies. They often pay a premium because the acquisition creates value beyond the business's standalone financials.

The tradeoff is real: longer due diligence, more complex negotiations, and a higher bar for financial documentation. In Chelsis Financial's transaction history, manufacturing and healthcare verticals draw the strongest strategic buyer interest — sectors where geographic coverage, specialized capabilities, or regulatory approvals make acquisitions worth a premium.

What they want:

- Complementary capabilities, customer lists, or geographic coverage

- Clean financials that can withstand rigorous due diligence

- A clear rationale for how the acquisition strengthens their existing operations

Family Offices

Family offices are private wealth management structures increasingly treating small business acquisitions as alternative assets. UBS's 2024 Global Family Office Report shows family offices allocated 11% of strategic assets to direct investments in 2023. Deloitte found 29% planned to increase private equity investments — more than any other asset class surveyed.

What distinguishes them: family offices are patient capital. They typically offer flexible deal structures, longer transition timelines, and less pressure to hit short-term performance targets than PE buyers.

What they want:

- Stable cash flow with low owner-dependency

- Reasonable entry price relative to earnings

- Flexible deal structures, including earnouts or seller notes

How to Prepare Your Business Before Searching for Investors

Preparation is the step most sellers skip or rush — and it's the one that determines whether a deal closes at full value or falls apart in due diligence. Buyers lose interest fast when basic questions can't be answered. Disorganization signals risk, and nothing compresses a valuation multiple faster.

Get a Professional Business Valuation

Before you approach anyone, you need a number you can defend. A credible valuation sets your asking price, helps you target the right buyer tier, and prevents you from either walking away underpriced or scaring off buyers with an unrealistic figure.

Valuation benchmarks vary significantly by deal size:

- Businesses under $500K: typically 2.0x SDE

- Businesses $1M–$2M: typically 3.0x SDE

- Businesses $5M–$50M: typically 5.3–6.0x EBITDA

Chelsis Financial offers a Complimentary Assessment of Value for sellers who want a clear picture of what their business is worth before going to market. The assessment reviews three years of financial statements, industry comparables, and growth potential. All conversations remain fully confidential.

Organize Your Financial Records

Buyers and their lenders will scrutinize everything. At minimum, have three years of the following ready before any outreach:

- Profit & Loss statements

- Tax returns (fully reconciled to your P&Ls)

- Balance sheets

- Cash flow statements

- Seller's Discretionary Earnings (SDE) calculation

If your P&L and tax returns diverge by a notable margin, be prepared to explain why. Unexplained discrepancies slow due diligence and reduce buyer confidence.

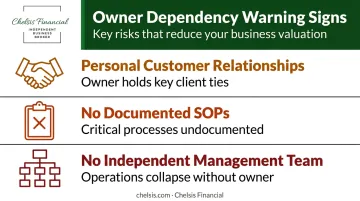

Document Operations and Reduce Owner Dependency

High owner dependency is one of the fastest ways to suppress your valuation or lose a buyer entirely. When a business can't function without its owner, the buyer pool shrinks considerably. Buyers who remain will push for earn-outs, extended transitions, or lower prices to offset that risk.

The most common dependency issues Chelsis Financial encounters:

- Customer relationships held personally by the owner (especially in services businesses)

- No documented SOPs, leaving critical processes known only to the owner

- Absence of a management team that can operate independently post-sale

The fix takes time, which is why addressing this years before a planned sale matters. Bringing in a CFO or operations lead, documenting key processes, and transitioning customer relationships to the team all directly increase buyer confidence and deal value.

Identify and Address Liabilities Early

Issues that surface unexpectedly in due diligence kill deals — or force price reductions. The most consequential liability concerns include:

- Customer concentration above 20–30% of revenue in one account

- Pending or undisclosed litigation

- Contracts that may not survive ownership transition

- Environmental risks (particularly in manufacturing)

Proactive disclosure protects deal momentum. Buyers who feel misled at any stage rarely stay at the table.

Prepare a Confidential Information Memorandum (CIM)

The CIM is the professional document you share with qualified, NDA-signed buyers. It replaces informal pitches and ensures consistent, controlled messaging throughout the process.

A standard CIM covers:

- Business description and operating overview

- Three-year financial performance

- Market position and competitive landscape

- Growth opportunities

- Ideal buyer profile and transition considerations

Chelsis Financial prepares CIMs, teasers, and blind summaries as part of its deal packaging services. Every document that reaches a buyer is accurate, professionally positioned, and appropriately confidential.

Where to Find Investors to Buy Your Business

Your search strategy should match the buyer type you're targeting. Reaching out indiscriminately — without qualifying buyers first — wastes time and creates real confidentiality risk.

Work with a Business Broker

A business broker with an active, vetted buyer registry is the most efficient route for most sellers. Brokers match your business to buyers who already meet budget, industry, and acquisition criteria requirements — before anyone outside that circle knows you're for sale.

Chelsis Financial maintains a buyer network of 2,000+ businesses in Indiana alone, with reach across the broader Midwest. The firm connects sellers with qualified acquirers across manufacturing, healthcare, technology, industrial contracting, and automotive sectors — while managing confidentiality throughout.

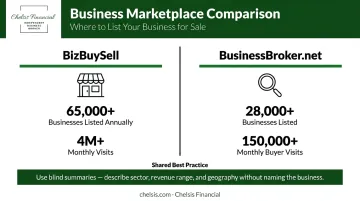

List on Business-for-Sale Marketplaces

Online marketplaces attract individual buyers, acquisition entrepreneurs, and search funds actively searching for deals. Key platforms include:

- BizBuySell — claims 65,000+ businesses listed annually and 4M+ monthly visits

- BusinessBroker.net — 28,000+ businesses listed, 150,000+ monthly buyer visits

Listings on these platforms should be written to attract the right buyers without revealing the business identity prematurely. A blind summary that describes the business by sector, revenue range, and geography — without naming the company — is standard practice.

Tap Industry and Professional Networks

Strategic buyers often come from within your own sector. Competitors, suppliers, or major customers may be logical acquirers — and they may pay a premium because the acquisition solves a specific strategic problem for them.

These conversations need to be handled through an intermediary — approaching a competitor or customer directly risks exposing your intent prematurely and weakening your negotiating position.

Leverage Advisor and Attorney Referrals

M&A attorneys, CPAs, and financial advisors often know of buyers or can provide referrals within their networks. If you have an existing advisory team, ask directly whether they're aware of parties with acquisition interest in your sector. A single referral from a trusted advisor can open a conversation that a public listing never would.

How to Approach and Qualify Potential Buyers

Not every inquiry is a serious buyer. Many people express interest without the capital, operational experience, or genuine intent to close. Treating every inquiry as a real opportunity wastes time and creates confidentiality exposure.

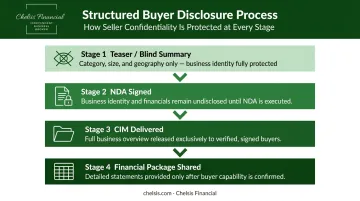

Use NDAs and Structured Disclosure

Every substantive buyer conversation should follow a staged disclosure process:

- Teaser / blind summary — describes the business category, size, and geography without naming it

- NDA signed — before the business is identified or financials are shared

- CIM delivered — full business overview released only to qualified, verified buyers

- Financial package shared — detailed statements provided after buyer screening confirms capability and intent

This structure protects you throughout. Confidentiality breaches cause key employees to worry and leave, alert competitors, and expose your customer base — damage that translates directly into lost deal value.

Screen for Financial Capability and Intent

Before advancing any buyer conversation, confirm:

- Can they demonstrate proof of funds or financing pre-approval?

- Do they have relevant operational experience for this type of business?

- What is their acquisition timeline, and is it realistic?

- Have they completed acquisitions before?

Screening early shields your employees and customers from premature exposure, and saves you months of time on a buyer who was never going to close.

Working with a Business Broker to Find the Right Investor

A broker's value goes well beyond posting a listing. The right one gives you:

- Access to vetted buyers who have already been screened for financial capability and acquisition intent

- Confidential process management — your employees, customers, and competitors don't learn the business is for sale

- Deal structuring expertise — knowing when to push back on terms, how to structure seller financing or earn-outs, and where deals typically stall

- Professional representation — buyers take brokered deals more seriously, and the presence of a broker signals an organized, credible seller

BizBuySell data shows the median small-business sale in 2025 took 170 days to close, with IBBA/M&A Source reporting an average of 7–10 months from advisor engagement to closing. Sellers who begin disorganized add time to both ends of that window.

That timeline also depends on who's running your process — which brings up a common question sellers ask early on.

Broker vs. M&A Advisor: Which Do You Need?

| Business Broker | M&A Advisor | |

|---|---|---|

| Deal size | Typically under $2M | $2M–$50M+ |

| Buyer pool | Individual buyers, acquisition entrepreneurs | PE firms, family offices, strategic buyers |

| Process complexity | 2–6 months typical | 6–12+ months typical |

| Representation style | Transaction-focused | Strategic advisory |

Chelsis Financial operates across both — from straightforward Main Street transactions to more complex lower-middle-market deals involving PE or strategic buyers. Regardless of deal size, sellers start in the same place: a confidential conversation and a complimentary business value assessment.

Frequently Asked Questions

How do I find investors for my business?

Finding acquisition investors involves targeting the right buyer type for your business size, preparing clean financials and a defensible valuation, and using channels like business brokers, M&A marketplaces, and industry networks to reach qualified buyers. Most sellers find that working with a broker delivers the best results — brokers handle buyer access, screening, and confidentiality in a single engagement rather than leaving sellers to manage each piece separately.

What is the 10% investor rule?

In business acquisition financing, the "10% rule" refers to the SBA's equity injection requirement: buyers using SBA 7(a) loans must contribute at least 10% of their own capital, and seller notes may count toward this threshold under specific standby conditions.

What types of investors typically buy small businesses?

Four buyer types dominate small business acquisitions, each with different deal size requirements and motivations:

- Individual acquisition entrepreneurs — professionals buying their first business, often from corporate or trades backgrounds

- Private equity firms and search funds — targeting stable EBITDA and growth potential

- Strategic buyers — competitors or adjacent companies seeking operational synergies

- Family offices — patient capital investors looking for alternative assets

How do I value my business before finding a buyer?

Valuation is typically based on a multiple of Seller's Discretionary Earnings (SDE) for smaller businesses or EBITDA for businesses generating over $1M–$2M in earnings. Working with a professional broker or appraiser gives you a defensible number to present to investors — Chelsis Financial provides a complimentary valuation assessment if you want a grounded starting point.

Should I tell my employees I'm looking for a buyer?

No — maintain strict confidentiality during the search. Premature disclosure can unsettle employees, alert competitors, and cause customers to reconsider commitments, all of which can reduce deal value or cause a transaction to fall apart before it closes.

How long does it take to find an investor to buy a business?

Timelines vary by business size, preparation level, and buyer type. IBBA/M&A Source data shows the average runs 7–10 months from advisor engagement to closing. Sellers who work with a broker and have organized documentation in place typically move through the process faster than those starting unprepared.