But that same familiarity cuts both ways. Share your financials, customer lists, and pricing strategy with a competitor — and then watch the deal collapse — and you've handed your most capable rival a roadmap to outmaneuver you. The risk is real.

The good news: it's manageable. With the right process, strict information controls, and a qualified intermediary, selling to a competitor can be one of the cleanest, most profitable exits available to a business owner. This guide covers how to evaluate whether a competitor is the right buyer, how to prepare your business, how to protect confidential information at every stage, and what the step-by-step process actually looks like.

TL;DR

- Competitors often pay strategic premiums — but only when you run a structured, competitive process

- Never approach a competitor directly; always use a business broker or M&A advisor first

- Get a professional valuation before any contact — valuation gaps drove 26% of failed deals (Pepperdine, 2025)

- Follow a staged disclosure model: teaser and NDA first, then CIM, IOI, and LOI before due diligence

- Include both strategic and financial buyers in your process to create competitive tension

Should You Sell Your Business to a Competitor?

The Strategic Case

Competitors make motivated buyers for one reason: they already understand what they're buying. Your customer relationships, operational workflows, and market position don't require explanation. That reduces their risk — and risk reduction often shows up as a higher offer.

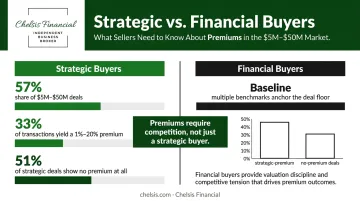

According to IBBA/M&A Source Q1 2023 Market Pulse data, strategic buyers represented 57% of buyers in the $5M–$50M deal segment. Competitors aren't a niche buyer type — they're the dominant acquirer category in the lower middle market.

A strategic premium isn't guaranteed, though. Pepperdine's 2025 data shows 51% of strategic buyer transactions involved no premium over financial buyer multiples, while 33% showed a 1%–20% premium. The premium materializes when you create competition — not when you negotiate with one buyer in isolation.

When It Makes Sense (and When It Doesn't)

Selling to a competitor works well when:

- You're planning retirement and want a buyer who can preserve operations without a long transition

- Your industry is consolidating and competitors are actively acquiring

- You want to free up capital for a new venture with a faster, cleaner exit

- The competitive landscape is shifting and staying independent carries real risk

It's the wrong move when:

- You haven't prepared financials or organized documentation

- You're negotiating with only one buyer and haven't engaged an advisor

- You're willing to skip the NDA process to accelerate conversations

- The potential buyer has a history of using due diligence as a fishing expedition

Process and confidentiality controls matter more than buyer type. A well-structured sale with proper NDA protections is far safer than an unstructured conversation, regardless of how trustworthy the acquirer seems.

How to Prepare Your Business Before Approaching a Competitor

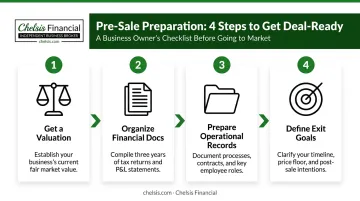

Establish a Realistic Business Valuation

Before any competitor contact happens, you need an independent valuation. Knowing your number matters less than being able to defend it. A credible, third-party valuation anchors the negotiation before a competitor can reframe it.

Pepperdine's 2025 report identified valuation gaps as the cause of 26% of failed deal engagements, with 84% of those gaps ranging from 11%–30%. A competitor who knows your industry can spot an inflated asking price immediately and use it to control the negotiation.

Chelsis Financial's Complimentary Assessment of Value is a practical starting point. The assessment reviews three years of financial statements, P&Ls, cash flow statements, and balance sheets, and produces a realistic market value based on current benchmarks — not wishful thinking. For the $5M–$50M segment, IBBA/M&A Source reported 5.5x EBITDA as the Q2 2025 benchmark.

Organize Your Financial Documentation

Competitors scrutinize financials differently than financial buyers — they have industry benchmarks to compare against. Be ready before the first substantive conversation.

Required financial documentation:

- Three years of profit and loss statements, fully reconciled with tax returns

- Balance sheets and cash flow statements for the same period

- Normalized EBITDA calculation with documented add-backs

- Owner benefit analysis and seller's discretionary earnings (SDE)

Chelsis Financial advises sellers to prepare this documentation before going to market rather than scrambling during due diligence. When P&L statements and tax returns diverge, expect scrutiny and delays. Using cloud-based accounting (QuickBooks Online, for example) before marketing speeds up due diligence.

Prepare Operational and Legal Documentation

Once financials are in order, the next layer is operational. A competitor will request this package quickly, and having it organized signals a well-run operation — reducing perceived risk and keeping the deal on track.

Key operational documents to prepare:

- Key customer contracts (with names redacted at early stages)

- Supplier and vendor agreements

- Employee rosters and compensation structures

- Intellectual property documentation and licenses

- Asset lists and equipment schedules

- Current organizational chart with key role summaries

Define Your Exit Goals Before Engaging Anyone

Know your non-negotiables before the first conversation. These four areas shape which competitor is actually the right buyer:

- Price range: Your floor, not just your target

- Timeline: Hard deadline vs. flexible transition

- Employee retention: Which roles are non-negotiable to keep

- Brand continuity: Whether the business carries forward under your name

An offer that hits your financial number but eliminates your team or dissolves your brand may not be the right exit. Clarifying this upfront prevents late-stage deal failures, when emotions and sunk costs are at their highest.

The Step-by-Step Process for Selling Your Business to a Competitor

Selling to a competitor follows the same structured process as any M&A transaction — with one critical difference: confidentiality controls must be enforced at every stage, not just at the start.

Step 1: Engage a Business Broker or M&A Advisor Before Any Contact

The first action is hiring a qualified intermediary — not reaching out to the competitor directly, even informally.

An experienced business broker protects your identity during initial outreach, manages information flow, and builds a qualified buyer list that includes both strategic and financial acquirers — producing the competitive tension that yields stronger offers and better terms.

Chelsis Financial explicitly warns against "proprietary deals," situations where a single buyer negotiates without competition. Buyers who know they face no competition consistently make weaker offers with more punitive terms.

Step 2: Create an Anonymous Investment Teaser

Your advisor prepares a one-page anonymized document covering revenue range, EBITDA, industry, and growth narrative — without identifying your company. This teaser generates genuine buyer interest while keeping your identity protected during initial outreach. Competitors receive this document the same way any other buyer would, with no indication of who the seller is until they've demonstrated serious interest and financial capacity.

Step 3: Screen Buyers and Execute NDAs Before Sharing Sensitive Information

Buyer vetting happens before any confidential information changes hands. The evaluation covers:

- Strategic motivation for the acquisition

- Financial capacity to complete the deal

- Alignment with the seller's exit goals

The buyer must sign an NDA before receiving the Confidential Information Memorandum (CIM). The CIM contains detailed financials, operations, and management information — it doesn't get shared until the buyer is vetted and the NDA is signed.

Step 4: Evaluate Offers — From IOI to LOI and Into Due Diligence

Buyer interest escalates through two formal documents:

- IOI (Indication of Interest): Non-binding, issued after CIM review; communicates serious intent and a preliminary valuation range

- LOI (Letter of Intent): More detailed, issued after preliminary diligence; includes proposed purchase price, deal structure, exclusivity period (typically 45–75 days), and due diligence timeline

Due diligence is the highest-risk phase in a competitor transaction. Most M&A due diligence periods run 30–60 days, extending to 90 days for complex deals. Staged document release, virtual data room access tracking, and coordinated advisor oversight are essential controls during this period — without them, a competitor buyer can extract operational intelligence before the deal closes.

Step 5: Negotiate Final Terms and Close the Deal

The final phase covers:

- Purchase price adjustments based on due diligence findings

- Payment structure, including any earn-outs or seller financing (Chelsis Financial typically sees 10%–30% seller financing over 3–5 years in smaller transactions)

- Non-compete clauses and transition periods

- Employee retention provisions

- Closing document package: bill of sale, ownership transfer documents, and any transition service agreements

How to Protect Confidential Information When Selling to a Competitor

The Staged Disclosure Model

Information is released in phases, not all at once:

- Anonymous teaser — industry, revenue range, EBITDA, growth narrative only

- CIM — released only after NDA is signed and buyer is vetted

- Financial detail — full statements shared during structured due diligence

- Trade secrets and full customer data — only at final stages, and in some cases never shared directly

What gets shared, and when:

| Information Type | When Shared | Controls |

|---|---|---|

| Financial statements (anonymized) | After NDA | Standard CIM package |

| Tax returns and P&L detail | Due diligence | VDR with access tracking |

| Customer contracts | Due diligence | Names redacted initially |

| Employee information | Near closing | Limited access |

| Full customer lists, pricing, IP | Final stages only | Third-party verification recommended |

What a Strong Competitor-Specific NDA Must Include

A standard template NDA is insufficient when the buyer is a direct market competitor. Get your legal counsel to prepare a buyer-specific version that covers:

- Precise definition of what constitutes confidential information

- Permitted-use clause — restricts the buyer to using disclosed information for deal evaluation only, not competitive intelligence gathering

- Non-solicitation of customers and employees for a defined period

- Representative signatures requiring the buyer's advisors and team members to also be bound

- Term of at least two to three years

The Delaware case Martin Marietta Materials, Inc. v. Vulcan Materials Co. established that courts will enforce M&A confidentiality restrictions when parties misuse information obtained during deal negotiations. Trust alone isn't a legal remedy. Binding agreements are.

Practical Document Controls

- Stamp all shared materials "Confidential"

- Use a virtual data room (not Google Drive) with access tracking and version control

- Maintain a log of exactly what was shared and when

- Consider independent third-party due diligence for the most sensitive assets — for example, a jointly hired CPA firm that reports findings to the buyer without giving the competitor direct access to raw data

Common Mistakes Sellers Make When Selling to a Competitor

Negotiating with only one buyer. Single-buyer negotiations hand the competitor disproportionate leverage. Even when a competitor initiates the approach — which should itself raise your guard — a structured process that includes multiple buyer types consistently produces better prices and terms. Chelsis Financial documents a case where a founder invited five potential acquirers to a single event, ensuring all five knew they were competing. That signal alone changed the negotiating dynamics entirely.

Making direct contact without an intermediary. A direct outreach signals the business is for sale. That can unsettle employees, trigger market rumors, and allow the competitor to extract strategic information through casual conversation. The FTC's own guidance warns that competitors must manage competitively sensitive information carefully even during legitimate M&A discussions.

Sharing sensitive information too early. Many sellers disclose financials or customer data before the buyer is vetted or a binding NDA is in place — eager to demonstrate value or move faster. With a direct competitor, that information doesn't come back. A structured process with proper vetting prevents this entirely.

Frequently Asked Questions

How do you approach a competitor to sell your business?

The safest approach is through a qualified business broker or M&A advisor who can make anonymous initial inquiries, assess the competitor's interest and financial capacity, and keep the seller's identity protected until a confidentiality agreement is fully executed. Direct outreach is one of the most common — and costly — mistakes sellers make.

Is it a good idea to sell your business to a competitor?

It can be an excellent exit strategy — competitors often pay strategic premiums, move faster through early diligence, and enter negotiations as motivated buyers. The primary risk is information exposure if the deal falls through, which a structured process with strict confidentiality controls addresses directly.

How do you protect confidential information when selling to a competitor?

Use a staged disclosure model — releasing only anonymized information initially, then more detail only after a competitor-specific NDA is signed. Vet buyers before sharing anything sensitive. For proprietary systems or full customer data, consider neutral third-party verification rather than direct competitor access.

Will a competitor pay more for my business than a financial buyer?

Often, yes — but not automatically. Strategic buyers value synergies, market share, and operational fit, which can translate into higher multiples. However, having both strategic and financial buyers in your process creates the competition needed to maximize total value. A financial buyer may also offer better structural terms or flexibility in certain situations.

How long does it take to sell a business to a competitor?

Most structured business sales take 6–12 months from preparation through closing — IBBA/M&A Source reported a 9-month average close time for $5M–$50M deals. Competitor buyers may move faster through early stages, but due diligence should still be thorough regardless of how familiar they are with your industry.

What happens to my employees when I sell to a competitor?

Outcomes vary: MIT Sloan research found 33% of acquired workers leave in the first year following an acquisition, often due to role consolidation when a competitor absorbs overlapping functions. Address employee retention and role protection explicitly in LOI negotiations — before you sign, not after.