That gap exists largely because owners wait until they're ready to exit before thinking seriously about value. By then, the window for meaningful improvement has closed.

Valuation isn't a snapshot of today's revenue. Buyers pay for future earnings potential and the perceived risk of achieving it. Owners who don't prepare early often sell below what they could have achieved — or struggle to attract qualified buyers at all.

This article covers a practical roadmap: the multiplier effect, proven value-boosting strategies, financial cleanup, and timing — everything you need to take control of your sale outcome.

TL;DR

- Up to 80% of owner net worth sits in the business, making valuation improvement personal wealth protection

- A modest EBITDA increase multiplies at your deal multiple — a $50K gain can add $200K+ to your sale price

- Buyers pay for predictability and low risk, not just revenue history

- Financial cleanup and owner independence take years to build, so starting well before a planned exit matters

- Chelsis Financial offers a Complimentary Assessment of Value as a no-obligation first step

Why Business Valuation Matters More Than You Think

The Multiplier Effect Is Bigger Than Most Owners Realize

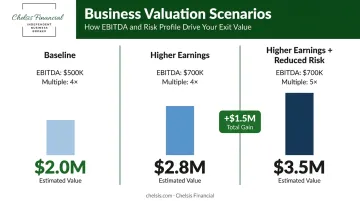

Earnings improvements don't add value dollar-for-dollar — they multiply across the applicable multiple. That compounding effect is where most sellers leave money on the table.

Consider a manufacturing business generating $500K in recast EBITDA. Two years of profitability work pushes that to $700K. Here's how the scenarios compare:

| Scenario | EBITDA | Multiple | Indicated Value |

|---|---|---|---|

| Baseline | $500K | 4x | $2.0M |

| Higher earnings only | $700K | 4x | $2.8M |

| Higher earnings + reduced risk | $700K | 5x | $3.5M |

The same underlying work — improving profitability and reducing owner dependence — produces a $1.5M gain over the baseline. The multiple shift from 4x to 5x accounts for $700K of that difference on its own.

IBBA/M&A Source Q3 2025 data confirms this range: median multiples run 2.0x SDE for deals under $500K, rising to 4.0x SDE for $1M–$2M deals, and 6.5x EBITDA for $5M–$50M transactions. Scale and institutional quality directly move businesses into higher multiple bands.

Buyers Pay for Future Cash Flow, Not Past Performance

Historical financials are a proxy — buyers use them to estimate what the business will earn under new ownership. A business with consistent, growing, predictable revenue commands a noticeably higher multiple than one with flat or erratic performance.

This distinction matters. Improving both the earnings figure (through profitability and revenue stability) and the multiple (by reducing risk) creates a compounding effect. That's the first mindset shift sellers need to make.

Why Starting Early Changes Everything

Most of the changes that move the valuation needle — building a management team, diversifying customers, cleaning up financials — take two to five years to implement and stabilize credibly in the historical record buyers will review.

Chelsis Financial's internal data reflects this clearly: businesses that engage in structured preparation typically realize more value than those that go to market unprepared. Waiting until you feel ready to sell compresses the preparation window — and the strategies covered in the sections below require time to take hold in the financial record buyers will scrutinize.

Know Where You Stand: Getting a Pre-Sale Valuation

Two Types of Valuation — and When Each Applies

Not all valuations serve the same purpose:

- Formal appraisal: Conducted by a credentialed appraiser following rigorous professional standards (ASA, NACVA). Required for SBA financing above $250K where buyer and seller have a close relationship, estate planning, litigation, and other legal purposes.

- Informal calculation of value: A planning-oriented analysis of earnings, market comparables, and business risk factors. Lower cost, faster to complete, and the right starting point for owners 3–5 years from a target sale date.

For most Midwest business owners in the $300K–$11M revenue range, the informal version comes first. It answers the question: Where do I stand today, and what would it take to get where I want to be?

Why Pre-Sale Assessment Should Happen Well Before You're Ready

A pre-sale valuation regularly surfaces issues that take significant time to address:

- Undocumented processes that create transition risk

- Customer concentration above healthy thresholds

- Owner-dependent revenue relationships

- Loose legal or compliance items

- Financial records that don't tell a consistent story

Chelsis Financial's Complimentary Assessment of Value is designed for exactly this stage. Owners provide three years of financial statements, and the assessment delivers a defensible view of current value, identifies gaps, and informs a preparation roadmap, all handled with strict confidentiality. For owners unsure whether they're ready to engage a broker, it's a concrete way to answer that question without committing to a timeline.

Common Valuation Methods

| Method | Best Fit |

|---|---|

| Earnings multiplier (EBITDA/SDE) | Profitable operating businesses with stable earnings |

| Market comparison | Businesses with available comparable transaction data |

| Asset-based | Asset-heavy businesses or those with weak earnings |

| Discounted cash flow (DCF) | Companies with credible forecasts and changing growth profiles |

The right method depends on your industry, business size, and financial profile. For most small-to-mid-market operating companies, the earnings multiplier (EBITDA or SDE) is the dominant approach — which means improving your documented earnings has a direct, measurable impact on what a buyer will pay.

Proven Strategies to Increase Your Business Valuation

Grow and Stabilize Your Revenue

Recurring revenue matters more than one-time revenue. Subscriptions, retainers, and long-term service agreements reduce buyer risk by making future cash flows more predictable. Chelsis Financial's experience reinforces this: buyers consistently cite recurring contracts as a signal that the business has staying power post-acquisition.

Practically speaking:

- Move transactional customers toward service agreements or retainer arrangements where possible

- Include "successor clauses" in long-term contracts, confirming obligations survive an ownership change

- Diversify the revenue base so no single product line or customer relationship creates outsized dependency

That second point — customer diversification — is non-negotiable. Pepperdine's 2025 Private Capital Markets Report found 41% of PE respondents rated customer concentration as an important business risk. Chelsis Financial applies a benchmark of no single customer exceeding 10–15% of total revenue. In one documented transaction, customer concentration near 50% — combined with other diligence findings — led a buyer to reduce the offer price by 30%.

A healthier customer spread doesn't just protect your multiple. It protects your ability to close.

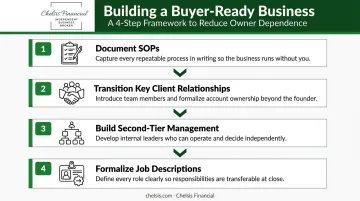

Reduce Owner Dependence

Owner dependence is one of the most common buyer concerns — and, with enough runway, one of the most correctable.

A business that can't function without its owner creates real transition risk. Buyers worry about relationships, key decisions, and institutional knowledge disappearing at closing. That concern sharpens in customer-facing businesses where the owner is the primary contact for key accounts.

Steps to reduce dependence:

- Document standard operating procedures (SOPs) for all critical functions — not just what happens, but who owns it and how decisions get made

- Transition key client relationships to other team members well before going to market

- Build a second tier of management capable of running operations independently

- Formalize job descriptions so authority and accountability are clear without you in the room

Buyers will interview your managers without you present during due diligence. What they find in those conversations shapes their confidence in the business post-close.

Strengthen Your Team and Operations

A strong management team signals leadership continuity and reduced execution risk. Pepperdine's 2025 data found 50% of PE respondents rated management team quality as a very important risk factor — making it one of the top buyer concerns going into any transaction.

What buyers want to see:

- A leadership team that can operate independently, not just support the owner

- Non-compete and retention agreements for key personnel (buyers consistently cite these during due diligence)

- Documented processes that don't exist solely in the owner's head

- A current organizational chart with clear roles and reporting lines

Operational improvements carry equal weight with buyers. A few areas that consistently move the needle:

- Reduce equipment downtime through preventive maintenance schedules

- Eliminate workflow bottlenecks before they show up in diligence

- Replace outdated infrastructure that could trigger capital expenditure concerns

- Present a documented growth plan — even a partially executed one adds perceived value

Clean Up Your Finances Before Going to Market

What "Clean Financials" Actually Means

Buyers and their advisors need to verify every material aspect of the business. Disorganized or inconsistent records don't just slow the process — they create perceived risk that directly affects price.

At minimum, prepare:

- Three years of profit & loss statements, balance sheets, and cash flow statements — fully reconciled

- Tax returns that tell a consistent story with your P&Ls

- Clear explanations for anomalies, one-time events, or year-over-year variances

If your P&L and tax return diverge meaningfully, expect scrutiny. The documentation gap becomes a negotiating lever for buyers.

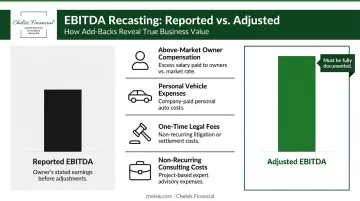

Recasting Financials: The Add-Back Process

Recasting (or normalizing) financials means adjusting for owner-specific expenses, one-time costs, and non-recurring items to reveal the business's true underlying earning power. According to CLA's sell-side quality-of-earnings guidance, adjusted EBITDA in owner-operated companies can differ from reported EBITDA by 30–50% or more — meaning the recast number can substantially change the valuation conversation.

Common add-backs include above-market owner compensation, personal vehicle expenses, one-time legal fees, and non-recurring consulting costs.

Critical caveat: Every add-back must be clearly documented. Buyers and their CPAs will challenge anything that isn't substantiated. Undocumented personal expenses — even if legitimate — are frequently rejected during due diligence, which directly reduces the agreed sale price.

Forward-Looking Projections and Unresolved Liabilities

Buyers want to understand the growth trajectory, not just historical performance. A well-reasoned financial forecast with supporting assumptions builds buyer confidence and can support a premium multiple. Projections that lack supporting rationale, however, do the opposite.

Before going to market, resolve:

- Pending or threatened litigation

- Licensing or permit gaps

- Worker classification or HR compliance issues

- Outstanding tax liabilities

Each item on that list is a potential deal-breaker. CLA reports that approximately one in three signed LOIs fails to close — and unresolved liabilities are a leading cause. They surface in due diligence and become leverage to renegotiate price downward or walk away entirely. Addressing them before going to market removes that leverage from the buyer's hands.

When to Sell and How the Right Advisors Make the Difference

Timing the Market

Selling when the business is on an upswing — not in decline — matters. Buyers extrapolate trends. A business showing three years of consistent growth tells a different story than one that peaked two years ago.

Key timing factors:

- Business performance: Sell during a period of growth, not after a plateau

- Market conditions: Active buyer demand and favorable financing conditions improve outcomes

- Personal readiness: Rushed exits driven by urgency — health, burnout, partnership disputes — weaken your negotiating position

On the macro side, interest rate environments affect buyer financing capacity and deal volume. When credit tightens, fewer buyers can execute leveraged acquisitions, which can compress both the buyer pool and achievable multiples.

That market awareness only pays off if you have the right team in place to act on it.

Choosing the Right Advisors

The advisors you work with determine as much of the outcome as the business itself.

A qualified team typically includes:

- Business broker or M&A advisor: Manages the process, positions the business, and runs a confidential, competitive buyer process

- Tax advisor: Models deal structures and minimizes avoidable tax friction — asset vs. stock sale decisions alone can significantly affect net proceeds

- Legal counsel: Handles LOI review, purchase agreement negotiation, and representation and warranty exposure

- CPA/accountant: Supports due diligence, financial verification, and purchase price allocation

When evaluating a broker or intermediary, look for industry experience, a track record of completed transactions at your business's size, a genuine network of qualified buyers, and transparent communication throughout.

Chelsis Financial works with Midwest business owners across manufacturing, industrial, healthcare, automotive, and technology sectors — providing confidential support from initial valuation through closing. For owners who want a clear picture of where their business stands before committing to a timeline, Chelsis offers a Complimentary Assessment of Value with no obligation to proceed.

Frequently Asked Questions

How do you increase the value of a business before selling?

Value increases come from three areas: improving earnings (profitability, recurring revenue, growth), reducing buyer-perceived risk (owner independence, customer diversification, clean operations), and preparing financials meticulously. The most impactful results come from starting this process 3–5 years before the intended sale.

How far in advance should I start preparing to sell my business?

Plan to start at least 3–5 years before your target sale date. Meaningful improvements take time to implement — and buyers need to see them reflected in at least 2–3 years of financial history. Starting earlier creates more options and a stronger negotiating position.

What is the most important factor buyers consider when valuing a business?

Buyers focus primarily on future cash flow potential and the perceived risk of achieving it. Predictable, recurring revenue combined with low owner dependence and a strong management team consistently commands the highest multiples — regardless of industry or deal size.

How do personal expenses in the business affect the sale price?

Personal and discretionary expenses run through the business can be added back to show true earnings — but only if they're well-documented. Undocumented add-backs are routinely rejected during buyer due diligence, directly reducing the final agreed-upon sale price.

Does reducing owner dependence really impact business value?

Owner dependence is one of the most cited risk factors by buyers. A business that runs smoothly without the owner is more transferable, less risky, and commands a higher multiple — often representing a substantial dollar difference in the final sale price.

What's the difference between a formal appraisal and an informal valuation?

A formal appraisal follows rigorous professional standards (ASA or NACVA) and is required for legal, estate, and SBA financing purposes. An informal calculation of value is a planning-focused estimate used to identify gaps and set improvement priorities before listing.