Introduction

According to PitchBook's 2025 Annual US PE Middle Market Report, US PE middle-market deal value hit $410.7 billion in 2025 — up 8.5% year-over-year. Institutional capital is moving decisively toward established, privately held businesses, and competition for quality deals is only intensifying.

That activity has also brought a flood of firms claiming middle-market expertise. Picking the right advisor is harder than it should be. Common failure modes include:

- Firms too large to give a $25M deal meaningful attention

- Advisors without the buyer relationships to run a competitive process

- Teams that pitch senior bankers but execute with junior analysts

- Advisors who oversell their deal count and underdeliver on preparation

The wrong choice doesn't just create friction. It leaves real money on the table at close.

This guide profiles five of the most active M&A advisory firms for middle-market companies in 2026 and walks through the selection criteria that actually separate good advisors from great ones.

TL;DR

- US PE middle-market deal value hit $410.7B in 2025, with 72.6% of global M&A advisors expecting deal flow to increase further in 2026

- Top firms for 2026 include Harris Williams, Houlihan Lokey, Lincoln International, Capstone Partners, and Raymond James — each suited to different deal sizes and seller profiles

- Prioritize sub-sector track record, senior-banker involvement, and buyer universe depth when shortlisting advisors

- Sellers in the $5M–$100M enterprise value range should assess whether they need a full investment bank or a boutique advisory firm before signing an engagement letter

- Before approaching any advisor, get a realistic read on your business's market value — it shapes every negotiation that follows

What Is Middle-Market M&A Advisory?

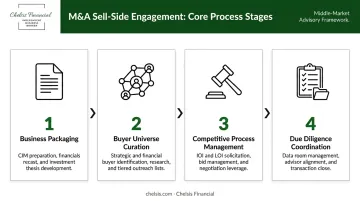

Middle-market M&A advisory is a structured, process-driven discipline — one that looks nothing like listing a business and waiting for calls. The full scope of work includes:

- Packaging the business — building a Confidential Information Memorandum (CIM), financial model, and management presentation

- Curating a buyer universe — identifying strategic acquirers, PE platforms, and family offices with the synergistic fit and capital deployment appetite to drive competitive tension

- Running a competitive process — managing IOI deadlines, management meetings, and LOI negotiations simultaneously

- Coordinating due diligence — organizing data rooms, responding to buyer requests, and keeping multiple parties aligned through closing

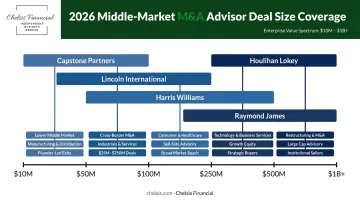

Capstone Partners defines the middle market as businesses valued between $10M and $1B, with the lower middle market covering $10M–$250M and the core middle market spanning $250M–$500M. This blog focuses on the $10M–$500M enterprise value range — the segment where institutional-grade advisory delivers the most measurable impact.

That range matters because the buyer profile changes entirely. At this level, PE sponsors and strategic acquirers run structured diligence processes, deploy deal teams, and move on strict timelines. A business broker — who lists a business and qualifies inbound inquiries — is built for transactions below the $2M–$5M threshold. Above that, a managed competitive process typically produces multiple competing bids, higher valuation multiples, and a materially lower rate of deal fall-through.

Top M&A Advisory Services for Middle-Market Companies (2026)

These five firms were selected based on middle-market deal activity, sub-sector coverage depth, senior-banker involvement, and demonstrated track record with founder-owned and privately held businesses.

Harris Williams

Harris Williams is a Richmond, Virginia-based sell-side advisory firm and PNC subsidiary (acquired in 2005) with eight dedicated industry groups covering aerospace and defense, business services, consumer, energy and infrastructure, healthcare and life sciences, industrials, technology, and transportation and logistics.

What makes Harris Williams distinct is its sub-sector specialist structure. Rather than assigning generalist bankers to any deal that comes in, each group builds genuine pattern recognition within a narrow niche. A seller in facility services or IT services gets a banker who has closed five comparable transactions in the last 18 months — not a generalist with broad sector coverage.

The firm is best suited for sellers in active PE roll-up sub-sectors with $10M+ EBITDA who want a rigorous, competitive auction process.

| Attribute | Detail |

|---|---|

| Deal Size Sweet Spot | $75M–$1B+ EV; best fit for sellers with $10M+ EBITDA |

| Key Specialization | Business services, healthcare services, IT services, industrials |

| Notable Strength | Deepest dedicated sub-sector bench in mid-market sell-side M&A |

Houlihan Lokey

Houlihan Lokey (NYSE: HLI), headquartered in Los Angeles, is publicly reported as the #1 global M&A advisor by deal count — a claim supported by its own investor materials and a PwC 2024 Global M&A Rankings report that identified Houlihan leading US deal count with 307 transactions. The firm operates with 2,000+ financial professionals across a broad platform that includes sell-side M&A, restructuring, and valuation.

Houlihan's standout combination for middle-market sellers is institutional breadth paired with a top-tier restructuring practice. That pairing matters most in complex transactions: deals with distressed elements, cross-border buyers, or situations requiring a fairness opinion alongside the sale process.

| Attribute | Detail |

|---|---|

| Deal Size Sweet Spot | $50M–$1B+ EV; ideal for diversified platforms or complex deal structures |

| Key Specialization | Healthcare, technology, business services, financial services |

| Notable Strength | Global buyer network; top-tier restructuring; fairness opinion capability |

Lincoln International

Lincoln International is a Chicago-based, employee-owned mid-market advisory firm with 25+ offices in 16 countries and a team of 1,400+ professionals. In 2025, the firm closed more than 430 transactions globally. Its independence — no public shareholders, no bank parent — removes the cross-selling pressure and competing priorities common at bank-owned peers.

PE-backed platforms regularly select Lincoln for sponsor-to-sponsor exits. Its active sponsor coverage team also gives founder-owned businesses with PE-ready financials real access to cross-border financial buyers in Europe and Asia, extending well beyond domestic platforms.

| Attribute | Detail |

|---|---|

| Deal Size Sweet Spot | $50M–$500M EV; PE-backed platforms and founder-owned businesses with clean financials |

| Key Specialization | Business services, healthcare, technology, sponsor-to-sponsor exits |

| Notable Strength | Structurally independent; 430+ global transactions in 2025; strong cross-border reach |

Capstone Partners

Capstone Partners expanded significantly in January 2026 with the acquisition of TM Capital and other business units from Janney Montgomery Scott, resulting in approximately 40% headcount growth and a combined firm of roughly 300 professionals. The firm is an IMAP partner member, giving sellers access to a network that has closed 2,200+ transactions valued at $130B over the past decade.

Capstone's key advantage for founder-owned businesses is its deal-size accessibility. While bulge-bracket peers often set informal minimums in the $50M–$75M EV range, Capstone actively serves the lower middle market — businesses in the $10M–$150M EV range that would be underserved or deprioritized elsewhere.

| Attribute | Detail |

|---|---|

| Deal Size Sweet Spot | $10M–$300M EV; lower and core middle-market founder-owned businesses |

| Key Specialization | Business services, healthcare, industrials, TMT, consumer |

| Notable Strength | One of the largest US MMIBs; IMAP global network; ESOP advisory capability |

Raymond James

Raymond James (NYSE: RJF), headquartered in St. Petersburg, Florida, is a diversified financial services firm with approximately 19,000 associates and $1.67 trillion in PCG assets under administration as of fiscal year 2025. Its investment banking arm maintains a broad middle-market M&A practice across business services, healthcare, industrials, and financial services.

What sets Raymond James apart for founder-owned businesses is its integrated wealth management platform. Most pure-play advisory firms hand off after closing — owners who haven't structured their after-tax proceeds are left to figure it out alone. Having advisory and wealth management under one roof closes that gap directly.

| Attribute | Detail |

|---|---|

| Deal Size Sweet Spot | $25M–$500M EV; core middle-market and founder-owned businesses |

| Key Specialization | Business services, healthcare, industrials, financial services |

| Notable Strength | Integrated wealth management; strong PE relationships; broad sector coverage |

How to Choose the Right M&A Advisory Service

The right advisor is determined by fit, not name recognition. Four criteria matter most:

1. Sub-Sector Track Record

Ask every firm to name specific, closed transactions in your exact industry and deal-size band within the last 24 months. Three comparable transactions, minimum. A firm that can't produce those examples without checking internal databases lacks the pattern recognition to run your process.

2. Senior-Banker Involvement

Many firms pitch with managing directors and execute with analysts. Before you sign anything, ask:

- Who will draft the CIM?

- Who manages buyer outreach calls?

- Who negotiates the LOI?

Get names in writing. A vague answer like "a senior team will be involved" is not a commitment.

3. Buyer Universe Depth

The right firm should produce a preliminary buyer list — segmented by strategic buyers, PE platforms, and family offices — within 48 hours of a pitch meeting. The list should have 30–50 names with a clear rationale for each. A generic or obviously recycled list signals limited sector knowledge.

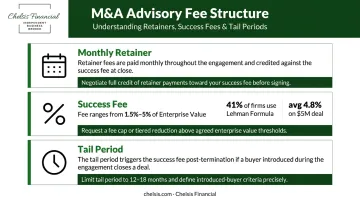

4. Fee Structure and Engagement Terms

Standard components include:

- Monthly retainer — typically credited against the success fee at close

- Success fee — ranges from roughly 1.5%–5% of enterprise value depending on deal size; the Firmex 2024–2025 North American M&A Fee Guide found the Lehman Formula used by 41% of firms, with an average success fee of 4.8% on a $5M deal

- Tail period — defines which buyers introduced during the engagement still trigger the success fee after termination

Negotiate the retainer credit, tighten the tail clause definition, and confirm clear termination rights before signing.

Business owners who haven't yet established a clear value baseline face a disadvantage in these conversations. Chelsis Financial's Complimentary Assessment of Value (a review of your financials, market benchmarks, and industry comparables) is a practical first step before entering advisory pitches. There's no cost, and it gives you a concrete number to anchor those early conversations.

2026 Market Trends Shaping Middle-Market M&A

PE Dry Powder and Deal Appetite

Global buyout dry powder stood at $1.2 trillion in 2024, with $282 billion classified as aging capital held four years or longer, according to Bain's Global Private Equity Report 2025. That aging capital creates deployment urgency for sponsors. For sellers in healthcare services, business services, or IT, that urgency means a more competitive buyer pool and stronger negotiating leverage.

The outlook from advisors themselves is clear: 72.6% of M&A advisors across 54 countries expect 2026 deal flow to increase, according to Capstone/IMAP's 2025–2026 Global M&A Trends Survey.

Recurring Revenue Commands Premium Multiples

With more capital chasing fewer quality deals, acquirers have shifted toward businesses with contractual or subscription-based revenue. The same Capstone/IMAP survey found that 66% of buyers identified recurring revenue as the top acquisition criterion in 2026 — even with a slight decline from the prior year, it remained the single most important factor by a wide margin.

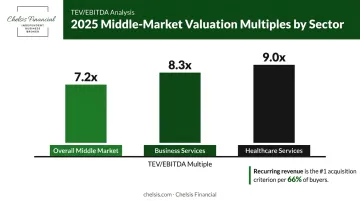

For middle-market sellers, this has direct valuation implications. According to GF Data benchmarks, average middle-market multiples in 2025 were approximately 7.2x TEV/EBITDA. Healthcare services reached 9.0x and business services hit 8.3x in Q1 2025 — both figures driven substantially by recurring revenue profiles.

Macroeconomic Headwinds Require Preparation

Geopolitical uncertainty, tariff policy, and market volatility remain real constraints. US M&A transactions under $500M declined approximately 13% year-over-year in H1 2025, according to CIBC's US Middle Market Monitor, citing tariff uncertainty as a primary factor.

Sellers who enter 2026 with:

- Three-plus years of clean, normalized financials

- Realistic valuation expectations anchored to current data

- No significant customer concentration or pending legal exposure

These factors don't guarantee a premium, but they substantially reduce the friction that causes deals to stall or reprice at closing.

Conclusion

Choosing an M&A advisory firm is not a brand decision. It is a sub-sector fit, deal-size match, and process quality decision — and it will directly determine the competitive tension (and therefore the final price) when the deal closes.

Shortlist two or three firms. Run structured pitches using consistent questions across all of them. Call references on closed deals in your specific sector and size range before signing any engagement letter.

If you're not yet sure what your business is worth, that's the right starting point. Chelsis Financial offers a Complimentary Assessment of Value — a no-obligation, confidential review of your business's financial performance, market positioning, and realistic value range. A clear value baseline means you negotiate from data, not assumption — and that shapes every advisor conversation that follows.

Reach out at 866-842-5151 or schedule a confidential call at calendly.com/chelsis/getanswers.

Frequently Asked Questions

What is a middle-market M&A advisory service?

A middle-market M&A advisory firm manages the full sell-side process for businesses typically valued between $10M and $500M — packaging the company, identifying strategic and financial buyers, running a competitive auction, and negotiating terms through closing. Unlike a broker, which lists and waits for inbound interest, an advisor actively builds buyer tension to maximize price.

How much do M&A advisory firms charge for middle-market deals?

The standard structure includes a monthly retainer (usually credited at close) plus a success fee of approximately 1.5%–5% of enterprise value — with Modified Lehman structures common in the lower middle market and flat percentages more typical above $25M EV. According to the Firmex 2024–2025 fee guide, 41% of firms still use the Lehman Formula.

What is the difference between an M&A advisor and a business broker?

A business broker lists a business and qualifies inbound buyers. An M&A advisor builds a targeted buyer list, produces institutional-grade marketing materials, runs a structured competitive process, and negotiates complex deal terms — skills that matter when PE firms or strategic acquirers are at the table. Brokers fit sub-$2M transactions; M&A advisors belong above that threshold.

How long does a middle-market M&A process typically take?

A sell-side engagement typically runs six to twelve months from kickoff to closing wire: preparation (6–12 weeks), buyer outreach and IOI collection (4–8 weeks), management meetings and LOI negotiation (4–6 weeks), and confirmatory diligence through definitive agreement (8–16 weeks).

What EBITDA multiples can middle-market business owners expect in 2026?

GF Data benchmarks put the 2025 average at approximately 7.2x TEV/EBITDA across middle-market transactions, with healthcare services reaching 9.0x and business services at 8.3x in Q1 2025. Quality platforms with recurring revenue, strong margins, and defensible customer relationships consistently command above-average multiples within their sector.

How do I know if my business is ready for an M&A advisory engagement?

Readiness typically requires:

- Three-plus years of clean, normalized financials

- No single customer representing more than 15–20% of revenue

- A management team that can run operations through a six-to-twelve month process

A complimentary business value assessment — Chelsis Financial provides one at no cost — is a practical first step to gauge where you stand before engaging an advisor.