This is where sell-side advisory changes the equation.

A skilled sell-side advisor levels that playing field: handling valuation, buyer outreach, negotiations, and due diligence while the owner stays focused on running the business. According to the Exit Planning Institute, only 20% to 30% of businesses that go to market actually sell — often because owners underestimate how much preparation and professional guidance the process requires.

This guide covers what sell-side advisory is, what advisors actually do, how the process works step by step, and how to choose the right firm for your exit.

TL;DR

- Sell-side advisors represent business owners exclusively, managing everything from valuation to closing

- The process typically spans six months to over a year, depending on business readiness and deal complexity

- Advisors protect confidentiality, qualify buyers, and negotiate deal structure — including terms beyond the headline price

- Hiring an advisor well before going to market dramatically improves preparation and outcomes

- Chelsis Financial's complimentary Assessment of Value provides a low-commitment way to understand where your business stands

What Is Sell-Side Advisory?

Sell-side advisory covers the professional services provided to a business owner who wants to sell their company. The advisor — whether an M&A firm, investment bank, or business broker — manages the entire transaction: valuation, buyer outreach, negotiation, due diligence, and closing.

Who It's For

This isn't a service for startups seeking funding or real estate investors. Sell-side advisors work with owners of established, operating businesses — typically those approaching retirement, a life transition, or a strategic inflection point where a sale makes sense. The IBBA defines transactions below roughly $2M as the domain of business brokers, while deals in the $2M–$50M lower middle market are typically handled by M&A advisors.

What Sets It Apart from Other Advisory Services

General business consultants advise on operations. Attorneys advise on legal exposure. Sell-side advisors focus on one thing: getting the deal done on terms that serve the seller.

What makes them different in practice:

- Scope is transaction-specific — the engagement begins when you decide to sell and ends at closing

- Represents the seller's interests exclusively, not a neutral third party

- Compensation is tied to a successful closing, aligning incentives with the owner's outcome

- Controls information flow throughout, something general consultants never manage

The advisor's job is to maximize sale price, protect confidentiality, and close on terms that match what the owner actually cares about — not just the number on the cover sheet.

What Does a Sell-Side Advisor Do?

The role spans the entire transaction lifecycle. "Finding buyers" is only one part of it.

Preparing the Business and Valuation

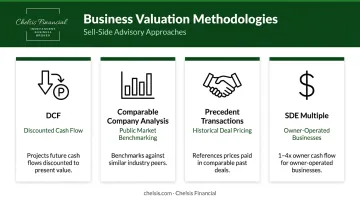

Before any buyer sees the business, the advisor conducts a thorough valuation. Common methodologies include:

- Discounted cash flow (DCF) — estimates value based on projected future cash flows discounted to present value

- Comparable company analysis — benchmarks the business against similar companies in the same industry

- Precedent transaction analysis — looks at prices paid in past deals for comparable businesses

For smaller owner-operated businesses, Seller's Discretionary Earnings (SDE) is often the primary metric, with typical multiples ranging from one to four times annual owner cash flow.

Financial normalization is equally important. Advisors recast financial statements to reflect true business performance — removing one-time expenses, owner perks, and non-recurring items. This adjusted view, sometimes called a "recasted" P&L or SDE statement, is what serious buyers actually evaluate.

Marketing to Qualified Buyers

Advisors develop a staged set of marketing materials:

- Blind teaser — introduces the opportunity without revealing the company's identity

- NDA — the gate a buyer must pass before receiving detailed information

- Confidential Information Memorandum (CIM) — the full story of the business, typically 50+ pages covering financials, operations, market position, and growth potential

From there, advisors manage buyer outreach — either through a targeted approach (a curated list of high-fit buyers) or a broader competitive process designed to create leverage. Either way, the advisor screens buyers for financial capability and genuine interest, filtering out tire-kickers before they consume the owner's time.

Negotiating and Closing the Deal

When offers arrive — first as Indications of Interest (IOIs), then as Letters of Intent (LOIs) — the advisor evaluates them on a structure-adjusted basis. Headline price rarely tells the full story. Structure matters just as much:

- Contingent payments tied to future performance (earnouts) reduce guaranteed proceeds

- Seller financing requirements shift risk back onto the owner

- Post-close transition obligations can extend the seller's involvement for months or years

- Representations and warranties clauses determine how much liability the seller retains

Through due diligence and final negotiations, the advisor coordinates seller responses, keeps the process on schedule, and guards against retrading — the tactic where buyers use due diligence findings to push for last-minute price reductions. The best protection is proactive disclosure upfront. Surprises erode trust; transparency keeps deals on track.

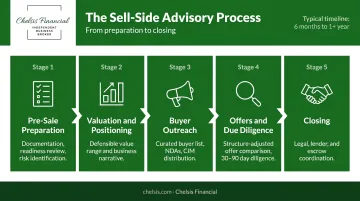

The Sell-Side Advisory Process Step by Step

The full process — from initial engagement through closing — typically spans six months to over a year, according to BizBuySell's research. For lower middle-market deals ($5M–$50M), the IBBA/M&A Source Q2 2024 Market Pulse reported a median time to close of nine months.

Each stage builds on the last. Skipping or rushing early stages is a primary reason deals fall apart.

Stage 1 — Pre-Sale Preparation

Before going to market, the advisor conducts a readiness review. At Chelsis Financial, this means assembling a complete documentation package covering:

- Three years of financial statements and tax returns

- Owner benefit analysis

- Lease agreements and vendor contracts

- Customer concentration data

- Transition support plans

Customer concentration gets particular attention. If a single customer accounts for more than 15% of revenue, that risk needs to be addressed — or structured around — before any buyer sees it.

Stage 2 — Valuation and Positioning

The advisor develops a defensible valuation range and builds the business's narrative: growth trajectory, competitive advantages, operational strengths, and future potential. This story must support the asking price — not just assert it.

Chelsis Financial provides a Complimentary Assessment of Value at this stage, reviewing formal financial statements from the current year and previous three years before any engagement formally begins.

Stage 3 — Buyer Outreach and Marketing

The advisor builds a curated buyer list across three categories: strategic acquirers, private equity groups, and qualified individual buyers. From there, they manage NDA execution, distribute the CIM, and field Q&A with interested parties. The goal is to generate competitive interest while keeping the process tightly controlled.

Stage 4 — Offers, Negotiation, and Due Diligence

Once IOIs and LOIs arrive, the advisor compares them on a structure-adjusted basis. A higher headline price loaded with earnouts and seller financing can be worth less than a cleaner offer at a lower number.

Due diligence typically runs 30–90 days. A good advisor keeps weekly check-ins on the calendar, treats buyer requests as urgent, and watches the clock — deals that drag past the agreed timeline rarely recover momentum.

Stage 5 — Closing

The final stage involves coordinating with legal counsel, lenders, CPAs, and escrow agents to satisfy every closing condition. The advisor tracks each open item in sequence — title work, financing confirmations, final representations — so no single dependency stalls the close.

Key Benefits of Sell-Side Advisory for Business Owners

Higher Sale Price Through Preparation and Competition

Advisors create competition among buyers — and competitive processes produce better outcomes than one-on-one negotiations. Beyond price, advisors catch structural issues that would otherwise surface during due diligence and reduce the final number. Sellers who show up prepared close deals; those who don't often watch valuations erode in the final stretch.

According to M&A Source, a qualified advisor assignment requires 400 to 800 working hours or more on a typical engagement. That work isn't just administrative — it's strategic.

Time and Bandwidth

Managing a sale without an advisor adds significant hours per week to the owner's workload at exactly the wrong moment: the period when the business needs the most attention. Revenue softness during a sale process is one of the fastest ways to undermine a deal's value.

An advisor takes on the process work — buyer calls, document requests, offer comparisons, legal coordination — while the owner keeps the business performing.

Confidentiality Protection

A confidentiality breach can damage a business before it sells. As CABB notes, once confidentiality is breached, the damage can be difficult or impossible to contain. Employees start looking for other jobs. Customers get nervous. Competitors exploit the uncertainty.

A good advisor controls information flow through staged disclosure — teaser, NDA, CIM — so only qualified, vetted buyers receive sensitive details. That discipline around information is what keeps a sale from unraveling before it closes. At Chelsis Financial, every interaction — from first contact through closing — is held in strict confidence, by design.

Sell-Side vs. Buy-Side Advisory: Key Differences

| Sell-Side Advisor | Buy-Side Advisor | |

|---|---|---|

| Represents | The seller | The acquirer |

| Primary goal | Maximize sale price and terms | Minimize purchase price and risk |

| Creates | CIM, teasers, buyer outreach | Target lists, valuation analysis |

| Manages | Confidentiality, competitive process | Diligence, deal sourcing |

In most transactions, both parties have independent representation. That independence means your advisor's incentives are fully aligned with your outcome — negotiating on your behalf, not simply facilitating a deal that closes.

One scenario worth understanding: some intermediaries work "two-sided," representing both buyer and seller in the same transaction. This creates a direct conflict of interest — advisors with established buy-side relationships may prioritize repeat acquirer clients over a one-time seller.

Before signing any advisory agreement, ask directly: who does this advisor represent in this transaction?

How to Choose the Right Sell-Side Advisor

What to Evaluate

- Relevant deal experience — have they closed transactions in your industry and deal size range?

- Buyer network depth — do they have real relationships with qualified buyers, or just a database?

- Confidentiality protocols — how do they prevent premature disclosure to employees, customers, and competitors?

- Fee structure — is there a retainer, a success fee, or both? How is the success fee calculated?

- Senior advisor involvement — will you work with experienced principals throughout, or get handed to junior staff after signing?

Questions to Ask Prospective Advisors

Before committing, ask:

- How will you value my business, and what methodology will you use?

- How will you find and qualify buyers — what does your network actually look like?

- How will you compare offers beyond headline price?

- What's your realistic timeline for a business like mine?

- What's your process for maintaining confidentiality throughout?

M&A Source recommends business owners begin planning three to five years before their intended transition date — not to delay the process, but to give the advisor time to prepare the business properly.

Working with Chelsis Financial

If you're evaluating advisors in the Midwest, Chelsis Financial works with established businesses across manufacturing, industrial services, healthcare, technology, and distribution — primarily in Indiana and Michigan. The firm has facilitated transactions ranging from sub-$1M to multi-million-dollar deals across sectors including metal fabrication, healthcare SaaS, automotive services, and aerospace manufacturing.

What distinguishes the firm is a Complimentary Assessment of Value — a clear, independently validated picture of what your business is worth before any engagement begins. Backed by a network of over 2,000 businesses, it's a concrete starting point for owners who want to understand their options without committing upfront.

To schedule a confidential conversation, contact C. Ross Hedges at 866-842-5151 or visit calendly.com/chelsis/getanswers.

Frequently Asked Questions

What is a sell-side advisory agreement?

A formal contract between a business owner and their advisor defining the scope of services, fee structure, exclusivity terms, and the conditions under which the advisor earns their fee. It typically includes a retainer or engagement fee plus a success fee payable at closing.

How much does sell-side advisory cost?

Most advisors charge a monthly retainer ($5,000–$10,000 is common) plus a success fee at closing. According to Firmex's M&A Fee Guide, average success fees run approximately 6.3% on a $5M transaction and 3.9% on a $20M deal. Many firms deduct collected retainer fees from the final success fee.

How long does the sell-side advisory process take?

From preparation through closing, the full process typically takes six months to over a year. Business readiness, buyer demand, deal complexity, and financing conditions all affect timing. Lower middle-market deals in the $5M–$50M range averaged nine months to close in 2024.

What is the difference between sell-side and buy-side advisory?

Sell-side advisors represent the seller and work to maximize sale price and terms. Buy-side advisors represent the acquirer and work to minimize cost and risk. Each advisor works exclusively in their client's interest — roles and incentives never overlap.

When should I hire a sell-side advisor?

Well before you plan to go to market — years in advance if possible. Early engagement lets the advisor assess readiness, close documentation gaps, reduce owner dependence, and shape the business narrative before buyers ever see it.

Do I need a sell-side advisor to sell my business?

Owners can attempt a self-directed sale, but valuation, buyer qualification, negotiation, and due diligence are each complex disciplines. Buyers and their advisors typically have far more transaction experience than a first-time seller. Professional representation matters most when confidentiality and final value are at stake.