That's a costly mistake. The IRS treats seller-financed transactions in ways that can either work strongly in your favor or create significant surprise liabilities at closing — depending entirely on how the deal is structured.

This article covers what both parties need to understand: how installment sale tax treatment works for sellers, what buyers can and can't deduct, the financial benefits that make seller financing worth considering, and how to structure a deal that serves both sides before attorneys start drafting documents.

TL;DR

- Sellers can spread capital gains taxes over the note's life using the IRS installment sale method (IRC Section 453) — avoiding a large lump-sum tax bill

- Depreciation recapture must be recognized as ordinary income in the year of sale, regardless of installment reporting

- Interest income the seller earns on the note is taxed as ordinary income, not at capital gains rates

- Buyers can deduct interest paid on a seller note as a business expense

- Purchase price allocation directly shapes a buyer's future depreciation deductions — structure it carefully

- Both parties often benefit through higher sale prices, faster closings, and more flexibility than bank financing allows

What Is Seller Financing in a Business Acquisition?

In a seller-financed deal, the seller acts as the lender. The buyer provides a down payment at closing, and the remaining balance is paid in structured installments over an agreed period — typically 5 to 7 years at 8% to 10% interest, according to BizBuySell's seller financing guidance.

The financed portion is documented in a promissory note — a legally binding agreement specifying the payment schedule, interest rate, and default terms. The seller typically holds a security interest in the business assets as collateral, perfected through a UCC financing statement filed with the state.

In Chelsis Financial's experience brokering business sales across manufacturing, industrial, healthcare, and technology sectors in the Midwest, seller financing typically covers 10% to 30% of the purchase price over 3 to 5 years. This structure bridges financing gaps common in business acquisitions and signals seller confidence in the business's future — a meaningful assurance for buyers committing significant capital.

That confidence resonates broadly. According to BizBuySell's Insight Report, 61% of buyers hope seller financing will be included in a deal, with 32% calling it very important and 20% calling it extremely important. Sellers who understand the financial and tax consequences before signing are far better positioned to negotiate terms that protect their interests.

Tax Implications for Sellers: The Installment Sale Method

Seller financing carries real tax advantages for sellers — but also a few traps that catch even experienced business owners off guard. Understanding both is essential before structuring the deal.

How the Installment Sale Method Works

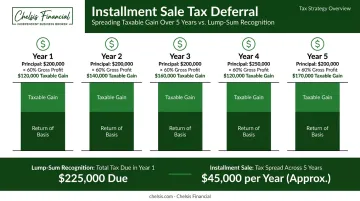

Under IRC Section 453 and IRS Publication 537, an installment sale is any sale where the seller receives at least one payment after the tax year of sale. If the transaction qualifies, the seller reports a proportional share of the gain with each principal payment received — rather than the full gain in the year of closing.

This treatment is automatic unless the seller elects out.

The gross profit percentage is the calculation that drives everything. The IRS defines it as:

Gross Profit ÷ Contract Price = Gross Profit Percentage

This percentage is applied to every principal payment received. For example, if the gross profit percentage is 60%, then 60 cents of every dollar of principal is treated as taxable gain. The remaining 40 cents is a return of basis and not taxable.

Over a 5-year note, this spreads the tax liability across five tax years — which can keep the seller in a lower bracket each year compared to recognizing the full gain at once.

The Depreciation Recapture Exception

Depreciation recapture cannot be deferred — and this is the provision that catches sellers off guard most often.

Any depreciation previously claimed on business assets — equipment, machinery, leasehold improvements — must be recognized as ordinary income in the year of sale under IRC Sections 1245 and 1250, even if no cash payment is received that year. This recapture income is taxed at ordinary income rates, which can reach 37% federally, not the more favorable capital gains rates.

Sellers who have claimed significant depreciation on equipment-heavy businesses — manufacturing, automotive, industrial contracting — need to model this liability before setting their asking price. Chelsis Financial treats this as a required step in deal preparation, not an afterthought.

Interest Income and the AFR Requirement

Interest received on the seller note is taxed as ordinary income, reported annually regardless of when principal is received.

The note must also carry an interest rate at or above the IRS Applicable Federal Rate (AFR). For June 2026, the IRS has set:

| Note Term | AFR |

|---|---|

| 3 years or less | 3.85% |

| Over 3 years, up to 9 years | 4.13% |

| Over 9 years | 4.87% |

If the stated rate falls below the applicable AFR, the IRS can impute interest — recharacterizing part of the purchase price as interest income, which negatively affects both parties' tax positions.

When to Consider Electing Out of Installment Reporting

AFR compliance is one piece of a larger decision: whether installment reporting even makes sense for the seller's situation. There are scenarios where electing out produces a better outcome:

- They expect their tax rate to increase in future years

- They have capital loss carryforwards available to offset the gain now

- They need the liquidity from a lump-sum payment

This decision should be modeled by a CPA before the deal closes, not after.

Tax Implications for Buyers in a Seller-Financed Deal

Interest Deductibility

Buyers can generally deduct interest paid on a seller note as a business interest expense, reducing taxable income and lowering the effective cost of the financing below the stated rate. However, deductibility depends on the business's tax structure, and under IRC Section 163(j), deductible business interest expense generally cannot exceed 30% of adjusted taxable income for larger operations. A tax advisor should confirm the buyer's specific deductibility position.

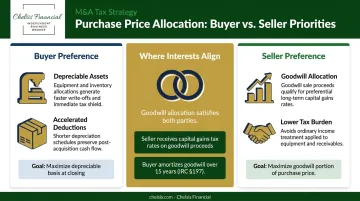

Purchase Price Allocation (Form 8594)

In an asset sale — the most common structure for small business acquisitions — both buyer and seller must complete IRS Form 8594 under Section 1060. The form allocates the total purchase price across asset classes, from tangible equipment to goodwill.

This allocation isn't just paperwork. It directly determines:

- The buyer's depreciation schedule and future tax deductions

- The seller's tax treatment on each component of the sale price

The two parties typically have opposing preferences:

| Party | Preference | Reason |

|---|---|---|

| Buyer | More to depreciable assets (equipment, inventory) | Faster write-offs |

| Seller | More to goodwill | Capital gains treatment |

Allocating more to goodwill can benefit both parties: sellers receive capital gains rates, while buyers amortize goodwill over 15 years — making it one of the few allocation decisions where interests genuinely align.

Asset Sale vs. Stock Sale

The choice of structure has major tax consequences for the buyer:

- Asset sale: Buyer receives fair-market-value basis in acquired assets, enabling higher depreciation and amortization deductions going forward

- Stock sale: Buyer receives outside basis in the stock; the company's assets retain their historical carryover basis — no step-up, no accelerated depreciation

Asset sales are standard in lower mid-market transactions because buyers strongly prefer the step-up in basis and the ability to control which liabilities they assume.

Key Benefits of Seller Financing for Both Parties

Seller Benefits

Higher sale price. BizBuySell notes that seller financing attracts a larger pool of serious buyers and can support a higher asking price. Chelsis Financial's experience confirms this: sellers who offer financing tend to close faster and at better valuations because the structure expands the buyer pool and reduces transaction friction.

Tax deferral across brackets. Installment reporting spreads recognized gain across multiple years instead of triggering a lump-sum tax hit. A seller with a $2M gain paid over a 5-year note may stay below bracket thresholds that a single-year recognition would cross.

Ongoing interest income. Seller notes at 8%–10% compare favorably to conventional savings instruments. FDIC national rates as of May 2026 showed money market accounts at 0.57% and 6-month CDs at 1.35%. A secured seller note backed by a business the seller knows well offers a considerably higher yield, though it carries illiquidity risk those alternatives don't.

Buyer Benefits

Lower capital barrier. Seller financing reduces the upfront requirement and cuts or eliminates the need to qualify for a third-party bank loan — a real advantage when rates are high and lender standards tighten.

Built-in seller alignment. When a seller carries part of the note, they have a direct financial stake in the buyer's success. That typically translates to more thorough training, warmer client introductions, and operational context that a fully cashed-out seller has little reason to provide.

How to Structure a Seller-Financed Deal to Maximize Tax Benefits

Key Terms and Their Tax Impact

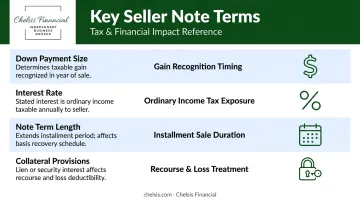

Every term in the seller note carries tax and financial consequences:

- Down payment size — affects the seller's installment ratio and how much basis is recovered early; larger down payments reduce the seller's ongoing note risk

- Interest rate — must meet or exceed the IRS AFR to avoid imputed interest issues (see rates above)

- Note term length — longer terms mean more tax deferral for sellers, but more total interest cost for buyers

- Collateral provisions — a UCC financing statement perfects the seller's security interest in the business assets, giving the seller lien priority if the buyer defaults

Chelsis Financial typically structures seller note terms between 3 and 5 years, balancing deferral benefits for sellers with manageable repayment timelines for buyers.

Get the Right Professionals Involved

No seller-financed deal should be finalized without two professionals in the room:

- A qualified CPA — to model the tax outcomes of different structures, calculate the depreciation recapture exposure, and determine whether installment reporting or an election out is more advantageous

- A business attorney — to draft the promissory note, security agreement, and file the UCC financing statement correctly

A business broker like Chelsis Financial helps sellers and buyers align on deal terms before legal and tax professionals finalize the documents. The firm guides both parties through purchase price allocation, financing structure, and term negotiations so both sides reach closing with a clear, agreed-upon structure.

Note Transferability

Sellers who need liquidity after closing have the option to sell their promissory note to a third-party investor — typically at a discount to face value. This should be specified in the note's transferability language at drafting. Under UCC Article 3, a negotiable instrument can be transferred by endorsement and delivery, and under UCC Section 9-310, assigning a perfected security interest doesn't require a new UCC filing to maintain perfected status.

Frequently Asked Questions

How do you negotiate seller financing?

Buyers should present strong financial qualifications — credit history, business experience, and personal financial statements — to reduce the seller's perceived risk. Both parties need to align on down payment, interest rate, term length, and collateral before attorneys draft documents. A business broker can facilitate these conversations and keep negotiations on track.

How do you finance a small business acquisition?

The main options are seller financing, SBA 7(a) loans (up to $5M), SBA 504 loans (for fixed assets, up to $5.5M), traditional bank loans, and private credit. Many deals combine approaches — seller financing filling the gap between a bank loan and the purchase price, sometimes structured as a standby note when SBA financing is involved.

Is seller financing complicated?

The basic concept is simple: the seller acts as the lender and receives installment payments over time. The tax and legal details — installment sale elections, depreciation recapture treatment, purchase price allocation, and promissory note drafting — require professional guidance to handle correctly.

When seller financing is used, what does the seller become?

The seller becomes the creditor, holding a promissory note and typically a security interest (UCC lien) in the business assets — similar to how a bank holds a lien on collateral for a commercial loan.

Does seller financing allow sellers to defer capital gains taxes?

Yes. Under IRC Section 453, sellers using the installment method report and pay capital gains tax only as principal payments are received. The exception is depreciation recapture, which is fully due as ordinary income in the year of sale.

What happens if a buyer defaults on a seller-financed loan?

The seller can typically repossess the business under the security agreement and UCC lien. This process is complex and costly, which is why requiring a substantial down payment and carefully vetting the buyer's qualifications before closing is essential for any seller who carries a note.