The stakes are real — emotionally and financially. You've built something, and now you're navigating unfamiliar territory: valuations, buyer negotiations, legal documents, and tax structures that can reshape your net proceeds significantly.

This guide covers every major phase of a successful sale — from early preparation and accurate valuation to finding qualified buyers, managing legal documents, and closing with confidence.

TL;DR

- Start preparing 12–36 months before listing — buyers pay more for businesses with clean financials and reduced owner dependency

- Use size-specific valuation multiples: SDE multiples range from 2.3x (under $500K) to 3.0x (businesses in the $1M–$2M range)

- Qualified buyers close deals; volume doesn't — a screened buyer network cuts months off your timeline

- Four documents are required at every closing: NDA, LOI, Asset or Stock Purchase Agreement, and Disclosure Schedules

- Tax structure matters as much as price — consult a CPA before agreeing to any deal structure

Preparing Your Business for Sale

The Exit Planning Institute reports that only 20–30% of businesses that go to market actually sell. The gap between listing and closing isn't usually about market conditions — it's about preparation.

Sellers who address weaknesses before listing have time to improve financial records, reduce owner dependency, and build the kind of operational continuity that buyers pay a premium for. Those who list without preparation often find buyers walking away during due diligence.

Are You Selling a Business or a Job?

This is the first question serious buyers ask — even if they don't say it out loud.

A business that runs on systems, trained staff, and documented processes is worth far more than one that runs on the owner's daily presence. BizBuySell notes that high owner dependency reduces a business's attractiveness because buyers look for continuity that doesn't hinge on a single individual.

Ask yourself:

- Are core processes documented, or do they live in your head?

- Can client relationships transfer to a new owner or key employee?

- Is there at least one layer of management between you and daily operations?

If the answer to any of these is "no," that's where preparation starts. Chelsis Financial works with sellers specifically on this transition — helping owners build management infrastructure and stabilize customer relationships before a business ever goes to market.

Get Your Financials in Order

Operational readiness matters, but financial clarity is what moves deals forward. Buyers and their accountants will review 3–5 years of records. What they want to see:

- Profit and loss statements

- Tax returns (matching your P&Ls)

- Balance sheets

- A clear statement of Seller's Discretionary Earnings (SDE)

Gaps, inconsistencies, or unexplained anomalies in any of these documents will stop a deal in its tracks — often during due diligence, when it's too late to recover.

Adjusted EBITDA and SDE "add-backs" are worth understanding before you list. They normalize your financials by removing owner perks, one-time expenses, or personal items run through the business — giving buyers a clearer picture of true profitability. A business generating $400,000 in reported net income may show $550,000 in SDE once legitimate add-backs are calculated.

Reduce Owner Dependency and Strengthen Operations

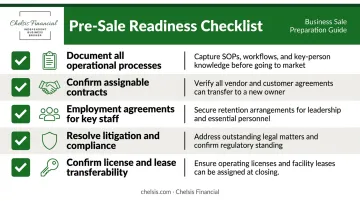

Before listing, work through this pre-sale checklist:

- Document all operational processes

- Ensure key customer and supplier contracts are assignable

- Put employment agreements with key staff in place

- Resolve any pending litigation or compliance issues

- Confirm that licenses and leases can transfer to a new owner

How to Value Your Business Accurately

Pricing a business is where emotion and data collide, and emotion rarely wins. Sellers often overestimate value because they're measuring years of effort rather than what a buyer can realistically earn from the investment. Underpricing is equally damaging. Neither extreme attracts serious, qualified buyers.

A professional valuation creates the credible, data-backed asking price that makes negotiations productive rather than adversarial.

The Three Primary Valuation Methods

Income Approach values a business on its future earning potential, adjusted for risk. It's the most commonly used method for profitable, operating businesses.

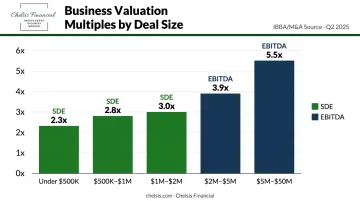

Current market data from the IBBA/M&A Source Q2 2025 Market Pulse shows median SDE and EBITDA multiples by deal size:

| Enterprise Value | Metric | Median Multiple |

|---|---|---|

| Under $500K | SDE | 2.3x |

| $500K – $1M | SDE | 2.8x |

| $1M – $2M | SDE | 3.0x |

| $2M – $5M | EBITDA | 3.9x |

| $5M – $50M | EBITDA | 5.5x |

The Market Approach compares your business to similar companies that have recently sold in the same industry and region. This grounds your asking price in what buyers are actually paying — not what sellers wish they could get.

The Asset Approach calculates value by subtracting total liabilities from total assets, both tangible and intangible. Use this method for asset-heavy businesses or those with limited profitability, where balance sheet value outweighs earnings potential.

Don't Overlook Intangible Assets

Hard assets tell part of the story. What's often worth more is what doesn't appear on the balance sheet:

- Brand reputation and market recognition

- Loyal customer relationships and recurring revenue

- Proprietary processes or intellectual property

- Long-term contracts with established accounts

Consider a manufacturing business with $800,000 in equipment and a 15-year relationship with a regional distributor generating 60% of revenue. That customer relationship, documented and transferable, can push the valuation well above what equipment alone would suggest.

This is what accountants call goodwill. It's real, it's negotiable, and it belongs in your asking price.

Quantifying goodwill accurately alongside hard assets is where professional valuation pays for itself. Chelsis Financial's Complimentary Assessment of Value is a practical starting point for owners who want a professional estimate before committing to a sale. The process requires 3–4 years of financial statements and is conducted under strict confidentiality. It's a low-risk way to understand what your business is worth before you decide anything.

Finding the Right Buyer

Volume of inquiries is not the goal. One serious, financially qualified buyer who closes is worth more than fifty tire-kickers who waste months of your time.

Types of Buyers and What Motivates Them

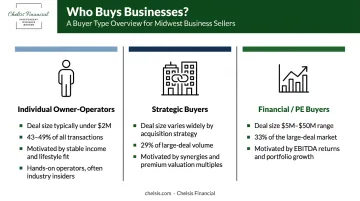

Three buyer types dominate the market, and each one evaluates your business through a different lens:

| Buyer Type | Typical Deal Size | Primary Motivation | What They'll Pay For |

|---|---|---|---|

| Individual owner-operators (first-time buyers) | Under $2M | Stable, transferable income | Consistent cash flow, low owner dependency |

| Strategic buyers (competitors, adjacent industries) | Varies | Synergies — customers, geography, capabilities | Access to what they can't build quickly |

| Financial buyers (PE groups, private investors) | $5M–$50M | Return on investment | EBITDA multiples and growth potential |

Per Q2 2025 Market Pulse data, individual buyers represent 43–49% of transactions under $2M. In the $5M–$50M range, PE add-on buyers hold 33% of the market; strategic buyers account for 29%. Strategic buyers often pay the highest multiples because an acquisition adds more value to their existing operation than the standalone earnings suggest.

Knowing which buyer type is likely to pursue your business shapes everything — how you position financials, which terms matter most, and how you market confidentially.

Marketing Your Business Confidentially

Listing your business publicly before a deal closes can damage what you're trying to sell. Employees may leave. Customers may shop elsewhere. Competitors can use the information against you.

Professional confidential marketing works through:

- Blind listings that describe the business category, revenue, and location without identifying details

- NDA-first protocols — no financials or operational details are shared until a buyer has signed a confidentiality agreement

- Selective outreach to pre-screened buyer candidates

Chelsis Financial markets through a registry of pre-qualified buyers, producing blind summaries and Confidential Information Memorandums (CIMs) that go only to vetted, NDA-signed candidates. Your identity stays protected at every stage — so the business keeps running normally while the process moves forward.

Key Legal Documents You Need

Legal paperwork is where deals progress cleanly or stall. Four documents drive most transactions — each one triggered at a specific stage, and each one carrying real consequences if handled poorly.

Non-Disclosure Agreement (NDA)

Before sharing financials, client lists, or any operational detail, a signed NDA must be in place. It prohibits the buyer from misusing or disclosing confidential information — even if the deal falls through.

Letter of Intent (LOI)

A non-binding document that establishes the key deal terms: price, payment structure, what's included, and a proposed timeline. Most LOIs include a "no shop" clause — a period during which the seller pauses discussions with other buyers while due diligence proceeds. Once signed, negotiating leverage shifts toward the buyer, so terms matter before you agree to exclusivity.

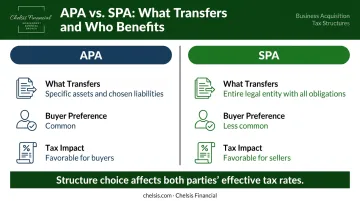

Asset Purchase Agreement (APA) vs. Stock Purchase Agreement (SPA)

This is one of the most consequential structural decisions in any transaction. The two approaches differ significantly in what transfers and who bears the risk:

| APA | SPA | |

|---|---|---|

| What transfers | Specific assets and liabilities chosen by the buyer | The entire legal entity — all contracts, obligations, and liabilities |

| Buyer preference | Common — buyer avoids inheriting unknown legacy liabilities | Less common unless contracts or licenses can't be reassigned |

| Tax impact | Generally favorable for buyers | Often more favorable for sellers |

Both sides face major tax consequences depending on the structure. An attorney should help determine the right fit before terms are finalized.

Disclosure Schedules

Detailed attachments to the purchase agreement listing all contracts, liabilities, pending litigation, and employee agreements — a full accounting of what the buyer is acquiring.

Transition Agreements

These outline the seller's post-closing role, training responsibilities, and any ongoing obligations. A clear transition agreement protects both sides and keeps operations stable after the handoff.

Navigating the Closing Process

Due Diligence: What Buyers Are Really Looking For

Due diligence is the buyer's formal verification of everything the seller has represented. It covers:

- Financial records and tax returns

- Customer concentration and contract stability

- Legal compliance and pending claims

- Operational systems and key personnel

- Lease terms, licenses, and transferability of contracts

Each of these areas requires organized, accessible documentation. Sellers who consolidate records in a virtual data room (VDR) move through this phase faster and with fewer re-negotiations. Chelsis Financial recommends a proper VDR over shared drives: it provides controlled access, version tracking, and a clear audit trail — so buyers aren't waiting on documents and sellers aren't losing negotiating ground over disorganization.

One practical warning: due diligence is when most deals get renegotiated. Disclose known issues upfront rather than letting buyers find them mid-process. A surprise uncovered during diligence gives buyers far more leverage than the same issue disclosed at the outset.

What Happens at Closing

The closing process follows a predictable sequence:

- All pre-conditions (financing, regulatory approvals, lease assignments) are confirmed

- Final documents are reviewed and signed by all parties

- Ownership transfers and funds are disbursed

- Post-closing obligations activate: non-compete period, seller training, and any seller-financed note payment schedule begins

Per Q2 2025 Market Pulse data, typical engagement-to-close timelines run 6 months for businesses under $500K, 8–9 months for $500K–$2M, and 9 months for $2M–$5M.

Starting license transfers, lease assignments, and regulatory filings early — before closing conditions are fully confirmed — is the most reliable way to protect that timeline.

Tax Implications When Selling a Business

Asset Sale vs. Stock Sale: How Structure Affects Your Tax Bill

Deal structure isn't just a legal formality — it's a tax decision with real dollar consequences.

In an asset sale, the IRS treats each asset class separately under Form 8594. Inventory and equipment may be taxed as ordinary income; goodwill and intangibles typically qualify for capital gains treatment. The buyer gets a step-up in basis, which is why most buyers prefer asset sales.

In a stock sale, the seller generally receives long-term capital gains treatment on the full proceeds — which is more favorable for sellers. However, buyers typically push back against stock sales because they inherit all liabilities, known and unknown.

This creates a negotiating tension that often resolves through price adjustments or hybrid deal structures. Which structure you land on shapes your effective tax rate — and the difference can be significant.

2025 long-term capital gains rates per the IRS: 0% for taxable income up to $48,350 (single filers), 15% above that threshold up to $533,400, and 20% above $533,400.

Strategies to Reduce Your Tax Burden

Installment Sales

Rather than receiving the full proceeds at closing, sellers can spread payments over multiple years. IRS Publication 537 confirms that sellers report a portion of gain as each payment is received — which can keep annual taxable income in a lower bracket.

Qualified Small Business Stock (QSBS) Exclusions

Under Section 1202, sellers of qualifying C corporation stock held more than five years may exclude a portion of eligible gain. To qualify, the stock must have been acquired at original issue in a C corp with gross assets of $75M or less at issuance (the limit was $50M for stock issued on or before July 4, 2025).

Per 2025 IRS Schedule D instructions, the exclusion is also subject to per-issuer limits. Verify current rules with a CPA — 2025 legislation updated several Section 1202 provisions.

Qualified Opportunity Zone (QOZ) Investments

Eligible capital gains invested in a Qualified Opportunity Fund within 180 days can be deferred until an inclusion event or December 31, 2026, whichever comes first.

Once a deal is signed, most tax planning options close. Chelsis Financial works directly with sellers' tax professionals to model outcomes under different deal structures before terms are finalized.

Frequently Asked Questions

How do I avoid paying capital gains when selling a business?

Strategies like installment sales, Qualified Opportunity Zone investments, and QSBS exclusions can reduce or defer capital gains — but eligibility depends on business structure, deal terms, and holding period. Consult a tax advisor before agreeing on any deal structure.

What happens to contracts when selling a business?

Existing contracts — leases, supplier agreements, customer contracts — must be reviewed for assignability clauses. Some transfer automatically with the business; others require third-party consent. Confirm assignability before due diligence begins — waiting until that stage leaves too little time to resolve complications.

What are common reasons a contract can be voided?

Under U.S. law, contracts can be rescinded for fraud or material misrepresentation, material breach by either party, or mutual agreement. Full disclosure and M&A legal counsel from the outset are the most reliable defenses against any of these outcomes.

Do I need a business broker to sell my business?

Technically, no — but most owners sell a business once in their lifetime. Brokers bring a qualified buyer pool, confidential marketing, and negotiation experience that's hard to replicate on your own. That combination typically produces better terms and fewer deal-killing surprises late in the process.

How long does it typically take to sell a business?

According to Q2 2025 Market Pulse data, most small business sales take 6–9 months from engagement to close for businesses under $5M. Sellers with clean financials and organized documentation move through due diligence faster and with fewer re-negotiations.

What is the difference between an asset sale and a stock sale?

In an asset sale, the buyer acquires specific assets and chosen liabilities — favorable for buyers avoiding legacy exposure. In a stock sale, the buyer acquires the entire entity including all obligations. The tax treatment differs significantly for both parties, making this a decision that requires input from both an attorney and a CPA.