This guide is for business owners considering a sale, buyers seeking acquisitions, and anyone navigating the mid-market space who wants a practical framework rather than generic advice. Whether you're the one writing the check or cashing it, the same disciplined practices separate deals that close from those that collapse.

The 10 best practices below are grouped into five strategic areas: building your thesis, assembling your team, executing due diligence, structuring the deal, and planning integration. Work through them in order — each builds on the last.

TL;DR: 10 Best Practices at a Glance

TL;DR: Key Takeaways

- Define a clear M&A strategy before approaching any deal — your thesis drives every downstream decision

- Assemble your deal team and secure a professional business valuation before going to market

- Conduct layered due diligence across financials, operations, culture, and documentation — cutting corners here is where deals collapse

- Structure transactions thoughtfully, with terms that reflect true business value

- Protect confidentiality throughout the process — from first contact through closing

- Build your post-merger integration plan during due diligence, not after closing

Build a Clear M&A Strategy First

Practices 1 and 2: Define Your Thesis and Time Your Transaction

Every successful mid-market deal begins with a clearly articulated strategy. For buyers, that means a written investment thesis. For sellers, it means a defined exit objective. Without either, deals drift: synergies get negotiated away, timelines stretch, and both parties lose clarity on what success actually looks like.

Common motivations that drive mid-market transactions include:

- Revenue synergies through customer base or channel expansion

- Cost reduction via operational consolidation

- Geographic or product line expansion

- Access to technology, IP, or specialized talent

- Retirement, succession planning, or liquidity events

Understanding your own motivation matters because it determines which deal criteria are non-negotiable versus flexible.

Timing Is a Strategy, Not an Afterthought

For sellers, timing is one of the most impactful variables in the entire process. Research from NCMM indicates that deal readiness can take multiple years, and a Pepperdine study found that 67% of sellers did no advance planning or less than one year of preparation before going to market.

Owners who begin exit preparation two to three years ahead — with stable EBITDA growth, documented systems, and reduced owner dependency — consistently enter the market from a position of strength.

Chelsis Financial works with business owners well before they're ready to sell, helping them build value and reduce owner dependence through strategic preparation.

For buyers, economic conditions and financing availability are equally important timing signals. While 55% of middle-market dealmakers expected higher deal activity in 2024, actual PE-sponsored middle-market transactions through Q3 2025 dropped 27% versus the prior year — a clear reminder that acquisition intent and market execution don't always align.

That gap between intent and execution is exactly why strategy needs to stay flexible. If your rationale shifts mid-process — say, from acquiring supply chain capacity to acquiring a product line — your valuation assumptions and integration priorities must shift with it. Otherwise you're measuring success against the wrong benchmarks.

Assemble Your Expert Deal Team and Know Your Numbers

Practices 3 and 4: Build the Right Advisory Team and Secure a Professional Valuation

NCMM research found that 70% of mid-market acquirers had limited or no prior M&A experience, and 90% of sellers had little to no prior transaction experience. That gap is where deals get hurt.

An effective mid-market deal team has three non-negotiable members:

| Role | Primary Contribution |

|---|---|

| Business broker / M&A advisor | Process management, buyer/seller access, negotiation |

| Transaction attorney | Deal structure, reps and warranties, closing certainty |

| Accounting firm / financial advisor | Quality of earnings, tax structuring, financial diligence |

The absence of any one of these creates blind spots that experienced counterparties will find and exploit. Buyers bring professional deal teams to every transaction — sellers who don't match that sophistication routinely leave value on the table or accept terms they later regret.

Get Your Valuation Before You Go to Market

An independent, professional business valuation is the foundation of a credible sale process: not optional, not deferrable. Overvalued businesses repel qualified buyers. Undervalued ones shortchange sellers who spent decades building something.

Chelsis Financial offers a Complimentary Assessment of Value that reviews formal financial statements (P&Ls, cash flow, balance sheets, and seller's discretionary earnings) alongside market conditions and industry benchmarks. The goal is to establish a realistic asking price before the first buyer conversation — valuation gaps discovered mid-process rank among the most common deal killers.

The sell-side discipline around valuation has a direct buy-side counterpart: building proprietary deal flow rather than reacting to listed transactions. A proactive outreach strategy with clearly defined target criteria — size, sector, culture, growth profile — produces better fit, lower premiums, and quicker closing timelines than competitive auction processes.

One consistent pitfall applies to both sides: verbal agreements on organizational structure, staffing, or integration priorities. Document every commitment formally at every stage.

In mid-market deals, where process discipline is typically lighter, undocumented agreements create post-close disputes that damage both deal value and working relationships.

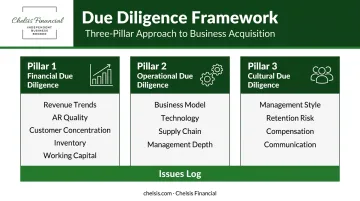

Execute Rigorous Due Diligence Across All Dimensions

Due diligence is where deals are won or lost — not at signing. Shallow diligence produces post-close surprises, and those surprises are expensive. Grant Thornton found that roughly half of all M&A deals experience accounting-related disputes, with Deloitte identifying purchase-price adjustments and earnout conflicts as the most common flashpoints.

Financial Due Diligence

The systematic review should cover:

- Revenue trends and EBITDA normalization

- Accounts receivable quality and collectability

- Customer concentration (anything above 20-30% concentration is a material risk)

- Inventory health and outstanding liabilities

- Working capital sufficiency and seasonal variability

Chelsis Financial's approach is direct: organized, defensible documentation is a signal of operational maturity. Sellers who enter due diligence with three years of fully reconciled P&Ls, balance sheets, and tax returns — plus a proper virtual data room — close faster and with fewer concessions.

Operational Due Diligence

Operational diligence must assess business model viability, technology systems, supply chain dependencies, and management depth. For founder-led and family-owned businesses — the dominant deal type in the mid-market — buyer confidence in post-close continuity often determines final pricing. Buyers specifically look for documented processes, distributed management responsibility, and evidence that operations don't hinge on a single person.

Cultural Due Diligence

Cultural diligence is not a soft afterthought. According to a 2023 Bain study, nearly half of M&A practitioners cited cultural fit or management team integration as a primary reason past deals failed — and 75% of acquirers still struggled with cultural issues despite making culture an early focus.

Assessments should address:

- Management style and decision-making norms

- Workforce expectations and retention risk

- Compensation structures and incentive alignment

- Communication patterns between leadership and staff

These belong in due diligence, not in the post-close retrospective.

Commercial diligence — how the target fits its market and where that market is heading — applies to single-purpose acquisitions as well. Strategic rationales evolve, and buyers who understand the target's competitive positioning can adapt more effectively.

Across every workstream, maintain a formal issues log that ranks risks by deal impact. Documentation gaps in the mid-market regularly produce post-close disputes that could have been avoided with a structured process.

Structure Deals Intelligently and Protect Confidentiality

Practices 8 and 9: Smart Deal Construction and Discretion Throughout

The headline purchase price is not the deal. The terms are.

Common mid-market deal structures and when to use them:

- Earnouts — bridge valuation gaps when buyer and seller disagree on future performance projections

- Rollover equity — align seller incentives post-close; common when buyers want key leadership retained

- Seller notes — provide financing flexibility and signal seller confidence in business continuity

- Working capital pegs — protect buyers against last-minute balance sheet manipulation before close

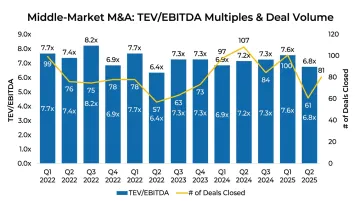

Financing conditions directly affect deal value. The $5M–$50M lower-middle-market median EBITDA multiple dropped from 6.1x to 5.4x between Q2 2022 and Q2 2023 as interest rates rose and 57-58% of advisors reported worsening lending conditions. Multiples have since stabilized — averaging 7.2x in H1 2025 for the lower middle market — but the lesson holds: financing assumptions must be stress-tested, not assumed.

Confidentiality Is a Business Asset

Deal structure decisions don't happen in a vacuum — they also depend on how well the process stays contained. Premature disclosure of a sale can unsettle employees, alert competitors, and cause customers to reconsider contracts, all before the deal closes. That's not a hypothetical risk; it's a recurring pattern in deals that lose value before they reach the finish line.

Effective confidentiality requires:

- NDAs executed before any business-specific information is shared

- Controlled buyer processes that limit access to qualified, serious parties

- An advisor with a pre-vetted buyer registry who can screen out unqualified parties and protect seller identity

For Chelsis Financial, this isn't a policy checkbox — it's how every engagement runs. Buyers must execute an NDA before accessing detailed business profiles, and outreach is directed at pre-screened buyers rather than broadcast to the open market.

Plan for Post-Merger Integration from Day One

Practice 10: Build Your Integration Plan During Due Diligence, Not After Closing

Bain's research found that when deals fail, integration is the root cause 83% of the time — and the firm's guidance is clear: start planning integration during diligence. McKinsey adds that companies managing culture effectively in integration planning are 50% more likely to meet or exceed synergy targets.

The core elements of a PMI plan that should be drafted in parallel with due diligence:

- Defined ownership of each integration workstream

- 30/60/100-day milestones with clear accountability

- Technology systems consolidation roadmap

- Cultural onboarding and communication plan for both workforces

- Retention plans for key employees identified during diligence

The People Imperative

In mid-market deals — particularly founder-led and family-owned businesses — the departure of key individuals post-close can eliminate the core value the buyer paid for. Chelsis Financial structures transition support plans as part of the documentation package, ranging from 30 days of seller availability to six months of part-time guidance depending on business complexity.

That approach reflects a broader principle: integration teams should be embedded during due diligence, not brought in after signing. Plans grounded in what diligence actually uncovered hold up under execution. Plans built on assumptions rarely do.

On the operational side, acquired businesses shouldn't be required to maintain back-office infrastructure that isn't a competitive differentiator. Standardizing systems early accelerates value capture — running legacy platforms in parallel adds cost without adding value.

Frequently Asked Questions

What is considered "mid-market" for M&A purposes?

The National Center for the Middle Market defines U.S. middle market companies as those with annual revenues between $10 million and $1 billion. The lower middle market — often the focus of business brokers — typically refers to businesses in the $5 million to $100 million revenue range, though definitions vary by advisor and transaction type.

Why do so many mid-market M&A deals fail?

The most common causes are poor strategic alignment, inadequate due diligence, valuation gaps between buyer and seller, cultural misalignment, and weak post-merger integration planning. All are preventable with disciplined preparation before the deal process begins.

How long does a typical mid-market M&A transaction take?

For the $5M–$50M segment, the average time from initial advisor engagement to close is approximately 11 months, with roughly 5 months from LOI to closing. Well-prepared sellers with organized financials and a clean data room consistently compress this timeline.

How is a mid-market business typically valued?

Mid-market valuations typically use a blend of EBITDA multiples benchmarked against precedent transactions, discounted cash flow analysis, and qualitative adjustments for factors like customer concentration, management depth, and growth trajectory. Current lower-middle-market multiples averaged 7.2x EBITDA in H1 2025, though the applicable range varies by sector and deal size.

How do you maintain confidentiality when selling a mid-market business?

The standard approach uses NDAs before sharing any business-specific information, controlled buyer processes managed by an advisor, and a pre-vetted buyer network that filters out unqualified parties. This ensures only serious, qualified buyers gain access, protecting the seller's employees, customers, and competitive position throughout the process.

Do I need a business broker for a mid-market deal?

For most business owners — who have limited prior M&A experience — the answer is yes. An experienced broker manages the process, provides access to qualified buyers, supports valuation, and protects the seller's negotiating position against buyers who have often completed dozens of similar transactions.