Introduction

Most manufacturing business owners spend decades building something genuinely valuable — then undermine it in the final act by mispricing the sale. According to Axial, 70–90% of manufacturing business sale processes fail to deliver the owner's ideal outcome on price, timeline, or stewardship. A significant share of those failures trace back to valuation gaps.

Whether you're planning a sale, seeking acquisition financing, or thinking through succession, an accurate valuation shapes every decision that follows. Overpricing drives buyers away. Underpricing leaves real money behind.

This guide covers:

- The two primary valuation methods used for manufacturing businesses

- How to calculate adjusted earnings correctly

- What industry multiples look like by sub-sector and company size

- The factors that move your multiple up or down

- What to do in the 12–24 months before you go to market

TLDR: Key Takeaways

- Manufacturing businesses are most commonly valued using a Multiple of Earnings — adjusted EBITDA or SDE multiplied by an industry-appropriate multiple

- EBITDA multiples broadly range from 3x to 5x for smaller manufacturers, with middle-market and specialty companies often exceeding that range

- Size matters significantly — a business with $5M in EBITDA commands a meaningfully higher multiple than one with $500K

- Revenue-based "rules of thumb" are unreliable — profitability drives offers far more than top-line revenue

- Manufacturing owners can get a complimentary Assessment of Value from Chelsis Financial — no commitment required

The Two Primary Valuation Methods for Manufacturing Businesses

For an operating manufacturer, the balance sheet tells only part of the story. Intangible assets — customer relationships, assembled workforce, proprietary processes, goodwill — contribute real value that hard assets don't capture. That's why two income- and market-based approaches drive most professional valuations.

The Market Approach

A valuator researches comparable sales of similar manufacturing businesses using transaction databases such as BVR's DealStats or BIZCOMPS, filtering by industry classification code, company size, and geography. They then adjust for differences in financial performance and deal structure — earnouts, seller financing, installment terms — to arrive at a well-supported value estimate.

This approach works best when enough comparable transactions exist. For niche manufacturers with limited comps, the income approach carries more weight.

The Income Approach

The most common income-based method for manufacturing businesses is the Multiple of Earnings method:

Adjusted EBITDA (or SDE) × Industry Multiple = Estimated Enterprise Value

A second method, Discounted Cash Flow (DCF) analysis, projects multiple years of future cash flows and discounts them to present value. DCF is reserved for larger or more complex businesses where near-term growth trajectories diverge from historical results — not the default tool for most Main Street or lower middle market deals.

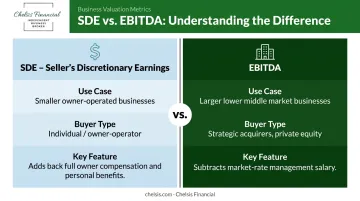

Choosing Between SDE and EBITDA

The right earnings metric depends on company size:

| Metric | When to Use | Who's Buying |

|---|---|---|

| SDE (Seller's Discretionary Earnings) | Smaller owner-operated businesses, typically Main Street deals | Individual buyers, owner-operators |

| EBITDA | Larger businesses, lower middle market | Strategic acquirers, private equity |

Per IBBA/M&A Source Market Pulse data, Main Street transactions (up to approximately $2M in value) most commonly use SDE, while lower middle market deals use EBITDA.

In practice, the distinction is straightforward: SDE adds back the full owner's compensation and personal benefits, normalizing earnings for a single owner-operator. EBITDA subtracts a market-rate management salary — reflecting the cost of replacing the owner — which is appropriate when the buyer won't personally run the business.

Calculating Your Earnings: EBITDA, SDE, and Add-Backs Explained

Getting your adjusted earnings right is the foundation of any credible valuation. Missed add-backs directly reduce your stated value. Poorly supported ones will draw fire during due diligence.

Standard Add-Backs

These apply to most manufacturing businesses:

- Owner's salary — adjust to market-rate replacement cost; add back the above-market portion for EBITDA, or the full amount for SDE

- Owner payroll taxes — the employer-side taxes tied to the owner's compensation

- Owner's health insurance — premiums paid through the business

- Owner's retirement contributions — 401(k) or similar employer contributions

- Depreciation — a non-cash expense; always added back

- Amortization — also a non-cash expense, covering intangible assets such as patents or goodwill; always added back

- Interest expense — removed because the buyer will have a different financing structure

Discretionary and Situational Add-Backs

These are business-specific and require careful judgment:

- Personal vehicle leases run through the business

- Charitable donations not tied to revenue generation

- One-time legal settlements

- Non-recurring equipment purchases or facility repairs

The key test: is the expense truly non-recurring? Buyers and their advisors will challenge any add-back that looks like an ongoing cost dressed up as a one-time event.

One Important Nuance on Owner's Salary

The owner's salary add-back in the Standard list above depends entirely on whether the owner is operationally involved — the treatment differs significantly between the two scenarios.

- If the owner is not active in daily operations: add back the entire officer's salary, no deduction needed

- If the owner is active: add back only the above-market portion, then subtract a market-rate replacement manager's salary

Using a Weighted Average

Standard practice calls for calculating adjusted earnings across the three most recent fiscal years, then applying a weighted average that gives greater weight to the most recent results. This matters most when your latest year ran unusually high or low. If a single peak year stands alone without a broader trend to support it, buyers and their lenders will normalize the number down.

Manufacturing Business Valuation Multiples: Benchmarks by Sector and Company Size

The "3x to 5x EBITDA" figure you'll hear most often is a rough baseline. Actual multiples vary considerably by sub-sector, company size, and buyer type — sometimes by several turns of EBITDA.

Sub-Sector Benchmarks

Recent transaction data shows meaningful variation across manufacturing categories:

| Sub-Sector | EBITDA Multiple | Source/Period |

|---|---|---|

| Overall manufacturing | 6.6x average | GF Data / Taureau Group, Q1 2025 |

| Food products | 7.3x average | Porter White / GF Data, Q1 2025 |

| Fabricated metal products | 6.2x average | Porter White, Q3 2025 |

| Metal fabrication (NAICS 332, $10M–$500M EV) | 6.1x median | Cascade Partners / GF Data, Q3 2024 |

| Specialty chemicals | ~9.0x–10.0x | Capstone Partners, H1 2025 |

| Plastics (PE buyers) | 9.9x median | R.L. Hulett, Q4 2025 |

| Plastics (strategic buyers) | 5.1x median | R.L. Hulett, Q4 2025 |

Note that these figures reflect middle-market and larger transactions. Smaller businesses — particularly those under $2M in enterprise value — trade at lower multiples.

How Size Affects Your Multiple

GF Data's H1 2025 analysis of transactions under $25M shows a clear size effect:

- $1M–$5M TEV tier: ~5.5x EBITDA average

- $10M–$25M TEV tier: 6.2x–6.7x EBITDA average

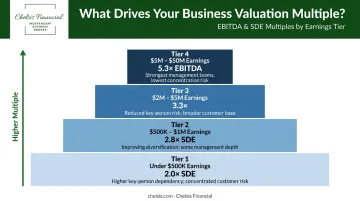

For smaller owner-operated manufacturers, Market Pulse Q2 2024 reported SDE multiples of:

- Under $500K earnings: 2.0x SDE

- $500K–$1M earnings: 2.8x SDE

- $2M–$5M earnings: 3.3x

- $5M–$50M earnings: 5.3x EBITDA

Larger businesses command higher multiples because they're less exposed to single-customer concentration, key-person dependency, and operational fragility. A manufacturer generating $5M in EBITDA simply carries fewer of these risks than one generating $500K.

How Buyer Type Influences Price

Strategic buyers — those who can capture synergies through added capacity or customer base overlap — often pay more than purely financial buyers. Pepperdine's 2023 Private Capital Markets Report found that 58% of respondents observed strategic buyer premiums between 1% and 20% over financial buyer offers.

Private equity buyers apply more conservative multiples based on target return thresholds and financing limits. For the same business, the spread between the lowest and highest offers can be 2x–3x — making buyer selection a significant lever in the final outcome.

What's Included in the Purchase Price

- Included: Inventory, furniture, fixtures, and equipment necessary to generate the earnings

- Excluded (retained by seller): Cash and accounts receivable

- Paid off at closing: Outstanding loans on equipment or machinery, typically from proceeds

Key Factors That Influence Your Valuation Multiple

Two factors suppress manufacturing valuations more than any others — owner dependence and customer concentration. Both are within a seller's control to address before going to market.

Customer Concentration

Chelsis Financial applies a straightforward benchmark: no single customer should represent more than 10–15% of revenue. Beyond that threshold, buyers start discounting.

When concentration is high, deals get restructured. Chelsis Financial has documented cases where high customer concentration resulted in a 30% reduction in offer price, along with earnout provisions and seller financing requirements designed to protect the buyer if key accounts don't transfer. Lenders take the same view — high concentration can affect financing availability, not just price.

Owner Dependence

When a business can't operate without its founder, buyers price that dependency directly into their offer. The indicators they examine:

- Does a management team exist that can operate independently?

- Are key processes documented, or do they live in the owner's head?

- Do customer relationships belong to the company or to the owner personally?

Addressing these gaps before listing — even 12 to 18 months out — directly expands the buyer pool and protects the multiple.

Additional Value Drivers

These factors push a manufacturing business toward the higher end of its multiple range:

- Clean, auditable financials — accrual-based accounting rather than simple cash-basis records

- Low upcoming capex requirements — aging equipment that needs replacement suppresses value

- Proprietary technology or patents — differentiation that competitors can't easily replicate

- Lean working capital management — disciplined inventory and strong receivables collections

- Recurring customer relationships — multi-year contracts or repeat purchase patterns

Valuation Mistakes Manufacturing Business Owners Must Avoid

Relying on Revenue Multiples

"Manufacturing businesses are worth 1x revenue plus inventory" is a rule of thumb, not a valuation. Two companies with $5M in revenue but different margins produce completely different values:

- Company A: $5M revenue × 10% EBITDA margin = $500K EBITDA × 4x = $2M value

- Company B: $5M revenue × 25% EBITDA margin = $1.25M EBITDA × 4x = $5M value

Same revenue. $3M difference in value. Buyers aren't paying for your top line — they're paying for what the business earns.

Using a Single Peak Year Without Context

Buyers normalize earnings. If your most recent year was inflated by a one-time contract, unusual market conditions, or a post-pandemic spike, buyers and their advisors will apply a conservative weighted trailing average. Going to market when you can't explain the sustainability of your results puts you at a negotiating disadvantage.

Failing the Buyer's Cash Flow Test

Serious buyers run a basic stress test on any acquisition: can this business simultaneously (1) service the acquisition debt, (2) pay the new owner a reasonable salary, and (3) generate an acceptable return on invested capital? For SBA-financed deals, lenders require a debt service coverage ratio of at least 1.25x. If your valuation implies the business can't clear that bar, the asking price will be challenged — regardless of which multiple you used.

Understanding these mistakes is the first step. Getting a professionally prepared valuation is what turns that awareness into leverage at the negotiating table.

How to Maximize Your Manufacturing Business Value Before Selling

Benchmark Your Financial Performance

Compare your gross margin, EBITDA margin, inventory turnover, and asset turnover against industry peers. Buyers and their advisors will run the same comparison. If you're lagging, address it at least 12–24 months before going to market — not after.

Time Your Exit Strategically

Go to market when your most recent year shows healthy growth or stable profitability. Selling after a down year significantly weakens your negotiating position. Market Pulse Q2 2024 data shows that a meaningful share of sellers delay transactions specifically to strengthen their financial story — that discipline pays off.

Reduce Owner Dependence Proactively

- Build out management with key roles — at minimum someone handling customer relationships and someone overseeing operations

- Document processes, key accounts, and institutional knowledge

- Migrate to cloud-based accounting (QuickBooks Online) before going to market — it improves buyer confidence during diligence

Work With the Right Buyer Network

Identifying synergistic buyers — those who would genuinely benefit from adding your capacity, customer base, or supplier relationships — can command a higher multiple than marketing to purely financial buyers. That gap can represent 20–50% or more in final sale price — a difference worth pursuing deliberately.

Chelsis Financial maintains a buyer registry and networks with over 2,000 businesses across the Midwest to surface exactly these strategic matches, keeping the seller's identity confidential throughout. Their complimentary Assessment of Value gives owners a clear picture of where they stand — current valuation range, key value drivers, and what's worth addressing before going to market.

Frequently Asked Questions

How would you value a manufacturing company?

Manufacturing companies are most commonly valued using a Multiple of Earnings method — multiplying adjusted EBITDA or SDE by an industry-appropriate multiple. Most manufacturing sub-sectors produce a valuation range of 3x to 5x EBITDA, though specialty manufacturers and larger businesses frequently exceed that range.

What is a good EBITDA multiple for a manufacturing business?

Most manufacturing businesses sell in the 3x–5x EBITDA range at the smaller end of the market, with middle-market transactions in specialty chemicals, food products, and fabricated metals regularly exceeding 6x. Sub-sector, company size, and the quality of the buyer pool are the primary variables.

Should I use SDE or EBITDA to value my manufacturing business?

Use SDE for smaller, owner-operated manufacturers where Main Street buyers are the likely acquirers. Use EBITDA when the business is larger and the likely buyer is a strategic acquirer or private equity group that will install professional management.

Does the value of my equipment get added to the sale price?

No — equipment necessary to generate the business's earnings is already embedded in the earnings-based valuation and should not be double-counted. However, any outstanding loans on equipment are typically paid off at closing from the seller's proceeds.

What factors most commonly hurt a manufacturing business valuation?

The most common value-reducing factors are:

- High customer concentration or reliance on a single account

- Heavy owner dependence with no management depth

- Aging equipment requiring significant near-term capital expenditure

- Inconsistent or declining revenue over the prior 2–3 years

- Poor documentation of processes, contracts, and key relationships

How do I know when my manufacturing business is ready to sell?

A business is best positioned when it has 2–3 years of consistent or growing earnings, a management team capable of operating without the owner, and clean financial records. Chelsis Financial offers a complimentary Assessment of Value to help owners understand where they stand before going to market.