Introduction

Every year, thousands of privately held businesses change hands in the lower-middle market. Most owners get one shot at it. Without in-house deal teams, smaller business owners often lack the negotiation experience, buyer networks, and valuation expertise needed to navigate a sale confidently — and the wrong advisor can cost them years of built-up value.

This guide presents a curated list of top M&A advisory firms for lower-middle-market businesses, the criteria used to evaluate them, and what to look for when choosing the right partner.

Key Takeaways

- Lower-middle-market businesses ($1M–$50M enterprise value) need specialized M&A advisors, not generalist banks

- The best firms keep your sale confidential throughout — protecting your identity during buyer outreach until letters of intent are signed

- Key criteria: deal size fit, buyer network depth, industry experience, fee transparency

- Standout firms include Chelsis Financial, Calder Capital, Sica|Fletcher, Sun Mergers & Acquisitions, and Woodbridge International

- Most lower-middle-market advisors work on a success-fee model — meaning they only get paid when your deal closes

What Is the Lower-Middle Market in M&A?

The lower-middle market generally refers to privately held businesses with revenues between $5M and $100M, or EBITDA between $1M and $10M. This segment is often underserved by large investment banks focused on bigger deals. Yet deal volume tells a different story: according to PitchBook's 2025 Annual US PE Middle Market Report, US private equity middle-market deal value climbed 8.5% year-over-year to $410.7 billion across approximately 4,018 transactions.

Lower-middle-market deals have distinct characteristics:

- Owner-operated businesses with founders deeply involved in daily operations

- Fewer institutional buyers compared to larger transactions

- Emotional complexity as founders transition businesses they've built over decades

- Critical confidentiality requirements to protect relationships with employees, suppliers, and customers

These same characteristics make the segment attractive to private equity buyers hunting for add-on acquisitions. GF Data reports that in the sub-$25M tier, add-on deals command total debt coverage of 5.7x EBITDA, compared to just 2.3x for standalone platforms. That leverage gap means buyers are willing to pay more — and owners who work with advisors who understand this dynamic negotiate from a much stronger position.

Best M&A Advisory Firms for Lower-Middle-Market Businesses

These firms were selected based on their demonstrated focus on lower-middle-market deal sizes, buyer network quality, track record of closed transactions, and reputation for client-centered service.

Chelsis Financial

Chelsis Financial is a business broker and M&A advisory firm focused on helping business owners sell with confidence and discretion. The firm prioritizes maximizing value for owners approaching retirement or ownership transitions, while protecting seller relationships, employees, and competitive standing throughout the process.

Key differentiators include:

- Complimentary Assessment of Value — defensible valuation guidance with no upfront cost

- Qualified buyer registry spanning multiple industries

- End-to-end support from initial valuation through closing

Chelsis has advised on transactions across fuel distribution, water purification manufacturing, healthcare equipment, aerospace manufacturing, and dental practices — bringing genuine cross-industry depth to each engagement.

| Focus Area | Business sales and ownership transitions for privately held companies |

|---|---|

| Deal Size Range | Lower-middle market; tailored for owner-operated businesses |

| Key Differentiator | Complimentary Assessment of Value + confidential, discreet process |

Calder Capital

Calder Capital is a nationally recognized lower-middle-market M&A advisory firm specializing in businesses valued between $1M and $100M across manufacturing, construction, distribution, and business services. The firm earned recognition as an Axial Top 10 Lower Middle Market M&A Advisor from 2020–2024 and advanced to the #4 ranking nationally for 2025.

Supported by a team of 50+ professionals, Calder maintains a proprietary buyer database and aggressive deal sourcing approach. The firm closed 58 transactions in 2025 alone, demonstrating consistent high-velocity execution. Calder is the only Michigan-based firm on Axial's Top 10 list and one of just two Midwest firms recognized.

| Focus Area | Manufacturing, construction, distribution, business services |

|---|---|

| Deal Size Range | $1M–$100M enterprise value |

| Key Differentiator | Axial Top 10 recognition, 58 annual closed deals, proprietary buyer database |

Sica|Fletcher

Sica|Fletcher is a boutique M&A advisory firm founded in 2014 with top-ranked lower-middle-market standing, specializing in financial services and insurance sectors alongside broader sell-side and buy-side advisory. The firm closes more deals than firms twice its size, earning top positions in lower-middle-market league tables.

A defining characteristic is that senior principals Mike Fletcher and Al Sica remain personally involved in every deal, ensuring clients receive experienced guidance throughout the transaction. This principal-led approach combined with small-team agility allows Sica|Fletcher to deliver responsive service — direct access to decision-makers that large-firm deal teams rarely provide.

| Focus Area | Financial services, insurance, sell-side and buy-side advisory |

|---|---|

| Deal Size Range | $1M–$30M |

| Key Differentiator | Principal-led deal execution, top league table rankings, small-team agility |

Sun Mergers & Acquisitions

Sun Mergers & Acquisitions is a full-service M&A advisory firm specializing in the confidential sale, merger, acquisition, and valuation of privately held mid-market companies—particularly entrepreneur-owned businesses. The firm maintains a strong network of strategic acquirers, financial buyers, and private equity firms across multiple industries.

Sun's strategy centers on generating multiple competing offers to avoid dependency on a single buyer, increasing negotiating leverage and driving higher valuations. The firm has earned Axial Top 20 Investment Bank recognition and brings broad cross-industry experience spanning manufacturing, services, and technology.

| Focus Area | Privately held, entrepreneur-owned companies across industries |

|---|---|

| Deal Size Range | $3M–$75M revenue businesses |

| Key Differentiator | Multi-buyer competitive process, Axial Top 20 recognition, confidential sale expertise |

Woodbridge International

Woodbridge International brings three decades of sell-side M&A experience, serving lower-middle-market clients across diverse industries including manufacturing, distribution, and service-based businesses. The firm operates with global reach across the US, Canada, and international markets.

Woodbridge differentiates through its collaborative culture and proprietary 150-day controlled auction process that establishes a closing date upfront to prevent deal drag. The firm leverages a global database of 8,400 private equity groups and 410,000 strategic companies to maximize buyer competition. Uniquely, Woodbridge offers management training and seller workshops, giving business owners practical preparation for the sale process before engaging.

| Focus Area | Sell-side advisory across manufacturing, distribution, and services |

|---|---|

| Deal Size Range | $5M–$150M |

| Key Differentiator | 30+ years of experience, global buyer outreach, seller workshop training |

How We Selected These Firms

These firms were assessed based on demonstrated specialization in the lower-middle-market segment, depth and quality of buyer networks, publicly available deal volume and transaction history, and client-focused service models—not simply brand recognition or firm size.

Many business owners choose advisors based on name prestige rather than deal size fit. A bulge-bracket bank focused on $500M+ transactions will rarely give a $10M business the attention or buyer-pool access it deserves. Elite boutiques like Perella Weinberg Partners handle $600M to $40B megadeals and lack the specialized processes required for $1M–$10M EBITDA companies.

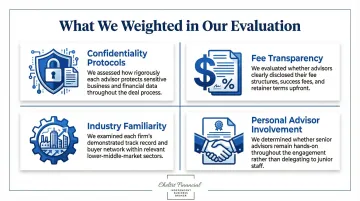

Beyond deal size fit, we weighted these factors heavily in our evaluation:

- Confidentiality protocols — how firms protect sensitive business information throughout the process

- Fee transparency — clear retainer vs. success-based structures with no hidden costs

- Industry familiarity — relevant sector experience, not generalist coverage

- Personal advisor involvement — senior-level engagement on deals, not hand-offs to junior staff

The stakes are real. The Firmex M&A Fee Guide (citing Fairfield University and Divestopedia) found that private sellers receive 6% to 25% higher acquisition premiums when they retain full-service advisors compared to unrepresented sellers—far exceeding the cost of advisory fees.

What to Look for in a Lower-Middle-Market M&A Advisor

Deal Size Specialization

Working with an advisor whose "sweet spot" aligns with your business's value range is critical. Advisors focused on your size bracket will have the right buyer relationships, realistic valuation benchmarks, and deal structures suited to your transaction. Mismatched advisory fit directly impacts deal outcomes—a firm accustomed to $100M deals will lack the specialized buyer network and process rigor needed for a $5M business.

Buyer Network Quality and Reach

The advisor's existing network of qualified buyers—strategic acquirers, private equity, independent sponsors, family offices—directly determines how competitive your sale process will be. Ask prospective advisors how many active buyers they maintain relationships with and how they source new ones. Firms using timeline-driven controlled auctions or tech-enabled buyer outreach create competitive tension that forces higher bids and faster closes.

Confidentiality and Discretion Protocols

For lower-middle-market sellers, a premature leak about a potential sale can damage relationships with employees, suppliers, and customers. Robust confidentiality practices include NDAs signed before any information release, blind teasers that reveal industry and financials without identifying the company, and controlled information release that stages data disclosure based on buyer qualification.

Fee Structure Transparency

The two primary fee models are retainer plus success fee versus success fee only. According to the Divestopedia/Axial M&A Fee Guide for 2024-2025, the Double-Lehman scale has become the dominant success fee structure:

- 10% on the first $1M, 8% on the second, 6% on the third

- 4% on the fourth, and 2% on everything thereafter

- Average total fees: 4.8% on a $5M deal, 3.4% on a $20M deal

Beyond the success fee, 81% of North American middle-market advisors charge an engagement or work fee, most commonly a monthly retainer between $5,000 and $10,000. Advisors should be upfront about all costs before engagement.

Senior-Level Involvement

One of the most common complaints in M&A advisory is that the senior partner wins the business and then disappears. For lower-middle-market deals, insist on an advisor where experienced professionals remain hands-on through valuation, buyer outreach, negotiation, and closing. Principal-led boutique firms that keep senior advisors personally involved from start to close exemplify this standard.

Conclusion

For lower-middle-market sellers, fit matters more than firm size. The advisor who closes deals in your revenue range, protects confidentiality from day one, and keeps your timeline and exit goals at the center of the process is worth far more than a recognizable name.

Evaluate any prospective advisor by asking direct questions:

- How many deals in my size range have you closed in the past 12 months?

- Who specifically will manage my transaction?

- What does your confidentiality process look like from day one?

If you're considering a sale, Chelsis Financial's Complimentary Assessment of Value gives you a clear picture of what your business is worth before you commit to anything. Schedule a confidential consultation at calendly.com/chelsis/getanswers or call 866-842-5151.

Frequently Asked Questions

What does "lower mid market" mean?

The lower-middle market typically refers to privately held businesses with revenues between roughly $5M and $50M or enterprise values in the $1M–$50M range. This segment sits between small "Main Street" businesses handled by traditional business brokers and the larger middle market served by institutional investment banks.

Who are the Big 4 in M&A?

The "Big 4" in M&A advisory context typically refers to the four major accounting and consulting firms—Deloitte, PwC, KPMG, and EY—that offer M&A transaction advisory services. For lower-middle-market deals, boutique M&A advisory firms are generally a better fit than these large institutional players.

What is the difference between a business broker and an M&A advisor for lower-middle-market deals?

Business brokers typically handle smaller Main Street transactions (under $1M–$2M) with less complex processes, while lower-middle-market M&A advisors manage larger, more structured deals. Advisors conduct detailed valuations, confidential buyer outreach, competitive bid processes, and post-closing structuring considerations that brokers typically don't handle.

How much does it cost to hire a lower-middle-market M&A advisor?

Most lower-middle-market M&A advisors use a combination of a modest monthly retainer ($5,000–$10,000) and a success fee (typically 5–10% for deals under $10M, decreasing for larger transactions). Clarify the full fee structure—including any upfront costs—before signing an engagement letter.

How long does it typically take to sell a lower-middle-market business?

Most lower-middle-market sales take 6–12 months from engagement to closing, depending on business complexity, market conditions, and documentation readiness. Industry sources recommend engaging an advisor 12–24 months before a planned exit to complete sell-side Quality of Earnings, optimize tax structures, and address operational gaps.

How do I know if my business is ready to go to market?

Key indicators include clean financials for 3+ years, stable or growing revenue, and documented processes that don't depend entirely on the owner. GF Data reports that businesses completing a sell-side Quality of Earnings before going to market achieve average TEV/EBITDA multiples of 7.4x vs. 7.0x for those that don't—a meaningful difference at scale. A reputable advisor can help assess your readiness through an initial valuation consultation.