Introduction

You've spent years building your business—grinding through slow seasons, holding payroll through downturns, and making calls no one else would make. When it's time to sell, most owners hit the same wall: no reliable way to know what the business is actually worth. Price too high and qualified buyers disappear. Underprice it and you could leave six figures on the table.

Pricing a business for sale isn't guesswork. It's a formal valuation process that requires financial analysis, market context, and the right methodology.

Unlike residential real estate, where comparable sales are public record, private business transactions demand a structured approach that accounts for earnings, risk, and transferability.

This guide explains what business pricing involves, the three core valuation methods professionals use, the factors that move your number up or down, and the mistakes that kill deals before they start.

Key Takeaways

- Three valuation methods apply to most sales: income-based, asset-based, and market-based (comparable sales)

- Most small businesses sell for a multiple of SDE or EBITDA—typically 2x to 6x depending on industry and size

- A realistic price reflects risk, growth potential, market conditions, and the quality of your financial records

- Overpricing is the #1 reason businesses fail to sell; an independent valuation anchors negotiations and attracts serious buyers

- Clean financials and strategic operational improvements before listing can increase your final sale price by 20% or more

What Does It Mean to Price a Business for Sale?

Business pricing is the process of determining a defensible asking price that reflects fair market value: what a willing buyer and seller would agree to under normal conditions, with neither party under duress.

Two paths exist:

Formal business valuation: Conducted by accredited appraisers (ABV, ASA, CVA) using standardized income, market, and asset approaches. Required for IRS filings, litigation, ESOP transactions, and financial reporting. Cost: $7,000 to $25,000.

Broker Opinion of Value (BOV): An informal, market-based estimate used for listing purposes. Relies primarily on comparable sales and industry data. Cost: $500 to $5,000.

Why pricing matters for sellers:

Knowing which approach fits your situation is only half the equation. Getting the number wrong carries real consequences.

An unsupported asking price prolongs the sale, invites lowball offers, and signals to buyers that the seller hasn't done their homework. The Pepperdine Private Capital Markets Report identifies pricing mismatches as the #1 reason deals fail, accounting for 26% of terminated engagements. Of those failures, 84% involved valuation gaps of 11% to 30%.

The Three Core Valuation Methods

Professional valuators and business brokers rely on three approaches—income-based, asset-based, and market-based—and typically blend all three to reach a defensible final number.

Income-Based Approach (Earnings Multiples)

This is the most common method for operating businesses. A normalized earnings figure is multiplied by an industry-appropriate multiple to estimate value.

SDE vs. EBITDA:

SDE (Seller's Discretionary Earnings) applies to smaller businesses (typically under $5M revenue). It adds back the owner's salary, benefits, and personal expenses to net profit, capturing the total financial benefit to one full-time owner-operator.

EBITDA (Earnings Before Interest, Taxes, Depreciation, Amortization) applies to larger businesses ($5M+ revenue) with professional management in place. It adds back only the portion of owner salary that exceeds market replacement cost.

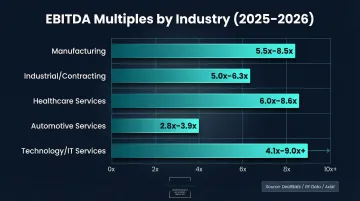

Typical multiples by industry:

| Industry | EBITDA Multiple Range |

|---|---|

| Manufacturing | 5.5x – 8.5x |

| Industrial / Contracting | 5.0x – 6.3x |

| Healthcare Services | 6.0x – 8.6x |

| Automotive Services | 2.8x – 3.9x |

| Technology / IT Services | 4.1x – 9.0x+ |

Source: DealStats / GF Data / Axial, 2025-2026

Size matters: GF Data reports that businesses under $10M enterprise value average 5.5x–5.6x EBITDA, while $10M–$25M deals average 6.2x–6.7x EBITDA.

Discounted Cash Flow (DCF) variant: Used when earnings show strong growth or decline trends. Projects future cash flows and discounts them to present value—more complex but appropriate for high-growth companies.

When earnings alone don't tell the full story, a second method shifts focus entirely to what the business owns.

Asset-Based Approach

This method calculates value based on net worth: total assets (equipment, inventory, IP, real estate) minus total liabilities.

When to use it:

- Asset value exceeds earning power

- Capital-heavy businesses (manufacturing, distribution)

- Companies being wound down

- Businesses with minimal ongoing cash flow

Practical limitations make this method harder to apply than it sounds:

- Private company transactions aren't publicly disclosed — proprietary database access is essential

- Data ages quickly, so recent comparables carry more weight than older ones

- Each comparable needs adjustment for working capital, deal structure (asset vs. stock), and how discretionary earnings were defined

Step-by-Step: How to Calculate Your Business's Asking Price

Step 1: Gather and Organize Financial Records

Start with three years of tax returns or CPA-reviewed financial statements, plus year-to-date P&L and balance sheet. Clean, consistent records reduce buyer skepticism and perceived risk.

Step 2: Calculate Normalized Earnings (SDE or EBITDA)

Identify and remove:

- Non-recurring expenses (one-time legal settlements, website redesigns)

- Personal expenses run through the business (family cell phones, personal vehicle leases)

- Owner's compensation (full salary for SDE; excess above market rate for EBITDA)

- Owner perks (health insurance, retirement contributions, client entertainment)

These add-backs show a buyer exactly what the business earns when stripped of owner-specific costs — the number they'll actually use to evaluate the deal.

Step 3: Select and Apply the Right Valuation Method(s)

Choose based on your business profile:

- Income approach (earnings multiple) — best for stable, profitable operations

- Asset approach — best when tangible assets outweigh cash flow

- Market approach — most useful when strong comparable sales data exists

For most small to mid-market businesses, the income approach is the primary method, with market comps used to validate the multiple.

Step 4: Set the Asking Price (Not Just the Valuation Number)

The asking price may be 5%–10% above the valuation conclusion to allow negotiating room—but stay within a credible range. Price too far above market and you'll lose qualified buyers before the first conversation — SBA lenders also cap financing based on appraised value, so an inflated ask can kill a deal at the finish line.

Once you have a defensible number, the next step is preparing the materials that get buyers to the table.

Key Factors That Affect Your Business's Price

The earnings multiple isn't fixed. It moves based on business-specific and market-level factors.

Financial factors:

- Revenue size and growth rate both matter — larger, faster-growing businesses command higher multiples

- Strong profit margins signal operational efficiency and reduce buyer risk

- Stable, consistent earnings lower perceived risk; volatile earnings compress multiples

- Audited financials command higher multiples than disorganized or incomplete books

These financial signals set the floor for your valuation. Operational factors then move the number up or down from there.

Operational and structural factors:

- Owner dependence carries a steep cost: manufacturing firms heavily reliant on the owner trade at 4.0x EBITDA vs. 7.5x for professionally managed firms, representing a 47% discount

- A single customer exceeding 20% of revenue triggers 10%–30% valuation discounts — concentration risk makes buyers nervous

- Subscription or contract revenue increases predictability and commands a premium over one-time sales

- Businesses that run without the owner are worth significantly more than those that can't function without them

Market and industry factors:

- M&A activity in the sector: Active acquisition sectors attract more buyers and higher multiples

- Macroeconomic conditions: Interest rates, lending availability, and economic outlook

- Industry growth trajectory: Buyers pay more for businesses in expanding sectors

Intangible value drivers:

- Brand reputation

- Proprietary systems or intellectual property

- Established supplier relationships

- Geographic advantages

These intangibles are real but harder to quantify — they typically surface within the goodwill component of your valuation. Taken together, all four categories explain why two businesses with identical revenue can sell at very different multiples. Understanding where you stand on each one is the first step toward closing that gap before you go to market.

Common Pricing Mistakes Business Owners Make

Even well-run businesses get stuck on the market because the asking price doesn't hold up to scrutiny. These three mistakes account for the majority of failed or delayed deals:

- Letting effort drive the number. Years of hard work don't translate to market value. Buyers assess financials, not personal investment — and an inflated ask based on sweat equity simply deters qualified offers.

- Treating goodwill as a separate add-on. Goodwill isn't a bonus tacked onto the valuation; it's already built into the earnings multiple. Sellers who try to charge for it twice consistently lose deals to buyers who know better.

- Pricing off revenue instead of earnings. A $5M-revenue business with thin margins can be worth less than a $2M-revenue business with stable, recurring profits. Buyers pay for what the business earns — not what it sells.

How to Prepare Your Business to Maximize Sale Price

Unlike real estate, business sellers often have 12–24 months to take steps that materially increase valuation. The earlier you start, the greater the impact.

Financial cleanup:

- Separate personal expenses from business expenses

- Pay applicable taxes and resolve outstanding liabilities

- Present financials in a format that reduces buyer risk

A complimentary Assessment of Value from Chelsis Financial can pinpoint which of these adjustments will move your number the most before you go to market.

Operational improvements that move the multiple:

- Build a management layer (CFO, COO, or operations manager) so the business doesn't depend on you

- Reduce any single customer to below 20% of revenue to eliminate concentration risk

- Lock in multi-year contracts that convert one-time sales into recurring revenue

- Create documented SOPs showing the business runs on systems, not on the owner

Buyers pay higher multiples for businesses that can grow after the owner leaves. Each of these steps directly addresses that concern.

Conclusion

Pricing a business for sale isn't guesswork. It requires a structured valuation using the right method for your business type, supported by clean financials and a clear understanding of what buyers actually pay for.

The gap between what an owner thinks their business is worth and what the market will pay is one of the biggest obstacles to a successful sale. An independent valuation — grounded in real transaction data and your specific financials — is what closes that gap.

If you're ready to understand what your business is actually worth, Chelsis Financial offers a no-cost, confidential business assessment — covering valuation methodology, your financial positioning, and what buyers in your sector are paying right now.

Frequently Asked Questions

What multiple of earnings is a business typically worth?

Most small to mid-size businesses sell for a multiple of SDE or EBITDA, typically 2x–6x. The specific multiple depends on industry, business size, earnings stability, and market conditions. Manufacturing firms average 5.5x–8.5x EBITDA, while automotive services average 2.8x–3.9x.

How do you determine if a business is worth buying?

Buyers review normalized earnings and compare the asking price to similar transactions. They also assess operational risks—owner dependence, customer concentration—and project whether the business can service acquisition debt and deliver acceptable returns after closing.

What is the difference between SDE and EBITDA in business valuation?

SDE applies to smaller businesses (under $5M revenue) where the owner works in the business—it adds back their full compensation. EBITDA suits larger companies with professional management and adds back only the portion of owner pay above a market-rate replacement salary. Applying the wrong metric can meaningfully skew your valuation in either direction.

Should I get a professional valuation before listing my business for sale?

Yes. An independent valuation establishes a credible asking price, speeds up buyer negotiations, supports SBA lending, and reduces the risk of leaving money on the table or wasting time on unqualified offers.

What factors most impact the asking price of a small business?

The biggest drivers are earnings size and consistency, owner dependence, customer concentration, industry growth trends, and financial documentation quality. Addressing even two or three of these before listing can add 20% or more to your final price.

How long does it typically take to sell a business after pricing it?

The timeline varies widely—often 6 months to over a year. An accurately priced business with clean financials and a targeted buyer pool closes significantly faster than one that is overpriced or poorly documented. Pricing mismatches account for 26% of failed deals.