Introduction

Nearly 2.9 million U.S. business owners — half of all privately-held companies — are at or near retirement age. Most will sell through the middle market, where the rules, participants, and pressures look nothing like the megadeals that dominate financial headlines. Understanding those differences is the starting point for any smart exit.

If you're a business owner weighing a sale or a buyer exploring middle market opportunities, this article offers a practical breakdown of how these deals differ — and what that means for your decisions.

TLDR

- Middle market M&A involves privately held, owner-operated companies and is far more personal and relationship-driven than large-cap deals

- Valuation is less transparent, with wider price ranges tied to owner dependency and private financials

- Financing leans on private equity, mezzanine debt, and seller financing — not public capital markets

- The deal process is leaner but often emotionally complex, with sellers who have spent decades building their businesses

- Post-close integration demands close attention to culture, key relationships, and operational continuity

Defining the Middle Market in M&A

The middle market encompasses companies with annual revenues between $10 million and $1 billion — though some definitions use enterprise value thresholds of $100 million to $1 billion. Nearly 200,000 U.S. middle market businesses represent one-third of private sector GDP and employ approximately 48 million people.

This segment typically includes:

- Family-owned and owner-operated businesses

- Private equity-backed portfolio companies

- Closely held firms not listed on public exchanges

Large-cap M&A, by contrast, typically involves publicly traded companies with market capitalizations in the billions, institutional shareholders, and deals scrutinized by regulators and the financial press. In 2025, 111 transactions valued above $5 billion were announced globally, up 76% from the prior year. These megadeals represented more than 73% of the increase in total deal value.

That concentration of deal value at the top obscures a different reality underneath. Middle market M&A operates as a distinct ecosystem — with its own participants, deal structures, and priorities. These transactions preserve jobs, fuel regional economies, and enable the generational wealth transfers that matter most to business owners who have spent decades building something worth selling.

Market Participants and Deal Dynamics

Large-Cap Deal Drivers

Large-cap deals are driven by institutional investors, corporate boards, activist shareholders, and Wall Street investment banks. Every decision answers to shareholder value and plays out in real time through public filings and stock price movements. The process is impersonal and data-driven, with deals evaluated on:

- Financial metrics and projected synergies

- Regulatory and antitrust considerations

- Market timing and public market conditions

Middle Market Deal Drivers

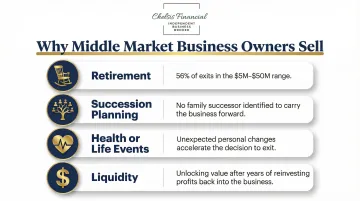

Middle market transactions are predominantly driven by business owners themselves — founders, families, and operators who built their companies over years or decades. Because ownership and management are often the same person, the decision to sell is deeply personal and is frequently triggered by:

- Retirement (the number one reason, accounting for 56% of exits in the $5M-$50M range in Q4 2024)

- Succession planning when no family member wants to take over

- Health events or unexpected life changes

- A desire for liquidity after years of reinvesting profits

Baby Boomers make up nearly 60% of current business owners bringing companies to market, driving the "Silver Tsunami" — an unprecedented wave of business ownership transitions playing out over the next decade.

The Buyer Landscape

That seller wave has attracted serious capital. Private equity firms, holding companies, and strategic acquirers make up the primary buyer pool in the middle market. Over the last eight quarters through Q1 2025, private equity captured 42% of deals in the $5M-$50M sector, while strategics accounted for 37%. With U.S. PE dry powder reaching a record $1.1 trillion, buyer demand remains robust.

Middle market deals are harder to find and far less visible than public company transactions. Most buyers and sellers rely on personal networks, industry relationships, and intermediaries like business brokers and investment bankers to discover opportunities. Open auction processes are the exception, not the rule. That means sellers with experienced advisors and strong market exposure consistently attract more qualified buyers and better terms than those who go it alone.

Valuation and Pricing Differences

Large-Cap Transparency

Large-cap companies are valued using publicly available data: stock prices, public comparables, audited financials, and real-time market multiples. Well-established EBITDA multiples by industry are readily benchmarked, making the process highly transparent. Global median M&A EV/EBITDA multiples stood at approximately 9.3x in 2025.

Middle Market Complexity

Middle market valuations work differently. Financials are private, often not audited to institutional standards, and buyers must dig deeper to normalize:

- Owner compensation (separating reasonable salary from excess distributions)

- Discretionary expenses (personal vehicles, travel, family members on payroll)

- One-time items (legal settlements, equipment purchases, COVID-related costs)

The average TEV/EBITDA multiple for middle market deals in 2024 was 7.2x, but that figure masks significant variation by size:

| Enterprise Value Range | Average EBITDA Multiple (2024) |

|---|---|

| $10M – $25M | 5.9x |

| $25M – $50M | 6.7x |

| $50M – $100M | 7.7x |

| $100M – $250M | 8.5x |

| $250M – $500M | 9.9x |

A distinct size premium exists, with multiples expanding by a full 4.0x from the lowest to highest cohorts.

The Owner Dependency Discount

When a business's revenue, relationships, or operations are heavily tied to a single founder or operator, buyers apply a risk discount. This challenge doesn't exist in large-cap deals with professional management teams. Buyers want answers to questions like:

- What happens to customer relationships when the founder leaves?

- Can the operations team run the business independently?

- Are key processes documented, or locked in the owner's head?

Because of these unknowns, middle market businesses often receive dramatically different bids depending on strategic fit, synergies, and risk tolerance. Large-cap deals, by contrast, cluster more tightly around public market data.

The Opportunity for Sellers

Working with a qualified advisor to prepare clean financials, reduce owner dependency, and document operations can meaningfully improve the final valuation. Companies that performed a sell-side Quality of Earnings report achieved an average multiple of 7.4x versus 7.0x for those without one — a benefit most notable for deals with enterprise values above $50 million.

Chelsis Financial offers a Complimentary Assessment of Value, giving business owners a clear, professional starting point for understanding what their company is worth before entering the market. It reviews four years of financial statements and key business factors, so sellers enter negotiations with a well-supported number — not a guess.

Capital Structure and Deal Financing

Large-Cap Financing Advantages

Large-cap deals have access to the full range of public capital markets: stock issuances, high-grade and high-yield bond markets, syndicated loans, and institutional financing at competitive rates. Large acquirers use their credit ratings and institutional relationships to secure favorable terms—often at significantly lower borrowing costs than middle market peers.

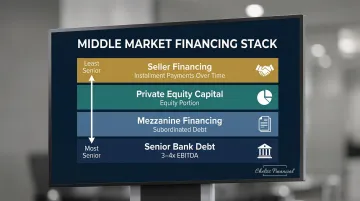

Middle Market Financing Stack

Middle market deals rely on a layered financing structure:

- Senior bank debt — typically covering 3-4x EBITDA

- Private equity capital — providing the equity portion

- Mezzanine financing — subordinated debt filling the gap between senior debt and equity

- Seller financing — where the seller accepts a portion of the purchase price in installments over time

Seller financing appears in over 75% of lower-middle-market transactions, and listings that promote seller financing command an average 15% valuation premium over all-cash consideration. For sellers, this creates interest income and tax advantages while signaling confidence in the business's future performance.

Earnout provisions — where a portion of the deal value depends on post-close performance — are common in middle market transactions and rarely appear in large-cap deals. Though earnouts dropped to an average of 2% of deal financing in Q4 2024 (down from a peak of 10% in 2023), they remain a useful tool for closing valuation gaps between buyers and sellers.

Rollover Equity's Rising Role

Rollover equity has climbed steadily, rising from 14.0% of total enterprise value in 2021 to 16.9% through Q3 2025. This structure keeps sellers invested in the business post-close, aligning interests and reducing buyer risk.

These financing dynamics reflect a broader reality: middle market borrowers face higher borrowing costs and fewer lender options than large corporations, with debt availability shifting alongside economic conditions. The current environment in 2026 features improved debt capital availability—a favorable window for business owners considering a sale.

Deal Process, Timeline, and Post-Close Integration

Process Comparison

Large-cap deals involve armies of investment bankers, lawyers, accountants, and consultants working through formal multi-round auction processes that can take 12–24+ months. The average closing duration for public company acquisitions is 187 days from announcement to closing. Shareholder votes, SEC filings, and regulatory reviews add significant time and complexity.

Middle market deal timelines are more compressed. Most middle market deals close within 6–12 months from initial engagement to closing, though the due diligence period for businesses in the $5M-$50M sector reached a 5.5 month average in Q1 2025 — the longest ever reported. The negotiation dynamic is far more personal, with sellers who are emotionally invested in the outcome and often concerned about the future of their employees and customers, not just the price.

Regulatory Differences

While large-cap deals face strict SEC disclosure requirements, antitrust reviews (HSR filings with a threshold of $133.9 million effective February 2026), and Sarbanes-Oxley compliance, middle market private deals face fewer regulatory hurdles. However, they still require attention to securities law, state business regulations, tax structuring, and contractual obligations. Those obligations are manageable — but they're rarely the hardest part of getting a deal across the finish line.

Post-Close Integration Challenges

Post-close integration is one of the biggest challenges in middle market M&A. Unlike large corporations with dedicated integration teams and documented systems, many middle market companies lack formal processes. The primary integration risks include:

- Cultural fit — aligning company values and work styles

- Founder transition — managing the emotional and operational handoff

- Employee retention — keeping key talent who may be uncertain about new ownership

- Customer relationship continuity — maintaining trust and service levels

Studies put the share of middle market deals facing significant integration challenges above 40%. Success requires careful planning and transparent communication. A structured transition period — where the seller stays involved — is often what makes the difference between a smooth handoff and a costly disruption.

What Middle Market Sellers Need to Know Before Going to Market

The Importance of Deal Readiness

The most successful middle market sellers begin preparing 3–5 years before they intend to sell. This includes:

- Cleaning up financials — ensuring accurate, audited statements that buyers can trust

- Documenting operations — creating standard operating procedures and process documentation

- Reducing owner dependency — building a management team that can run the business independently

- Retaining key employees — implementing incentive programs to keep critical talent through the transition

- Aligning on valuation expectations — understanding what the business is realistically worth in the current market

A useful rule of thumb: the planning horizon should be 3–5 times the expected execution timeframe. If the sale process takes 12 months, preparation should start years earlier.

Choosing the Right Advisor

Choosing the right advisor is one of the most consequential decisions a middle market seller will make. Unlike large corporations with dedicated in-house M&A teams, most middle market owners navigate a sale for the first time without internal expertise. An experienced business broker or M&A advisor provides:

- Market access — connections to qualified buyers you wouldn't find on your own

- Valuation expertise — ensuring you don't leave money on the table or price too high

- Confidentiality management — protecting your business during the sale process so employees, customers, and competitors don't learn prematurely

- Negotiating leverage — experience navigating complex deal structures and terms

Chelsis Financial works with business owners across manufacturing, distribution, and service sectors — managing the full sale process from initial valuation through closing while keeping the transaction confidential.

Timing the Market

Market conditions in 2026 are particularly favorable for middle market sellers. Improved economic fundamentals, elevated PE dry powder, and a business-friendly regulatory environment create a window of opportunity. Sellers who wait for the window to fully open often find it has already begun to close — preparation now is what determines whether you can move when conditions are right.

Frequently Asked Questions

What is the mid-market in M&A?

The middle market encompasses companies with revenues typically between $10 million and $1 billion (or enterprise values of $100M–$1B). This segment includes privately held, family-owned, and PE-backed businesses that are too large for a simple business sale but too small for Wall Street-style megadeals.

Do mid-cap companies outperform large-cap companies in M&A?

Middle market deals are evaluated on different metrics than public market performance, so direct comparisons have limited value. For buyers, the segment offers attractive valuations, less competition, and significant upside potential. Sellers in a well-run process routinely achieve strong multiples.

What deal size qualifies as a middle market M&A transaction?

Deal size definitions vary, but most practitioners define middle market transactions as having enterprise values between $25 million and $1 billion. The "lower middle market" covers roughly $10M–$100M, and the "core middle market" covers $100M–$500M.

How long does it typically take to close a middle market M&A deal?

Most middle market deals close within 6–12 months from initial engagement to closing, though deal preparation should begin years earlier. Complex deals or those with financing contingencies may take longer.

What types of financing are typically used in middle market acquisitions?

The common financing stack includes senior bank debt, private equity capital, mezzanine/subordinated debt, and seller financing — often layered together in a way that reflects the buyer's risk tolerance and the deal's financial profile.

Why do middle market business owners need a broker or M&A advisor to sell?

Most middle market sellers have never run a sale process before, lack access to qualified buyers, and risk leaving significant value on the table without guidance. A good advisor brings buyer relationships, negotiating leverage, and the confidentiality controls that protect the business while it's being marketed.