Introduction

Most business owners spend years building their company, yet studies suggest the majority enter the sale process without a realistic sense of what it's worth. Without data-backed analysis, many rely on gut feel or emotional attachment. Set the price too high, and your listing stalls. Price it too low, and you leave hundreds of thousands of dollars on the table.

Sale prices vary enormously based on industry, financial performance, size, and valuation method. There is no universal formula. A profitable manufacturer with recurring revenue may command 5x earnings, while a retail business with thin margins might sell for 2x — and knowing where you fall on that spectrum changes everything about how you approach a sale.

This guide covers what you need to make an informed decision:

- Realistic sale price ranges by business size and industry

- The factors that move valuations up or down

- Common valuation methods buyers and brokers actually use

- Practical steps to maximize what you walk away with

Key Takeaways

- Small businesses typically sell for 2–4x Seller's Discretionary Earnings (SDE); mid-market businesses use EBITDA multiples ranging from 4x to 8x depending on industry

- The biggest drivers of sale price are consistent financial performance, reduced owner dependence, and strong growth potential

- Customer concentration and lack of documented processes can reduce valuations by 10–25%

- Starting preparation 12–24 months before listing can add 20–30% to your final sale price and reduce time to close

How Much Can You Sell Your Business For?

There is no fixed sale price for a business. The amount a buyer will pay depends on the size of the business, how it earns money, industry demand, and which valuation method is applied. Two businesses with identical revenue can sell for vastly different amounts based on profitability, operational efficiency, and buyer perception of risk.

What goes wrong when business owners skip proper valuation:

- Overpricing stalls deals - Setting an asking price based on emotional investment or years of sacrifice leads to listings that sit unsold for months or years

- Underpricing leaves money on the table - Without market data, owners may accept offers far below what informed buyers would pay

- Buyers and lenders expect defensible numbers - Without a data-backed valuation, negotiations break down during due diligence when buyers discover the price lacks foundation

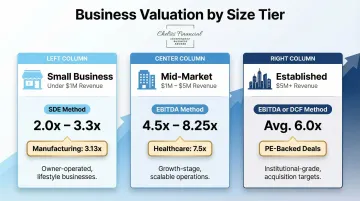

Typical Sale Price Ranges by Business Size

The table below summarizes typical sale price ranges across the three main business tiers, based on data from BizBuySell, the Pepperdine Private Capital Markets Report, and the IBBA Market Pulse Report:

| Business Size | Revenue Range | Valuation Method | Typical Multiple | High-Multiple Sectors |

|---|---|---|---|---|

| Small | Under $1M | Seller's Discretionary Earnings (SDE) | 2.0x–3.3x (median 2.4x) | Manufacturing (~3.13x) |

| Mid-Market | $1M–$5M | EBITDA | 4.5x–8.25x | Healthcare/Biotech (7.5x) |

| Established | $5M+ | EBITDA or DCF | 4.5x–8.25x (avg. 6.0x) | Strategic/PE-backed deals |

Sources: BizBuySell 2024 | Pepperdine Private Capital Markets Report | IBBA Market Pulse Report

What these ranges typically include:

- Goodwill and intangible assets (brand name, customer lists, non-compete agreements)

- Furniture, fixtures, equipment (FF&E)

- Inventory at cost

- Assignable customer and supplier contracts

- A normalized level of working capital

What they typically exclude:

- Cash and cash equivalents (most deals are structured "cash-free, debt-free")

- Business-owned real estate (often sold separately or leased back)

- Seller's personal assets

- Pre-existing liabilities like unpaid taxes or legal claims

Small Business (Under $1M Revenue)

Owner-operated businesses in this tier are valued on the financial benefit a new owner-operator would receive — making SDE the most appropriate metric. These deals fit service businesses, retail shops, trades, and local franchises where the owner is central to daily operations.

What's typically included:

- Equipment, inventory, and customer lists

- Brand goodwill and local market reputation

- Owner's salary add-backs (personal expenses run through the business)

- Transferable vendor relationships

Mid-Market Business ($1M–$5M Revenue)

Buyers at this level pay for predictable earnings and operations that don't depend on the seller. EBITDA is the standard metric because it strips out owner-specific costs and shows what the business actually produces.

What's typically included:

- Documented processes and Standard Operating Procedures (SOPs)

- Management team with defined roles

- Recurring revenue contracts or subscription models

- Intellectual property (patents, trademarks, proprietary software)

Larger or Established Business ($5M+ Revenue)

Strategic buyers and private equity firms target this tier. They pay premiums for businesses with audited financials, a documented growth plan, and operations that can scale — often using DCF analysis to justify higher multiples.

What's typically included:

- Full organizational structure with professional management

- Proprietary assets (technology platforms, exclusive contracts, patents)

- Long-term client contracts with enterprise or institutional customers

- Scalable infrastructure and documented growth strategy

Key Factors That Affect Your Business's Sale Price

The multiple a buyer is willing to apply depends on how they perceive risk and opportunity. The following factors directly move your valuation up or down.

Financial Performance and Consistency

Buyers prioritize businesses with clean books, consistent revenue growth, and healthy profit margins. Erratic financials or poor record-keeping significantly reduce perceived value.

What buyers evaluate:

- Trends, not anomalies — A business showing one "great year" after three mediocre ones raises red flags. Buyers evaluate normalized earnings over 3+ years to identify sustainable performance

- Profit margins relative to industry benchmarks — Thin margins signal operational inefficiency or pricing pressure

- GAAP-compliant financials — Professionally prepared statements increase buyer confidence and streamline due diligence

According to BizBuySell's Insight Report, buyers pay premiums for businesses with clean financials that match tax returns, and poor record-keeping is a primary reason deals fail in the Main Street market.

Clean financials get you to the table — but how the business runs without you determines whether buyers stay.

Owner Dependence and Operational Independence

A business that runs primarily through the owner's relationships, skills, or daily involvement is a riskier acquisition. Reducing owner dependence increases buyer confidence and sale price.

Businesses with high key-person risk face valuation discounts of 10–25% according to valuation literature and court precedents. Approximately 35% of business listings terminate without closing, with lack of management depth cited as a key reason, per the Pepperdine Private Capital Markets Report.

What improves valuation:

- Documented Standard Operating Procedures (SOPs) that enable any qualified manager to run operations

- A capable management team with defined roles and decision-making authority

- Transferable customer relationships (customers buy from the company, not the owner personally)

Growth Potential and Market Position

Businesses in growing industries, with scalable models or proprietary advantages, attract higher multiples. Buyers pay premiums for future earnings potential, not just historical performance.

What drives premium valuations:

- Market leadership — A dominant player in a niche market commands higher multiples than a follower in the same space

- Proprietary advantages — Patents, exclusive contracts, and proprietary technology create lasting competitive advantages that buyers are willing to pay for

- Recurring revenue models — Subscription-based businesses or those with monitoring contracts can command 2x–3x higher multiples than transaction-based models

According to industry data, SaaS companies with recurring revenue models command 7x–12x Annual Recurring Revenue (ARR) for larger, growing firms—substantially higher than typical SDE or revenue multiples in traditional businesses.

Customer and Supplier Concentration Risk

If one customer accounts for a large share of revenue, or a single supplier is critical to operations, buyers discount for that risk.

Risk thresholds:

- A single customer representing 10% of revenue signals initial concern

- 20% concentration triggers heightened scrutiny

- 25%+ concentration represents material risk

- 40%+ concentration represents substantial risk to profitability

Impact on valuation:

According to advisory firm Highland Global's guidance, potential discounts include:

- 10% discount for 25–35% concentration

- 15–20% discount for 36–50% concentration

- 25–35% discount (or fundamental deal restructuring) for concentrations exceeding 50%

How buyers mitigate this risk:

Rather than applying a simple discount, buyers typically restructure deals using earnouts, seller financing tied to customer retention, or escrows where a portion of the purchase price is held until customer transition is confirmed.

Sellers who can demonstrate revenue spread across 10+ customers — with no single account above 15% — rarely face concentration-related deal restructuring.

Intangible Assets

Brand recognition, customer loyalty, proprietary technology, and long-standing vendor relationships add value beyond what appears on the balance sheet.

How intangibles increase value:

- Brand recognition creates pricing power and customer loyalty, reducing marketing costs and supporting predictable revenue

- Proprietary IP offers tax amortization benefits to buyers, increasing the asset's effective value by approximately 20%

- Customer relationships documented in CRM systems demonstrate transferability and reduce buyer risk

- Vendor exclusivity or favorable terms create competitive advantages that justify higher multiples

A business with strong intangibles — documented IP, a recognizable brand, and CRM-tracked customer history — often commands a multiple 0.5x–1x higher than an otherwise identical company without them.

How Business Valuation Methods Work

Business valuation methods vary based on your company's size, industry, and financial structure. Each approach serves a different purpose — and most sellers benefit from understanding at least two or three before entering the market.

Seller's Discretionary Earnings (SDE) Method

Best for: Small, owner-operated businesses

Formula:

Business Value = SDE × Multiple

Where SDE = Net Profit + Owner's Salary + Interest + Depreciation + Amortization + Other Discretionary/Non-recurring Expenses

SDE represents the total financial benefit a single owner-operator would derive from the business. It adds back the owner's salary, non-cash expenses, one-time costs, and owner perks to net profit — giving buyers a clear picture of true earning power.

Typical multiples:

According to BizBuySell's 2024 data, small businesses typically sell at:

- 2.0x SDE for deals under $500K

- 2.8x SDE for deals between $500K–$1M

- 3.3x SDE for deals between $1M–$2M

The multiple reflects risk, growth potential, and industry norms. Manufacturing businesses command higher multiples (3.13x) while restaurants average lower (2.25x).

EBITDA Multiple Method

Best for: Mid-market businesses

Formula:

Business Value = Adjusted EBITDA × Multiple

Where EBITDA = Earnings Before Interest, Taxes, Depreciation, and Amortization

EBITDA strips out non-operational costs to show true earning power. A market-derived multiple is then applied based on industry benchmarks and comparable sales data.

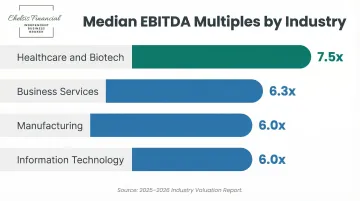

Industry-specific multiples (2025-2026 data):

| Industry | Median EBITDA Multiple | Source |

|---|---|---|

| Healthcare & Biotech | 7.5x | Pepperdine Private Capital Markets Report |

| Business Services | 6.3x | Pepperdine Private Capital Markets Report |

| Manufacturing | 6.0x | Pepperdine Private Capital Markets Report |

| Information Technology | 6.0x | Pepperdine Private Capital Markets Report |

These figures represent median values for companies with $1M–$5M in EBITDA. Actual multiples shift based on industry, growth rate, and buyer type — strategic acquirers often pay more than financial buyers.

Market-Based (Comparable Sales) Method

Best for: Benchmarking and validation

This approach compares your business to recently sold companies in the same industry with similar size and characteristics. It's useful for pressure-testing a valuation, but works best alongside income-based methods rather than on its own.

Limitation:

Two businesses in the same industry with similar revenue can be valued very differently based on profitability, operational quality, customer concentration, and owner dependence. What drives value is earnings quality and risk profile, not top-line revenue.

Asset-Based Method

Best for: Asset-heavy businesses (manufacturing, real estate holding companies)

Formula:

Business Value = Total Assets − Total Liabilities

This method calculates value based on the net book value of tangible assets — equipment, inventory, real estate — plus intangible assets like goodwill and brand equity.

When to use:

- Businesses undergoing liquidation

- Asset-intensive firms where tangible assets drive value

- Distressed or unprofitable companies where future earnings are uncertain

Limitation:

This method significantly undervalues profitable service businesses with few physical assets, as it ignores future earning power and intangible value drivers like customer relationships and brand recognition.

Discounted Cash Flow (DCF) Method

Best for: Businesses with predictable, multi-year revenue streams

DCF projects future cash flows over 5–10 years and discounts them to present value using a rate that reflects the business's risk profile. The higher the risk, the higher the discount rate — and the lower the resulting valuation.

Simplified example:

Year 1 projected cash flow: $500,000

Year 2 projected cash flow: $550,000

Year 3 projected cash flow: $600,000

Discount rate (cost of capital): 15%

Present Value Calculation:

- Year 1: $500,000 ÷ 1.15 = $434,783

- Year 2: $550,000 ÷ (1.15)² = $416,335

- Year 3: $600,000 ÷ (1.15)³ = $394,476

Terminal Value (assuming 3% perpetual growth):

Terminal Value = $600,000 × 1.03 ÷ (0.15 − 0.03) = $5,150,000

Present Value of Terminal Value = $5,150,000 ÷ (1.15)³ = $3,385,416

Total Business Value: $434,783 + $416,335 + $394,476 + $3,385,416 = $4,631,010

Final adjustment:

For private firms, apply an illiquidity discount (a markdown reflecting that private companies can't be sold as quickly as public stock) of 20–30%, resulting in a final valuation of approximately $3.2M–$3.7M. That range becomes your negotiating baseline — not a ceiling.

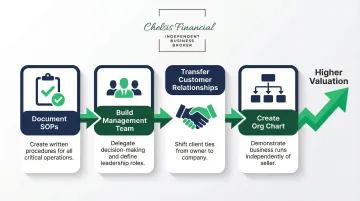

How to Maximize Your Business's Sale Price

The sale price you achieve is not fixed at the time of listing. Preparation done 12–24 months in advance can meaningfully increase your valuation.

Key steps to take before going to market:

Strengthen Financial Performance

- Reduce unnecessary expenses that don't contribute to revenue

- Diversify revenue streams to reduce concentration risk

- Resolve outstanding debts and clean up the balance sheet

- Ensure financials are GAAP-compliant and professionally prepared

Reduce Owner Dependence

- Build and document Standard Operating Procedures (SOPs) for all critical processes

- Develop your management team and delegate decision-making authority

- Ensure key customer relationships are transferable rather than owner-held

- Create an org chart showing the business can operate without you

Work With Professional Advisors Early

A business broker or M&A advisor can identify overlooked value drivers, connect you with the right buyer pool, and negotiate better deal terms. The earlier you engage an advisor, the more runway you have to address gaps that would otherwise compress your price.

Chelsis Financial offers a complimentary Assessment of Value for business owners who want a clear, objective picture of what their business is worth before going to market.

Common Seller Mistakes That Hurt Your Valuation

Three mistakes consistently reduce what sellers walk away with — and all three are avoidable with the right preparation.

Pricing on Emotion Instead of Market Data

Buyers pay for future earnings, not the owner's sacrifice or personal history. Emotional pricing leads to overpriced listings that sit unsold — or underpriced deals that leave real money on the table.

Focusing on Revenue While Ignoring Profitability

High revenue with thin margins won't attract strong offers. Buyers assess Seller's Discretionary Earnings (SDE) or EBITDA, not top-line sales.

A $5M revenue business generating $300K in earnings is worth less than a $2M revenue business generating $500K. The profit is what gets purchased.

Skipping Preparation and Letting Confidentiality Slip

Messy books and undocumented processes erode buyer confidence before negotiations even begin. Worse, premature disclosure to employees, customers, or competitors can destabilize the business mid-sale.

According to the IBBA Market Pulse Report, poor financials account for 43% of deal failures in transactions under $500K — and unrealistic seller expectations drive another 23%.

Conclusion

The amount you can sell your business for depends on a combination of financial performance, market conditions, valuation method, and how well you've prepared the business for a buyer's scrutiny. There is no single answer, but there is a right process.

Working with experienced advisors gives business owners the best chance of achieving maximum value. Chelsis Financial guides sellers through every stage—from establishing a defensible valuation to connecting with qualified buyers and closing the deal—with full confidentiality throughout. If you're ready to find out what your business is worth, a complimentary assessment is a practical first step.

Frequently Asked Questions

How do you calculate the value of your business to sell?

Business value is calculated by applying a valuation method appropriate to the business's size and industry—typically SDE multiples for small businesses, EBITDA multiples for mid-market firms, or DCF analysis for larger companies—using verified financial data and comparable market transactions.

How much is a business worth with $1,000,000 in sales?

Value depends on profitability and industry multiple, not revenue alone. A business with $1M in sales could be worth anywhere from $500K to $4M+ depending on profit margins, growth trajectory, and the applicable revenue or earnings multiple for that industry.

What is a good multiple to sell a business for?

"Good" multiples vary by industry and size. Small businesses often sell at 2–4x SDE, while mid-market businesses may command 4.5x–8x EBITDA depending on sector. BizBuySell and IBBA market data consistently show manufacturing and healthcare businesses commanding higher multiples than retail or food service.

What documents do I need to sell my business?

Key documents include three years of tax returns, profit and loss statements, balance sheets, customer contracts, lease agreements, documented SOPs, payroll records, and debt agreements. Clean, organized documentation accelerates due diligence and supports your asking price.

How long does it take to sell a business?

Most business sales take 6–12 months from initial valuation to closing, according to the IBBA Market Pulse Report. Well-prepared businesses with clean financials and professional representation tend to close at the shorter end of that range.

Should I use a business broker to sell my business?

Business brokers bring buyer networks, valuation expertise, and negotiation experience that typically result in higher sale prices. The IBBA reports broker-represented transactions close at roughly 50% success rates, versus 25–30% for businesses listed without representation—meaning you're nearly twice as likely to close with a broker.