Introduction

Imagine you're preparing to sell the business you've built over the past decade. Your tax return shows a modest $75,000 profit—but that figure doesn't account for your $120,000 salary, the $18,000 you spent on your personal truck, or the $12,000 one-time legal settlement. To a buyer evaluating your business, that $75,000 tells a misleading story.

This is where Seller's Discretionary Earnings (SDE) comes in. Unlike taxable profit, SDE captures the total financial benefit your business generates—including your salary, personal expenses run through the company, and one-time costs. Buyers and brokers rely on SDE to determine what a business is truly worth.

This guide covers:

- The SDE definition and why it matters in a sale

- The formula and step-by-step calculation process

- How SDE differs from EBITDA

- How to use SDE to maximize your sale price

- A calculator to run the numbers on your own business

TLDR: Key Takeaways

- SDE captures the total financial benefit a business generates for its owner—salary, perks, and discretionary spending included

- Formula: Net Profit + Owner's Salary + Depreciation & Amortization + Interest + Discretionary Expenses + Non-Recurring Expenses = SDE

- SDE is the standard valuation metric for small businesses under $5–10M in revenue, while larger companies typically use EBITDA

- Business value = SDE × Multiple (typically 2x–4x for small businesses)

- Well-documented SDE calculations build buyer confidence and support stronger sale prices

What Is Seller's Discretionary Earnings (SDE)?

Seller's Discretionary Earnings (SDE) is a cash-flow-based profitability metric that captures the total economic benefit an owner receives from their business. According to the International Business Brokers Association (IBBA), SDE includes not just salary, but also personal expenses run through the company, non-cash charges like depreciation, and one-time costs. It reflects what a new owner would earn by stepping directly into the seller's role.

Why SDE Exists

Standard accounting statements—tax returns and P&Ls—are often structured to minimize taxable income, not showcase earning power. Business owners run personal expenses through the company to reduce their tax burden. Research shows that 60% of businesses with under $1M in earnings commingle personal and business finances, distorting reported profitability.

SDE normalizes those financials by adding back items that obscure true earning power, including:

- Owner's salary and personal expenses run through the business

- Non-cash charges such as depreciation and amortization

- One-time or non-recurring costs (legal settlements, equipment write-offs)

- Discretionary spending that a new owner wouldn't replicate

The result is a clearer picture of the cash the business actually generates — which is what buyers are paying for.

When SDE Is Used

SDE is the standard valuation metric for small to mid-sized business (SMB) mergers and acquisitions, particularly for businesses generating under $5–10M in annual revenue. It's most relevant for owner-operated businesses where the owner is actively involved in daily operations. A buyer stepping into that role inherits the owner's full income stream.

What's Included in SDE: The Key Add-Back Categories

"Add-backs" are expenses subtracted from income on the P&L but added back when calculating SDE because they either benefit the owner personally or are unlikely to recur under new ownership. Each add-back must be thoroughly documented to be defensible to buyers and lenders.

Owner's Compensation and Benefits

The owner's salary, bonuses, and associated payroll taxes are added back because compensation levels vary widely between owners. A new buyer may pay themselves differently. SDE normalizes this by including the full owner compensation package rather than assuming a "market rate" replacement salary.

When multiple owners are involved, only one full-time owner's salary is added back. Additional owner salaries are adjusted to market-rate replacement cost.

Personal Expenses Run Through the Business

Common examples of personal discretionary expenses that owners route through the business include:

- Personal vehicle use and lease payments

- Cell phone plans for family members

- Home office expenses

- Personal travel and entertainment

- Health insurance premiums

- Family member salaries above market rate

Since these expenses benefit the owner personally rather than core operations, they don't reflect what a new buyer would actually spend.

Non-Cash Expenses (Depreciation and Amortization)

Depreciation and amortization (D&A) reduce accounting profit but don't represent actual cash leaving the business in the current period. Because SDE aims to reflect real cash flow available to the owner, D&A is added back.

Non-Recurring and One-Time Expenses

Non-recurring expenses are one-time costs unlikely to appear again under new ownership:

- Litigation or legal settlement fees

- One-time equipment purchases or major repairs

- Consulting fees for specific projects

- Extraordinary repair expenses (flood, fire damage)

These are added back because they distort the picture of ongoing earnings.

Interest Expense

Interest expense reflects the current owner's financing decisions and capital structure, which a new buyer will likely restructure. Adding it back allows buyers to evaluate the business independent of the seller's debt obligations.

SBA Lender Scrutiny

SBA 7(a) lenders heavily scrutinize add-backs during underwriting because inflated SDE can cause the loan to fail underwriting. Under SBA SOP 50 10 8, lenders must justify all additions and subtractions — including unfunded capital expenditures, non-recurring income, and owner's draws.

Add-back treatment varies significantly depending on documentation:

| Add-Back Type | Lender Treatment |

|---|---|

| Owner's salary (documented) | Generally accepted |

| D&A (on financial statements) | Accepted |

| One-time legal/repair costs | Accepted with invoices |

| Meals, entertainment, travel | Rejected unless purely personal |

| Family salaries above market | Requires market-rate justification |

Every claimed add-back must be supported by receipts, invoices, or payroll records.

The SDE Formula and How to Calculate It Step by Step

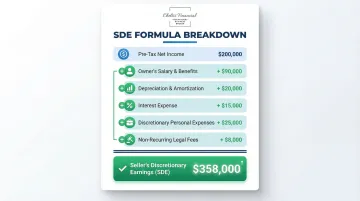

The standard SDE formula is:

SDE = Pre-Tax Income + Owner's Compensation + Depreciation & Amortization + Interest Expense + Discretionary Expenses + Non-Recurring Expenses

Why Pre-Tax Income Is the Starting Point

The calculation begins with Pre-Tax Income (Earnings Before Taxes) rather than Net Income. This removes the effect of different tax structures across entity types — S-Corps, C-Corps, LLCs, and Sole Proprietorships all report differently. Since a buyer will operate under their own capitalization and tax setup, pre-tax income puts all businesses on a comparable footing.

Step-by-Step Calculation Walkthrough

Here's how the calculation works using a sample service company:

| Line Item | Amount |

|---|---|

| Pre-Tax Income (Net Profit) | $200,000 |

| + Owner's Salary | $90,000 |

| + Depreciation & Amortization | $20,000 |

| + Interest Expense | $15,000 |

| + Discretionary Personal Expenses | $25,000 |

| + Non-Recurring Legal Fees | $8,000 |

| = Seller's Discretionary Earnings (SDE) | $358,000 |

This $358,000 figure represents the total financial benefit the business generates for its owner, and it's the number buyers use to estimate business value.

Using Last Twelve Months (LTM) and 3-Year Averages

SDE is generally calculated using the Last Twelve Months (LTM) of financials. That said, buyers and brokers usually want 3 years of data to evaluate whether performance is consistent or trending. Most will average the 2-3 most recent years to smooth out anomalies before settling on a valuation number.

Important: Inconsistencies between tax returns and internal financials should be investigated. Quality of Earnings discrepancies accounted for 21.3% of failed transactions post-LOI in 2025.

Common Mistakes to Avoid

The most frequent errors sellers make include:

- Counting the same expense twice across different add-back categories

- Labeling routine costs as "one-time" items when they recur annually

- Claiming add-backs without receipts, invoices, or payroll records to support them

- Overstating owner compensation with figures no replacement manager would command

Unsupported add-backs erode buyer trust quickly — and approximately 25% of failed transactions collapse because sellers cannot provide clean financial statements during due diligence.

SDE vs. EBITDA: Key Differences

Both EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) and SDE normalize earnings for comparison, but they serve different audiences and business sizes.

The Critical Distinction: Owner Compensation

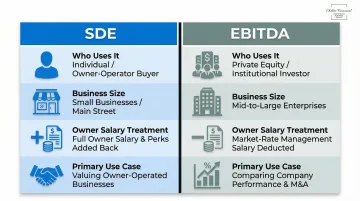

The single most important difference is how each metric treats the owner's salary:

- SDE adds back the owner's full compensation (salary + personal perks), so a buyer stepping into the role captures the total financial benefit of the position

- EBITDA deducts a market-rate replacement salary instead, assuming a professional management team will run the company post-acquisition

Comparison Table

| Metric | Who Uses It | Business Size | Owner Salary Treatment | Primary Use Case |

|---|---|---|---|---|

| SDE | Individual buyers, small business brokers | Under $5–10M revenue | Adds back full owner compensation | Owner-operated SMB M&A |

| EBITDA | Institutional investors, private equity | Over $5–10M revenue | Deducts market-rate replacement salary | Middle-market and corporate M&A |

The $2M to $5M Transition Zone

According to the IBBA Market Pulse report, SDE is the dominant valuation method for deals under $2 million in enterprise value. Between $2 million and $5 million, the landscape is mixed, with both SDE and EBITDA used depending on whether the buyer is an individual or an institution. For transactions above $5 million, EBITDA dominates.

Critical: Applying an EBITDA multiple to an SDE cash flow figure artificially inflates the valuation and guarantees deal failure.

How SDE Is Used to Value a Small Business

The SDE Multiple Method

Business value is estimated by multiplying SDE by an industry-specific multiple, typically ranging from 2x to 4x for small businesses. Higher multiples reflect lower risk, stronger growth trends, recurring revenue, and less owner dependency.

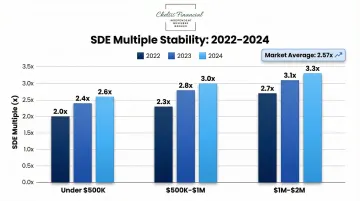

2022-2024 SDE Multiple Stability

Despite severe macroeconomic headwinds and rising interest rates, SDE multiples for Main Street businesses held steady from 2022 through 2024:

| Enterprise Value Tier | 2022 Average | 2023 Average | 2024 Average |

|---|---|---|---|

| Under $500K | 2.0x | 2.0x | 2.0x |

| $500K - $1M | 2.8x | 2.8x | 2.8x |

| $1M - $2M | 3.0x | 3.0x | 3.0x |

According to BizBuySell, average SDE multiples across all sectors range from 2.0x to 3.3x, with an overall average of 2.57x.

What Increases or Decreases the SDE Multiple

Specific risk factors push a company's multiple to the top or bottom of its range:

Factors that increase multiples:

- Diversified customer base (no single customer over 15% of revenue)

- Documented systems and processes that reduce owner dependency

- Strong profit margins and consistent growth trends

- Recurring revenue contracts

- Transferable customer relationships

Factors that decrease multiples:

- Customer concentration risk (a single customer exceeding 35% of revenue frequently terminates deals)

- High owner dependency without documented systems

- Declining revenue trends or inconsistent performance

- Low profit margins relative to industry benchmarks

Get Your Business Valued

Chelsis Financial offers a Complimentary Assessment of Value to help sellers understand their SDE and estimated business value before going to market. The assessment delivers a market-supported asking price grounded in financial analysis and comparable transaction data, so you go to market with a number buyers can validate and sellers can defend.

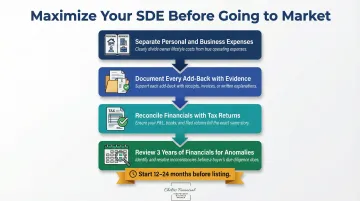

How to Maximize Your SDE Before Selling

Maximizing SDE isn't about inflating numbers—it's about accurately presenting all the financial benefits your business provides, many of which are routinely underreported or buried in the books. Begin this process at least 12–24 months before listing.

Four Actionable Steps

Separate personal and business expenses clearly Make add-backs transparent by maintaining distinct categories in your accounting system. This allows buyers to easily verify which expenses benefit the owner personally versus the business operations.

Document every add-back with supporting evidence Gather invoices, receipts, and payroll records for all add-backs. Businesses with complete, clean documentation receive 2.3x more offers and achieve 15-20% premium valuations.

Clean up bookkeeping so financials reconcile with tax returns Ensure your internal P&Ls match your tax returns. Discrepancies raise red flags during due diligence and can derail deals.

Review 3 years of financials to identify and explain anomalies Buyers will scrutinize trends and inconsistencies. Prepare clear explanations for any unusual expenses, revenue spikes, or one-time events.

Work With an Experienced Broker Early

An experienced business broker can identify add-backs you may have overlooked and help structure your financials in a way that holds up under buyer scrutiny. Look for a broker with direct experience in your industry and a verified network of pre-qualified buyers—not just a listing service.

Chelsis Financial, for example, offers a complimentary business valuation assessment and works with Midwest business owners through the full process, from initial SDE preparation to closing. Starting that conversation 12–18 months before your target sale date gives you the most room to strengthen your numbers.

Frequently Asked Questions

What are seller's discretionary earnings?

Seller's Discretionary Earnings (SDE) is the total financial benefit a business owner derives from their company—including salary, personal perks, non-cash charges like depreciation, and one-time expenses. It reflects the true earning power of a small, owner-operated business.

What is included in seller's discretionary earnings and how is SDE calculated?

SDE starts with pre-tax net profit and adds back owner's compensation, D&A, interest expense, personal/discretionary expenses, and non-recurring costs. The formula is: SDE = Net Profit + Owner's Salary + D&A + Interest + Discretionary + Non-Recurring Expenses.

How does seller's discretionary earnings (SDE) differ from profit and EBITDA?

Net profit excludes owner add-backs entirely. EBITDA excludes owner compensation from its adjustments, assuming a market-rate manager will be hired. SDE adds back the full owner's salary and personal perks, making it the right metric when the buyer is stepping into the owner's role.

How do you value a small business based on seller's discretionary earnings?

Business value is typically estimated by applying a multiple (often 2x–4x) to SDE. The multiple varies based on industry, business risk, growth trends, customer concentration, and owner dependency. For example, a business with $300,000 in SDE and a 3x multiple would be valued at $900,000.

What is a good SDE percentage?

There is no universal "good" SDE percentage, but healthy SDE margins typically vary by industry. Service businesses often achieve 25-35% SDE margins, while retail businesses may see 10-20%. Higher SDE margins signal stronger profitability and typically command better valuation multiples.

What is an example of seller's discretionary earnings?

If a business has a net profit of $150,000, owner salary of $80,000, $15,000 in personal vehicle expenses, and $10,000 in one-time legal fees, the SDE would be $255,000. This $255,000 figure—not the $150,000 net profit—is what buyers use to estimate business value.