Introduction

Most service business owners have no idea what their company is worth until they sit down to sell—and by then, the best opportunities to maximize value have already passed. Whether you're running an HVAC company, a consulting firm, or a healthcare practice, the difference between a mediocre exit and a premium sale often comes down to one thing: understanding how buyers value your business years before you're ready to sell.

Service businesses present unique valuation challenges. Unlike manufacturers with physical assets or retailers with inventory, your company's worth rests almost entirely on intangibles: customer relationships, recurring revenue streams, documented processes, and the strength of your management team.

These factors don't show up neatly on a balance sheet, yet they determine whether you'll command a 4x or an 8x multiple when the time comes to exit.

This guide covers how EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is used to value service businesses, what typical multiples look like across industries, and what you can do starting today to influence the outcome.

Key Takeaways

- Service businesses are valued using EBITDA multiplied by an industry-specific multiple

- Private service company multiples typically range from 4x to 10x depending on size, industry, and quality

- Higher EBITDA, lower owner-dependence, and recurring revenue push multiples higher

- A formal valuation reveals your current multiple, what's suppressing it, and what a realistic sale price looks like

What Is EBITDA—And Why It's the Foundation of Service Business Valuation

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It measures core operating profitability by stripping out financing decisions, tax strategies, and non-cash accounting entries.

For buyers, EBITDA shows the cash-generating power of your operation—independent of how you've structured debt or managed your tax bill.

Why EBITDA Beats Net Income for Valuation

Net income is easily distorted. Many service business owners run personal expenses through the company, pay themselves above or below market rates, or absorb one-time costs that won't recur under new ownership. EBITDA—or more precisely, normalized EBITDA—corrects for these distortions and shows what the business actually earns when run by a professional buyer.

The Power of EBITDA Normalization

Normalization—also called "add-backs"—can materially lift your calculated valuation by removing costs that won't transfer to a new owner. Common add-backs include:

- Above-market owner compensation — If you pay yourself $250,000 but a replacement manager costs $120,000, that $130,000 difference gets added back

- Personal expenses — Vehicle costs, travel, meals, or family member salaries unrelated to operations

- One-time costs — Legal settlements, equipment write-offs, or pandemic-related expenses that won't repeat

- Discretionary spending — Country club memberships, personal insurance, or other owner perks

Critical warning: Buyers aggressively scrutinize add-backs during due diligence. Unsupported or aggressive add-backs are a leading cause of broken deals. Document everything and benchmark owner comp against objective market rates.

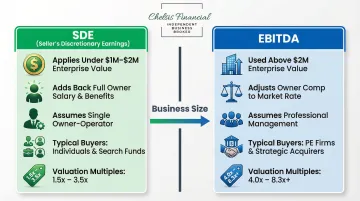

SDE vs. EBITDA: Which Applies to Your Business?

The valuation metric shifts based on business size:

Seller's Discretionary Earnings (SDE):

- Applies to businesses under $1M–$2M in enterprise value

- Adds back the owner's full salary and benefits

- Assumes a single owner-operator will run the business

- Typical buyers: individuals, search funds, local competitors

- Multiples: 1.5x–3.5x

EBITDA:

- Used for businesses above $2M in enterprise value

- Adjusts owner comp to fair market replacement rate

- Assumes professional management

- Typical buyers: private equity, strategic acquirers, family offices

- Multiples: 4.0x–8.3x+

According to the Pepperdine Private Capital Markets Report, 73% to 76% of investment bankers and appraisers in the lower-middle market use recast EBITDA multiples as their primary valuation method.

The Basic Valuation Formula

Business Value = Normalized EBITDA × Multiple

Example: Your consulting firm generates $750,000 in normalized EBITDA. Comparable transactions in your industry show a 5.0x multiple. Your implied enterprise value is $3.75 million.

That multiple—5.0x in this example—is not fixed. It shifts based on industry, business size, and qualitative factors like customer concentration, recurring revenue, and management depth. Those factors are what the rest of this guide addresses.

How to Value a Service Business: Key Valuation Methods

Three Main Approaches

Professional valuations use three frameworks: income-based, market-based, and asset-based methods. For operating service businesses, the first two dominate.

EBITDA Multiple Method — The most widely used approach in private M&A. It values normalized earnings using a market-derived multiple—practical, transaction-grounded, and directly aligned with how buyers size up deals.

Discounted Cash Flow (DCF) — Projects future cash flows and discounts them to present value using a risk-adjusted rate. More complex and forward-looking, typically reserved for larger businesses or high-growth scenarios where historical earnings don't capture future potential.

Market-Based Method:

This approach examines actual sale prices from comparable private transactions to establish benchmark multiples. Brokers and buyers rely on databases like BizBuySell and private M&A transaction data to set expectations. The challenge: finding truly comparable deals with similar size, geography, customer mix, and business model.

Asset-Based Method:

This calculates book value (assets minus liabilities). Rarely used for operating service businesses because it misses intangible value—customer relationships, brand equity, workforce expertise—which account for the majority of value in asset-light companies. Most relevant in distressed or liquidation scenarios.

Which Method Should You Use?

For most small-to-mid-sized service businesses, the EBITDA or SDE multiple method aligned to comparable transactions is the most practical starting point. That said, the accuracy of any valuation hinges on normalized earnings calculated correctly. A few factors determine whether you land at the right number:

- Access to real, comparable transaction data (not public estimates)

- Knowing which add-backs buyers will actually accept

- Understanding how your industry, size, and customer concentration affect the multiple

Self-calculated valuations frequently miss these nuances. A professional assessment—like the complimentary valuation Chelsis Financial offers—gives you a defensible number grounded in actual market data before you enter any conversation with a buyer.

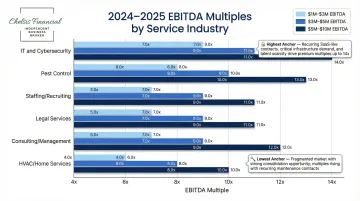

EBITDA Multiples by Service Industry: What the Data Shows

Private service company M&A data reveals that multiples vary significantly by industry and by earnings scale. Larger EBITDA commands higher multiples because buyers gain confidence in cash flow stability and operational resilience.

The Size Premium

According to the 2025 Pepperdine Private Capital Markets Report, multiples scale with business size:

- $0–$1M EBITDA: 4.0x average

- $1M–$5M EBITDA: 6.1x average

- $5M–$10M EBITDA: 6.6x average

- $50M+ EBITDA: 8.3x or higher

GF Data reports similar trends: "very small" deals ($1M–$10M total enterprise value) average 5.5x–5.6x trailing EBITDA, while the $10M–$25M tier jumps to 6.2x–6.7x.

Industry-Specific Multiples (2024-2025 Data)

| Industry | $1M–$3M EBITDA | $3M–$5M EBITDA | $5M–$10M EBITDA | Key Value Drivers |

|---|---|---|---|---|

| HVAC / Home Services | 4.5x – 5.1x | 5.9x – 7.9x | 7.0x – 9.8x | Recurring maintenance contracts, PE demand, recession resistance |

| Consulting / Management | 4.3x – 9.9x | 6.4x – 11.6x | 8.4x – 13.4x | Niche specialization, retainer clients, low owner dependence |

| Legal Services | 5.7x – 10.2x | 7.0x – 12.0x | 9.7x – 13.5x | Brand reputation, institutional clients, partner transition plans |

| Staffing / Recruiting | 4.7x | 6.5x | 7.4x | Contract stability, specialized labor pools, diversified clients |

| Pest Control | 5.0x | 6.4x | 8.2x | High margins (45%+), route density, subscription revenue |

| IT & Cybersecurity | 9.6x | 11.4x | 13.2x | Managed service contracts, proprietary processes, switching costs |

Sources: First Page Sage, Axial

Sector Trends to Watch

HVAC and Home Services: Private equity participation in HVAC deals surged from 8% in 2023 to 23% in 2024, driving multiple expansion. Recurring maintenance agreements and recession-resistant demand make these businesses highly attractive for roll-up strategies.

Insurance Brokerage: Sits among the highest-multiple sectors because revenue renews automatically — policy holders rarely switch brokers, and commission trails persist for years. From 2022 through 2025, insurance services averaged 16.2x EV/EBITDA.

Healthcare Services: An aging population keeps buyer demand strong across healthcare. Practices with $5M+ EBITDA often trade 2–4x higher than smaller add-ons, with established platforms reaching 10x–12x EBITDA.

When Revenue Multiples Replace EBITDA

Revenue multiples (typically 0.5x–2.0x) are used when:

- EBITDA is negative or inconsistent

- Businesses are very small (Main Street category)

- Strategic buyers value customer base over current profitability

BizBuySell data shows average revenue multiples around 0.67x across small businesses, ranging from 0.42x to 1.2x by sector.

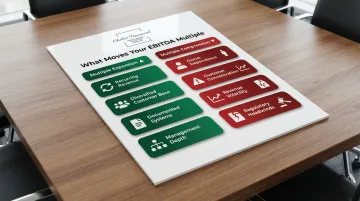

What Drives Your EBITDA Multiple Up or Down

Industry and size set the baseline, but qualitative factors determine where your multiple actually lands. Two HVAC companies with identical EBITDA can receive offers that differ by 3–4 multiple turns — here's what separates them.

Multiple Expansion Drivers

- Recurring revenue — Retainer agreements, long-term contracts, and subscription models reduce buyer risk. Businesses with 60%+ recurring revenue consistently command premium multiples.

- Diversified customer base — Buyers typically pull back when a single client exceeds 15%–20% of revenue. Research shows concentration above 25% triggers severe discounts or deal termination.

- Documented systems — Written processes and SOPs mean institutional knowledge doesn't walk out the door with the owner, which directly lowers transition risk for buyers.

- Management depth — A business that runs without daily owner involvement attracts institutional buyers. An operations manager, sales director, or CFO signals the company can grow without you.

Multiple Compression Factors

- Heavy owner-dependence — If you're the primary salesperson, key client contact, and operational decision-maker, expect significant discounts or earnouts structured to ensure the business survives your exit.

- Concentrated customer base — One client at 30% of revenue is a "revenue cliff." Diversification should start 2–3 years before a planned sale — not the year of.

- Revenue volatility — Year-over-year swings signal operational instability. Buyers discount unpredictable cash flows because acquisition lenders do too.

- Undocumented processes — When critical knowledge exists only in employees' heads, buyers price in the real risk: key people leave, processes break down, clients churn.

- Regulatory headwinds — Industries under regulatory pressure or facing technological disruption receive lower multiples regardless of current profitability.

The Size Premium Effect

Beyond these qualitative factors, scale compounds everything. According to Pepperdine research, companies with higher absolute EBITDA consistently attract higher multiples from private equity and strategic buyers — they have deeper management teams, broader customer bases, and more resilient cash flows. Crossing the $5M EBITDA threshold unlocks access to institutional capital and the valuations that come with it.

How to Increase Your Service Business Valuation Before You Sell

The best time to prepare for a sale is 1–2 years before you go to market. Changes in business structure, contract terms, and financial reporting need time to show up in the trailing earnings history that buyers rely on.

Three Highest-Impact Levers

Build Recurring Revenue — Convert project-based work to retainer or subscription models with auto-renewal clauses. Buyers pay premium multiples for predictable cash flows, so document renewal rates and contract stability.

Reduce Owner-Dependency — Hire or promote a management layer that can run operations without you. Transition key sales relationships to a team, document processes, and aim to step into an absentee role 12–18 months before going to market.

Clean Up Financials — Ensure EBITDA is clearly documented with defensible add-backs, personal expenses removed, and owner compensation benchmarked to market rates. If you're approaching $2M in enterprise value, engage a CPA for GAAP-compliant financials.

The cleaner your books and the more transferable your operations, the stronger your multiple.

Address Customer Concentration Early

If one or two clients represent more than 15% of revenue, diversification is your highest priority. Strategies include:

- Aggressive new client acquisition in adjacent markets

- Launching new service lines to attract different customer segments

- Securing long-term, transferable contracts with concentrated customers to mitigate risk

Start Early

According to exit planning research, advisors recommend a 3–5 year preparation window to maximize outcomes. Buyers base valuations on trailing twelve months (TTM) to 36 months of historical performance. Start now — every improvement needs time to build into the numbers a buyer will actually see.

When to Work With a Business Broker for Your Valuation

Professional assessment becomes essential when:

- You're preparing to sell and need a defensible number that holds up under buyer scrutiny

- You're seeking financing or a partner — lenders and investors require certified valuations

- Retirement, a health event, or a partnership dispute makes knowing your exact value urgent

The Cost of Guessing

98% of small business owners don't know their company's value. Self-calculated valuations frequently miss the mark because owners lack access to real comparable transaction data and don't know which add-backs buyers will accept. The result: 70% of businesses fail to sell because sellers overprice while buyers discount based on actual financial risk.

Chelsis Financial's Complimentary Assessment of Value

For service business owners who want to know what their company is worth before committing to a full sale process, Chelsis Financial offers a Complimentary Assessment of Value. It includes:

- Normalized EBITDA calculation with defensible add-backs

- Industry-specific multiple benchmarking based on real transaction data

- Identification of value drivers and risks that impact your multiple

- Strategic recommendations to maximize value before sale

Chelsis Financial works with a network of qualified buyers across the Midwest, supporting owners from the initial valuation through closing. Call 866-842-5151 to schedule your complimentary assessment.

Frequently Asked Questions

How much does a service business sell for?

Service businesses typically sell for a multiple of their normalized EBITDA or SDE. Most private transactions fall in the 3x–8x EBITDA range depending on industry, size, and profitability. Larger, more systemized businesses with recurring revenue and professional management teams command multiples at the higher end or above this range.

How to value a service industry business?

Calculate normalized EBITDA (or SDE for smaller businesses), then apply an industry-specific multiple drawn from comparable private transactions. The EBITDA multiple method is the fastest and most widely accepted approach among brokers and M&A advisors.

How do you value a business based on cash flow?

Cash flow-based valuation uses either the EBITDA multiple method or a discounted cash flow (DCF) analysis. For privately held service companies, EBITDA multiples are more common — they're simpler and align with how most buyers think about price.

Is a business worth 3 times profit?

Not always. Well-run, specialized, or recurring-revenue businesses often achieve 5x–8x EBITDA, and larger businesses with institutional management can exceed 10x in high-demand sectors. The 3x figure applies mainly to smaller or lower-margin businesses — it's a floor, not a standard.

Can you get ABV without CPA?

The ABV credential is issued by the AICPA and requires a CPA license. Business owners seeking professional valuations can instead work with certified business intermediaries (CBIs), M&A advisors, or ASA-accredited appraisers — none of whom need a CPA designation.