Introduction

Most brokerage owners don't know what their firm is worth until they're ready to sell—and by then, it's often too late to fix what's dragging down the number. Whether you run a real estate, financial, or insurance brokerage, your firm's value is determined by intangibles: your people, client relationships, deal pipeline, and reputation. Unlike manufacturing or retail, there's no equipment or inventory to anchor the price.

This guide is for brokerage owners approaching retirement, planning an exit, or simply wanting to understand where they stand. What a buyer is actually paying for is revenue continuity—the confidence that clients stay, agents remain, and deal flow doesn't disappear the day you walk out.

This article walks through how brokerage valuations work, the methods used, the specific value drivers that matter most, and the common mistakes owners make that cost them money at closing.

Key Takeaways

- Brokerage businesses are valued using EBITDA multiples (typically 4–6x for small firms), revenue/GCI multiples, or a combination

- Value is heavily tied to intangibles: pipeline health, agent retention, client relationships, and revenue diversity

- Key risks that suppress valuation include high key-person dependency, cancellable contracts, and revenue concentration in a single agent or client

- A formal valuation sets a defensible price that holds up to buyer scrutiny and SBA lender review — without one, deals fall apart at due diligence

- An experienced business broker identifies value gaps early, so you enter the market with realistic expectations and a stronger negotiating position

What Makes Valuing a Brokerage Business Different

Unlike manufacturing or retail businesses—where inventory, equipment, and physical assets anchor value—a brokerage's worth lives primarily in intangibles: its people, deal pipeline, client relationships, and reputation. Up to 70–80% of a brokerage's enterprise value walks out the door every night, making human capital the single most important asset on the balance sheet.

Brokerage Firm vs. Producer's Book of Business

Valuing a brokerage firm and valuing an individual producer's book of business are two distinct exercises — and conflating them is one of the most common pricing errors in negotiations:

- A brokerage firm's value rests on institutional strength: management depth, transferable systems, and brand relationships that survive personnel changes

- A producer's book of business is valued on personal client loyalty and how portable those relationships are without the original producer

Buyers and sellers who miss this distinction often end up arguing over fundamentally different things.

Market Sensitivity

Brokerage valuations swing harder with market cycles than most business types. Interest rate environments directly compress mortgage broker revenues, while commercial real estate downturns drain transaction-based firms. Between 2022 and 2023, M&A multiples compressed by 40–60% across most sectors as the Federal Reserve raised rates from 0% to 5.25–5.50%. Buyers price this cyclical risk directly into offers — which means sellers who prepare during favorable conditions capture meaningfully higher valuations than those who wait.

Key Valuation Methods Used for Brokerage Businesses

Brokerage businesses are typically valued using one or more of three core methods—earnings-based, revenue-based, and asset-based. Which method applies depends on the firm's size, how stable its revenue is, and whether the buyer is a strategic acquirer or a financial one.

EBITDA Multiple (Earnings-Based Valuation)

The EBITDA multiple method calculates value by multiplying a firm's normalized EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) by an industry-relevant multiple. Small-to-mid-size brokerages typically transact at 4–6x normalized EBITDA, though multiples vary based on market conditions and firm quality.

Higher multiples are earned by firms with:

- Strong profit margins (20%+ EBITDA margin)

- Diverse revenue streams across multiple clients and agents

- Retained teams with long-term contracts

- Documented operational systems

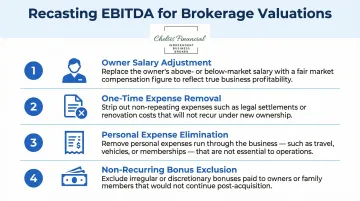

What "Normalized" EBITDA Means:

Normalized EBITDA strips out one-time expenses, owner perks, and non-recurring income to show buyers what the business earns — and a broker or appraiser must recast the financials rather than use raw tax returns.

Common adjustments include:

- Adding back owner salary above market rate

- Removing one-time legal settlements or equipment purchases

- Adjusting for personal expenses run through the business

- Eliminating non-recurring bonuses or consulting fees

Revenue/GCI Multiple

Gross Commission Income (GCI) is the total commission revenue the brokerage generates. It's often preferred over raw revenue because it isolates the firm's actual fee-generating activity, excluding pass-through costs.

Typical GCI/Revenue Multiples:

Most real estate brokerages trade at 0.5x–2x GCI, with stabilized, higher-margin firms commanding the upper range. Revenue multiples are often used alongside EBITDA multiples as a cross-check, especially when EBITDA is temporarily depressed, for example when a firm has recently invested in growth hires or technology infrastructure.

When Revenue Multiples Are Most Useful:

- Startups or high-growth firms with negative or low EBITDA

- Firms making significant reinvestment in people or systems

- Businesses with volatile earnings but stable revenue

Asset-Based and Hybrid Approaches

When neither earnings nor revenue tells the full story, asset-based valuation steps in. It's typically a floor: it captures tangible assets minus liabilities and is most relevant for brokerages being wound down or those with significant owned real estate or technology IP.

When a Hybrid Model Is Appropriate:

A hybrid model (blending asset value and earnings multiple) is appropriate when:

- The brokerage owns valuable real estate or proprietary technology

- The firm is marginally profitable but holds significant hard assets

- Buyers are acquiring primarily for the asset base, not the ongoing operations

Brokerage-Specific Value Drivers That Determine Your Price

Buyers don't just look at revenue — they evaluate operational and qualitative factors that directly shape the multiple they're willing to pay. The owners who understand these drivers before going to market consistently walk away with better terms.

Pipeline Health

A strong, documented deal pipeline is often cited as the single most important value driver for a brokerage because it assures buyers of near-term revenue continuity. Buyers will scrutinize:

- Pipeline size (number of deals and total potential GCI)

- Maturity of deals (how many are in late stages vs. early prospecting)

- Dependency on one or two individuals

Red Flag: If 60% of the pipeline is tied to the owner or one producer, buyers will discount heavily or structure earnouts to mitigate risk.

Agent and Broker Retention

High agent retention rates and agent productivity (measured by GCI per agent) indicate stable management and a retention-friendly culture — both of which lower buyer risk. If key associates leave within six months post-acquisition, revenue can decline 20–30% within twelve months.

What Buyers Look For:

- Agent turnover rate below 15% annually

- Long-term contracts or non-compete agreements with top producers

- GCI per agent above industry benchmarks

- Documented agent satisfaction and engagement metrics

Brokerages where top producers have no long-term agreements typically see valuation multiples discounted 0.5–1.0x compared to firms with retention contracts in place.

Client Retention and Revenue Diversity

Buyers assess the stability of client relationships and the spread of revenue across clients. A single client exceeding 20–25% of total revenue routinely triggers 15–30% valuation discounts, heavier earnout structures, or outright deal collapse during due diligence.

Concentration Thresholds:

- Under 10%: Clean and healthy—no discount applied

- 10–20%: Caution—manageable but prompts scrutiny

- 20–25%: High risk—triggers valuation compression

- Above 30%: Red flag—many buyers will pass entirely

A brokerage where 60% of GCI comes from one client or one agent sells at a steep discount versus one with diverse, recurring relationships.

Multi-Year Financial Trends

Concentration risk becomes most visible when viewed across time — which is why buyers want at least 3–5 years of revenue and profit history to assess trajectory. A firm with consistent year-over-year GCI growth, improving margins, and stable net income will command a meaningfully higher multiple than one with flat or volatile performance.

What Buyers Analyze:

- Compound annual growth rate (CAGR) in GCI

- EBITDA margin trends (expanding vs. contracting)

- Revenue stability through market cycles

- Seasonal patterns and predictability

Operational Systems and Transferability

Firms with documented processes, CRM systems, compliance infrastructure, and management depth beyond the owner are easier to transfer—and buyers pay a premium for businesses that don't collapse the moment the founder walks out the door.

Signs of a Transferable Business:

- CRM with complete client and pipeline data

- Documented SOPs for onboarding, compliance, and service delivery

- Management team capable of running day-to-day operations

- Financial systems producing accurate, timely reports

Key Risks That Can Reduce Your Brokerage's Value

Key-Person Dependency

When the majority of client relationships, deals, or agent loyalty is tied to the owner personally, buyers perceive high post-acquisition risk. When buyers identify severe key-person dependency during due diligence, they typically discount the deal valuation by 30–40% to price in the assumption that the key person will leave and revenue will drop.

Mitigation Strategies:

- Transition agreements (owner stays 12–24 months post-sale)

- Earnouts tied to revenue retention and client transition

- Staff retention bonuses for key producers

- Client relationship transfer protocols

Reducing this dependency before going to market is one of the highest-ROI steps a seller can take — buyers pay more when they see a business that runs without the owner at the center of every deal.

Contract structure is another area that gets scrutinized just as closely.

Cancellable or Short-Term Contracts

Management contracts, client agreements, or agent arrangements that can be cancelled on short notice are a major valuation red flag. Buyers will discount or exclude this revenue from their calculations entirely.

Buyers specifically look for:

- Multi-year client agreements with automatic renewals

- Agent contracts with 90-day or longer notice periods

- Management agreements with change-of-control protections

- Non-compete and non-solicitation clauses

Securing longer-term agreements 12–18 months before going to market can add 15–25% to your final sale price.

Beyond contracts, the composition of your revenue itself shapes how buyers assess risk.

Market Cycle Exposure

Brokerages whose income is heavily correlated with market volume — transaction-fee-dependent mortgage brokerages are a clear example in a high-rate environment — face valuation compression during downturns. Public insurance brokers with 80%+ recurring revenue command premium 16–18x EV/EBITDA multiples, while highly transactional real estate brokerages typically trade at 3x–8x EBITDA.

Revenue Diversification Strategies:

- Add advisory or consulting retainers

- Offer property management or recurring services

- Develop subscription-based technology or data products

- Build ancillary service lines (title, escrow, insurance)

Even a modest shift — moving from 20% to 40% recurring revenue — can push your valuation into a meaningfully higher multiple range when buyers run their models.

How to Get a Professional Valuation for Your Brokerage

Two Primary Valuation Paths

Broker-Authored Opinion of Value

- Faster and lower cost

- Suitable for initial planning and smaller transactions

- Based on comparable sales and market multiples

- Typically completed in 2–3 weeks

Third-Party Credentialed Appraisal

- More rigorous and defensible

- Required for SBA-backed deals over $250,000

- Harder for buyers to challenge

- Prepared by credentialed professionals (ABV, CVA, CBA, ASA)

- Takes 4–6 weeks depending on documentation readiness

Under SBA SOP 50 10 8, an independent business valuation from a "Qualified Source" (ASA, CBA, ABV, CVA, BCA) is mandatory if the financed amount (minus appraised real estate/equipment) exceeds $250,000.

Core Information to Prepare

Before a valuation engagement, prepare:

- 3–5 years of financial statements (P&L, balance sheet, cash flow)

- Recast EBITDA schedules showing normalizing adjustments

- Agent/producer contracts and commission structures

- Client retention data and revenue concentration analysis

- Pipeline documentation (size, maturity, ownership)

- Existing agreements with key staff

- CRM data and operational documentation

The quality and completeness of this documentation directly affects both valuation accuracy and buyer confidence. Well-prepared firms transact 30–40% faster than those scrambling to assemble records during due diligence.

Once your documentation is in order, the logical next step is a professional assessment to put a number on what you've built.

Chelsis Financial's Complimentary Assessment of Value

Chelsis Financial offers a complimentary Assessment of Value for brokerage owners — a no-cost, confidential starting point that reviews your financial performance, market positioning, and operational strengths to establish a defensible valuation range. Contact Chelsis Financial at 866-842-5151 or schedule a confidential consultation to get started.

Frequently Asked Questions

How do business brokers value a brokerage or mortgage broker business?

Brokerage businesses are typically valued using EBITDA multiples (often 4–6x for small firms), GCI/revenue multiples (0.5x–2x), or a combination of both. Valuation emphasizes intangible drivers like pipeline strength, agent retention, and client relationship stability more heavily than hard assets.

How do business brokers value a business based on annual sales?

When using a revenue multiple approach, brokers apply a multiplier (typically 0.5x–2x for brokerages) to annual gross revenue or GCI. The actual multiple is influenced by profit margins, revenue consistency, growth trajectory, and the quality of client relationships.

Can you get ABV without a CPA?

No. The ABV credential is issued by the AICPA exclusively to CPAs. Non-CPAs can pursue alternative designations — CVA, CBA, or ASA — that are accepted for SBA-lending purposes and carry equivalent standing with most buyers and lenders.

What is a typical EBITDA multiple for a brokerage business?

Small-to-mid-size brokerages typically transact at 4–6x normalized EBITDA. Multiples vary based on market conditions, revenue diversity, firm size, and the strength of the management team and agent base. High-quality firms with recurring revenue and strong retention can command 7x or higher.

What factors most reduce the value of a brokerage when selling?

Several concentration risks routinely suppress brokerage sale prices by 30–50%:

- Key-person dependency, where value is tied to a single individual

- Cancellable or short-term client and agent contracts

- Revenue concentrated in one client or top producer

- Flat or declining GCI trends heading into the sale

How long does the brokerage valuation and sale process typically take?

A professional valuation typically takes 2–6 weeks depending on documentation readiness. The full sale process — from valuation through closing — ranges from 6 to 18 months, though well-prepared firms with clean financials and documented systems often close in 9–12 months.