Many food manufacturing owners underestimate how complex the sale process becomes once a buyer's advisors get involved. Financials get stress-tested. Batch records get reviewed. FDA registrations get checked. And if any of it doesn't hold up, deals stall or reprice — sometimes dramatically.

This guide walks through the full process: how to value your business, what preparation actually moves the needle, how to structure the sale, find the right buyer, and navigate from LOI to closing without leaving money on the table.

Key Takeaways

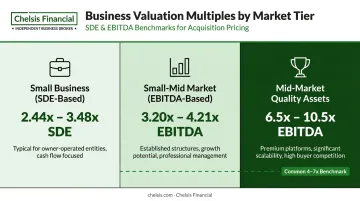

- Food manufacturing businesses are typically valued at 2.44–4.21x EBITDA (smaller operations) up to 6.5–10.5x for high-quality ones

- Certifications, brand equity, and customer diversification are the primary value levers

- Preparation starting 12–24 months before going to market is the single biggest driver of final price

- Buyers almost always prefer asset sales; sellers often prefer stock sales — the structure has major tax implications for both parties

- NDAs come before any financial disclosure; a blind profile protects your identity during early-stage marketing

- A broker with a vetted buyer registry keeps the process confidential while reaching qualified acquirers

How to Value a Food Manufacturing Business

SDE vs. EBITDA: Which Method Applies to You

The method used to value your business depends primarily on deal size, not revenue. According to the IBBA/M&A Source Market Pulse Q2 2025, transactions under $2M are generally valued using Seller's Discretionary Earnings (SDE), while deals in the $2M–$50M range typically use EBITDA multiples.

- SDE adds back owner salary, benefits, and one-time expenses to net income — best for owner-operated businesses where the owner is deeply involved in daily operations

- EBITDA reflects earnings before interest, taxes, depreciation, and amortization — preferred for businesses with professional management and more institutional buyers

What Multiples Actually Look Like

Valuation ranges vary significantly by business quality and size. Peak Business Valuation data for food manufacturing businesses shows:

| Business Size | Typical Multiple |

|---|---|

| Small (SDE-based) | 2.44x – 3.48x SDE |

| Small-Mid (EBITDA-based) | 3.20x – 4.21x EBITDA |

| Mid-Market quality assets | 6.5x – 10.5x EBITDA |

The 4–7x EBITDA range commonly cited across food M&A works as a starting benchmark, but quality businesses with strong brands and clean documentation consistently exceed it.

What Pushes Your Multiple Up or Down

Value drivers that move you toward the top of the range:

- Proprietary recipes or formulations backed by documented bills of materials

- Retail shelf presence or a loyal consumer following with measurable brand equity

- Third-party certifications: organic, kosher, non-GMO, SQF, BRCGS, HACCP

- Long-term distribution contracts with retail or foodservice accounts

- Production systems that run without depending on one person to operate

Value detractors that compress your multiple:

- Owner-dependency in production or key customer relationships

- High customer concentration — one retailer driving a large share of revenue is a common deal killer

- Aging equipment or a poorly maintained facility

- Inconsistent batch records or gaps in food safety documentation

Knowing where you stand on these factors before going to market changes your negotiating position entirely. Chelsis Financial offers a Complimentary Assessment of Value covering financial performance, market benchmarks, and tangible asset estimates. Schedule a confidential call at calendly.com/chelsis/getanswers.

Preparing Your Business for Sale

Start 12–24 months before you plan to go to market. That runway gives you time to fix what buyers will find anyway, rather than having those discoveries reprice your deal mid-negotiation.

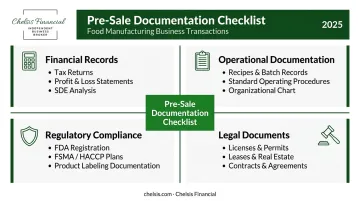

Financial Documentation

Buyers and their advisors will expect clean, complete financials going back three to five years. At minimum, assemble:

- Three to five years of federal tax returns

- Profit & loss statements, balance sheets, and cash flow statements

- A seller's discretionary earnings (SDE) analysis with documented add-backs

- Clear explanations for any anomalies, owner perks, or one-time expenses

Unaudited or inconsistently prepared financials are one of the most common reasons deals stall. If your books are on a desktop-only accounting system, migrate to cloud-based software before going to market — it speeds up buyer review.

Operational Documentation

A buyer is acquiring a business, not just a building and equipment. They need confidence the operation will run without you. Document:

- Formalized recipes and bills of materials

- Batch manufacturing records and production SOPs

- Supplier and distributor contact lists with contract terms

- Employee org chart with roles, tenure, and compensation

- Quality control procedures and inspection logs

Regulatory Compliance

This area derails more food manufacturing deals than any other. Buyers' advisors will check:

- FDA food facility registration — must be current; under 21 CFR § 1.234, registration updates are due within 60 calendar days of changes, and a change of ownership requires the former owner to cancel and the new owner to register separately

- FSMA/HACCP plans — current preventive controls documentation under FDA Part 117

- Labeling compliance — all product labels must meet current FDA requirements

- FSIS inspection (if applicable) — meat, poultry, and egg product facilities require a new application for any change of ownership

Gaps here don't just slow due diligence. They give buyers leverage to reprice or walk away entirely.

Facility, Equipment, and Team Readiness

Think of preparing your facility the way you'd stage a home before listing it. A buyer's first walkthrough creates an impression that's hard to undo. Service equipment, address deferred maintenance, and make the production floor clean and audit-ready.

On the people side, identify your key production staff, quality control personnel, and any customer-facing employees. Buyers place real value on a stable, experienced team. Retention incentives or employment agreements — even informal ones — can reassure buyers worried about key people leaving after close.

Choosing Your Sale Structure: Stock Sale vs. Asset Sale

How the deal is structured has a larger impact on your net proceeds than most sellers expect. Get both a CPA and a transaction attorney involved before negotiations begin.

Stock Sale

The buyer acquires the legal entity — all assets and liabilities transfer with it. For sellers, this typically means:

- Lower capital gains tax treatment (long-term capital gains rates rather than ordinary income on certain asset classes)

- Less administrative complexity — no need to reassign individual contracts or licenses

- The risk: the buyer inherits unknown liabilities, which is why many buyers resist this structure

Asset Sale

The buyer selects specific assets to acquire — equipment, inventory, recipes, brand, customer lists, contracts — without taking on the business entity or its existing liabilities. For buyers, this is usually the preferred structure because:

- They get a stepped-up tax basis on acquired assets

- They can exclude liabilities and unwanted assets

- IRS Form 8594 governs the allocation of purchase price across asset classes

FDA facility registration is not transferable in either structure. The former owner cancels their registration and the new owner files a fresh one — this applies regardless of how the deal is structured.

Most food manufacturing buyers push for asset sales. Sellers tend to prefer stock sales because of the more favorable capital gains treatment. That gap is negotiable. With the right advisors modeling both scenarios, you can see precisely what each structure means for your actual take-home proceeds.

Finding the Right Buyer and Keeping the Sale Confidential

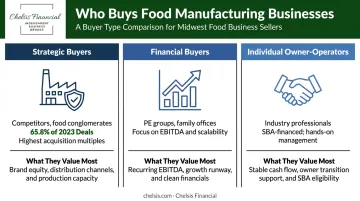

Who Buys Food Manufacturing Businesses

Three main buyer types are active in this market:

- Strategic buyers — competitors, food conglomerates, or complementary brands seeking production capacity, SKUs, or distribution reach. Capstone Partners data shows strategic buyers accounted for 65.8% of food-sector deals in 2023. They typically pay the highest multiples because they can capture synergies.

- Financial buyers — private equity groups, family offices, and PE add-on platforms. They focus on EBITDA margins, scalability, and management depth.

- Individual owner-operators — often industry professionals or experienced managers looking to acquire a business rather than start one. More common at smaller transaction values and frequently SBA-financed.

Each type comes to the table with different priorities. Strategics value your brand and distribution footprint; PE firms want EBITDA and a scalable model; individual operators want something they can step into and run.

Confidentiality Protocols

Premature disclosure is a real risk in food manufacturing. Employees get nervous. Suppliers start hedging. Competitors use the information. The standard protocol:

- Market the business using a blind profile — a teaser document that describes the business (geography, revenue, EBITDA, industry) without identifying it

- Require a signed NDA before disclosing any financial or operational detail

- Share the full Confidential Information Memorandum only after NDA execution and initial buyer qualification

Chelsis Financial maintains a registry of vetted, qualified buyers, which means sellers aren't fielding inquiries from unqualified prospects. NDA execution happens before any identifying information is shared — keeping the process confidential from first contact through closing.

Navigating Negotiations, Due Diligence, and Closing

The Letter of Intent

The LOI sets the framework for the deal: proposed price, payment structure (cash at close, seller financing, earnout), exclusivity period, and the seller's expected post-close involvement. It is non-binding on deal economics but typically binding on exclusivity and confidentiality.

A few things sellers commonly overlook:

- Earnout terms and milestones deserve as much scrutiny as the headline number

- Seller financing terms — amount, rate, and security — are negotiable

- The due diligence period length is negotiable; shorter windows are achievable if your documentation is organized

You have maximum leverage before signing the LOI. Don't accept the first offer without counter-negotiating on structure, not just price.

Food Manufacturing Due Diligence

Once the LOI is signed, the buyer's team goes to work. Beyond standard financials, food manufacturing buyers specifically examine:

- Batch manufacturing records and production consistency

- Food safety documentation and FDA/FSIS inspection history

- Supplier contract assignability — can key supplier relationships transfer?

- Customer contract transferability — do contracts have successor clauses?

- Equipment condition reports and maintenance records

- Food safety culture and FSQA management practices

Sellers who prepared 12–24 months before going to market move through this phase in weeks. Those who didn't can expect buyers to drag out diligence while building a case for a price reduction.

Purchase and Sale Agreement

With diligence complete, the parties move to the definitive agreement — which should closely mirror the LOI. Key negotiation points at this stage:

- Representations and warranties — what the seller certifies as true about the business

- Indemnification clauses — who bears liability if post-close issues surface

- Non-compete agreements — geographic scope, duration, and industry restrictions

Sellers without experienced legal counsel at this stage regularly sign representations and warranties that create years of post-closing liability exposure. Get a transaction attorney — not just a general business lawyer.

The Transition Period

Most food manufacturing sales include a 30–90 day seller-assisted transition, with complex businesses sometimes running up to 6–12 months. During this period, the seller typically:

- Introduces the buyer to key suppliers and customers

- Trains the new owner in production processes and quality procedures

- Supports key staff in adapting to new ownership

If your deal includes an earnout, a smooth transition directly protects that payment. It also protects your reputation with the suppliers, customers, and employees you've built relationships with over years.

Even well-structured deals can collapse late in the process. Most failures are preventable — but only if you address the issues before they surface in diligence.

Common Deal Killers (and How to Address Them)

| Risk | Prevention |

|---|---|

| Undisclosed compliance gaps | Conduct a pre-sale regulatory audit; disclose issues before the LOI |

| Financial records that don't reconcile | Clean up books 12–24 months before going to market |

| Key employees signaling they'll leave | Retention agreements or incentive packages before going to market |

| Customer concentration that surfaces in due diligence | Diversify accounts before selling, or price it into your expectations upfront |

| Unreconciled trade-spend or SKU complexity | Clean up accounting and reduce SKU count before the sale |

Frequently Asked Questions

How do you value a food manufacturing business?

Food manufacturing businesses are most commonly valued using EBITDA or SDE multiples. Smaller owner-operated businesses (under $2M transaction value) typically use SDE multiples, while larger operations use EBITDA — generally ranging from 3x to 10x+ depending on profitability, brand strength, certifications, and customer base diversification.

How long does it take to sell a food manufacturing business?

The active sale process — from engaging a broker to closing — typically takes 6–9 months, based on IBBA/M&A Source Market Pulse data. Add 12–24 months of pre-sale preparation before that, and owners should plan on a total timeline of 18–36 months from decision to close.

What documents do I need to sell my food manufacturing business?

Expect to gather documents across four categories:

- Financial records: Tax returns, P&Ls, and balance sheets (3–5 years)

- Operational documentation: Recipes, SOPs, and batch records

- Regulatory compliance: FDA registration, FSMA/HACCP plans, and labeling files

- Legal documents: Business licenses, leases, and supplier/customer contracts

Should I use a business broker to sell my food manufacturing business?

A broker with food manufacturing experience adds real value: access to qualified buyers, confidential marketing, negotiation support, and transaction management. Given the regulatory complexity and confidentiality requirements in food manufacturing, choosing the right broker matters more here than in most industries.

What is the difference between a stock sale and an asset sale?

In a stock sale, the buyer acquires the entire legal entity — liabilities included. In an asset sale, the buyer selects specific assets without inheriting the business entity. Buyers typically prefer asset sales for tax step-up and liability protection; sellers often favor stock sales for better tax treatment. Both parties should model the implications with their CPA before settling on structure.

How do I find buyers for my food manufacturing business?

Buyers include strategic acquirers (food companies, competitors), private equity groups, and individual owner-operators. Working with a business broker like Chelsis Financial, which maintains a vetted buyer registry, is typically the most effective approach — qualified prospects are screened before any sensitive information changes hands.