Introduction

Selling a manufacturing business is one of the most significant financial decisions an owner will ever make. Unlike service or digital businesses, manufacturing operations involve complex asset valuations, equipment appraisals, supply chain considerations, and regulatory requirements that don't have simple answers.

Most owners reach this point asking the same two questions: What is my business actually worth? And how do I sell without destroying what I spent years building?

The stakes are genuinely high. Over 52% of U.S. employer-businesses are now owned by individuals aged 55 and older, yet 90% of recent sellers are first-timers without formal exit strategies. Poor preparation, emotional pricing, or inadequate planning can cost manufacturing business owners hundreds of thousands of dollars—or cause deals to collapse entirely during due diligence.

This guide is written for small to mid-size manufacturing business owners in the Midwest who are actively planning an exit. Inside, you'll find a practical walkthrough of how buyers value manufacturing companies, how to prepare your operations and financials for sale, and how to structure a deal that protects what you've built—whether you run a metal fabrication shop, a food production facility, or an industrial equipment operation.

Key Takeaways

- Manufacturing businesses are valued using SDE multiples (3.0x–4.2x) or EBITDA multiples (3.0x–10.9x) based on size and specialization

- Pre-sale preparation—including financial documentation, reduced owner dependency, and customer diversification—directly increases final sale price

- Customer concentration above 20-25% triggers significant buyer concern and valuation discounts

- The full sale process—from valuation through closing—typically takes 6-12 months

- An experienced business broker improves outcomes by reaching qualified buyers while keeping the sale confidential

What Makes a Manufacturing Business Valuable?

Core Value Drivers Unique to Manufacturing

Manufacturing businesses possess tangible assets and operational characteristics that distinguish them from service or digital companies. Buyers prioritize these specific value drivers:

- Supply chain depth: Long-standing supplier agreements and negotiated pricing take years to build — buyers pay for that continuity, especially in industries facing material volatility.

- Workforce expertise: Employees trained in proprietary processes or specialized equipment provide immediate production capability. High retention rates signal stability and reduce post-acquisition risk.

- IP and certifications: Patents, custom tooling, and proprietary processes create defensible advantages that justify higher multiples. Businesses with ISO or AS9100 credentials consistently achieve stronger valuations.

- Physical assets: Owned facilities and modern equipment reduce buyer capital requirements. Operations needing immediate reinvestment trade at a discount.

Revenue Consistency and Customer Concentration

Revenue quality matters as much as revenue size. Two factors drive most of the scrutiny:

Recurring contracts and purchase orders give buyers the ability to model future cash flow and service acquisition debt with confidence. Multi-year agreements or subscription-based arrangements directly support higher valuations.

Customer diversification is where many manufacturing businesses lose value. Concentration above 20-25% typically produces a 1.0x multiple discount. A single customer at 40%+ of revenue creates a "revenue cliff" that many buyers — and nearly all lenders — won't accept. SBA lenders explicitly flag concentration above 20% as a financing concern, which limits the buyer pool significantly. Businesses with no single customer exceeding 15% of revenue face fewer obstacles and command stronger offers.

The Owner Dependency Problem

When the owner is the primary customer contact, technical expert, and operational decision-maker, buyers see a business that stops running the day the owner leaves. During due diligence, buyers routinely interview managers without the owner in the room — specifically to test whether the business can stand on its own.

Sellers who reduce this dependency before going to market consistently command higher multiples. That means building a professional management layer, documenting processes, and transitioning customer relationships to staff. Owners who take these steps two to five years before sale give buyers a business they can actually operate — which is precisely what supports a competitive acquisition process and a stronger final price.

How to Value a Manufacturing Business

SDE vs. EBITDA: Choosing the Right Framework

Manufacturing business valuations use one of two primary frameworks depending on size and structure:

Seller's Discretionary Earnings (SDE)

SDE is used for smaller, owner-operated manufacturing businesses typically under $2 million in revenue. SDE represents the total financial benefit to a single owner-operator, including salary, benefits, and discretionary expenses. For businesses valued at $1M-$2M, average SDE multiples are 3.15x.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization)

EBITDA is used for larger manufacturing operations with professional management teams. Businesses in the $5M-$10M enterprise value range achieve average EBITDA multiples of 4.60x, while larger operations command higher multiples as they attract institutional buyers.

Understanding Earnings Multiples

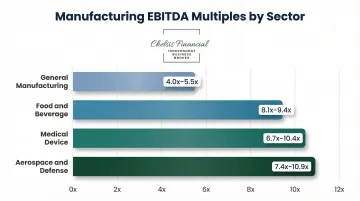

Manufacturing businesses generally trade at 3-4x SDE or 3-5x EBITDA as broad averages, but specific sub-categories vary significantly:

General Manufacturing: 4.0x-5.5x EBITDA

Aerospace & Defense: 7.4x-10.9x EBITDA depending on size

Medical Device: 6.7x-10.4x EBITDA

Food & Beverage: 8.1x-9.4x EBITDA

Specialized manufacturers with certifications, proprietary technology, or long-term contracts command significant multiple expansion compared to generalist machine shops.

Factors That Determine Your Multiple

Where your business falls within the valuation range depends on several critical factors:

- Revenue and earnings trends: Growing businesses command premium multiples; declining operations face discounts

- Customer concentration: High concentration (>25% from one customer) typically results in 1.0x multiple reduction

- Owner dependency: Businesses requiring owner involvement daily face valuation suppression

- Capital expenditure needs: Deferred maintenance or aging equipment is deducted dollar-for-dollar from enterprise value

- Employee retention: High turnover or key employee risks reduce buyer confidence

- Intellectual property: Patents, trademarks, or proprietary processes justify higher valuations

The Cash Flow Reality Check

Valuation multiples mean nothing if the business cannot support acquisition financing. The sale price must enable the buyer to:

- Service acquisition debt payments without straining operating cash flow

- Pay themselves a reasonable salary in line with market rates for their role

- Generate an acceptable return on the equity they invested at closing

Buyers and their lenders run detailed cash flow models before committing. A price that looks reasonable on a multiple basis can still kill a deal if the numbers don't support the debt load.

Professional Valuation: The Critical First Step

Sellers should obtain a professional opinion of value before going to market. Owners who price based on gut feel or what a neighbor got for their business routinely misprice — in either direction.

Chelsis Financial's Complimentary Assessment of Value gives manufacturing owners a grounded starting point. It reviews three years of financials, analyzes cash flow quality, evaluates tangible assets, and benchmarks against current market conditions to build a defensible asking price.

Preparing Your Manufacturing Business for Sale

The 12-24 Month Preparation Timeline

Sellers who begin preparing 12-24 months before listing consistently attract more buyers, close faster, and command higher multiples than those who rush to market. This preparation window allows owners to:

- Build or strengthen management teams

- Document operational processes and procedures

- Address deferred maintenance and capital needs

- Improve financial documentation and controls

- Diversify customer relationships where possible

- Reduce owner dependency through delegation

One Wisconsin commercial millwork manufacturer began preparation five years before the owner's desired exit at age 65. During this period, the owner brought in professional management and transitioned to an absentee role. When the business went to market, the competitive process attracted multiple qualified buyers, ultimately resulting in acquisition by a middle-market private equity fund—directly attributed to the owner's advance planning.

That kind of outcome starts with documentation. Of all the preparation steps, financial records carry the most weight with buyers and their advisors.

Financial Documentation

Buyers and their advisors require comprehensive financial documentation:

- Minimum 3 years of profit-and-loss statements

- Cash flow statements and balance sheets

- Tax returns for corresponding periods

- Asset schedules with current valuations

- Clear calculations of discretionary earnings

Financial documents must be presented in clean, organized, standardized formats. Messy or inconsistent financials create buyer doubt and invite price reductions during due diligence. The most common reason deals stall or fail is incomplete or disorganized financial information.

Net Working Capital Management

Net working capital (NWC)—current assets (inventory, accounts receivable, prepaid expenses) minus current liabilities (trade payables, accrued wages)—represents the capital required to operate the business day-to-day.

Buyers typically establish an NWC target based on a 12-18 month average. Sellers who manage NWC down to the lowest functional level before listing retain more value at close. Excess inventory, inflated receivables, or unnecessarily high working capital requirements all reduce proceeds at closing.

Operational Readiness

Manufacturing buyers scrutinize operations closely—and visible problems become negotiating leverage. Address these issues before listing:

- Deferred facility maintenance: Buyers price in risk for visible maintenance issues

- Process documentation: Document standard operating procedures, quality control processes, and production workflows

- Operational inefficiencies: Identify and address bottlenecks, waste, or process gaps

Well-run, well-documented operations signal lower transition risk and support higher multiples. Fixing identifiable problems before going to market is almost always cheaper than accepting a reduced offer later.

The Sale Process: From Listing to Closing

Working with a Business Broker

Business brokers provide critical services throughout the sale process:

- Conduct or validate professional valuations

- Prepare confidential information memoranda

- Identify and vet qualified buyers

- Negotiate on the seller's behalf

- Manage the process through closing

Selling independently risks poor pricing, confidentiality breaches, and drawn-out timelines. For most manufacturing business owners, working with a qualified broker significantly improves both the final sale price and the likelihood of a successful close.

Chelsis Financial works with manufacturing sellers across the Midwest — including metal fabrication, healthcare equipment, and aerospace machining businesses — managing the process from initial valuation through closing.

Confidentiality and Marketing

Confidentiality is particularly critical in manufacturing sales. Employees, suppliers, customers, and competitors may react negatively if a sale becomes known prematurely.

Protecting Confidentiality:

- Brokers use non-disclosure agreements (NDAs) before sharing sensitive information

- Blind teasers market the opportunity without revealing the business's identity

- Qualified buyers are screened for financial capacity and legitimate interest before detailed disclosure

The Confidential Information Memorandum (CIM) provides a comprehensive overview of the business — covering operations, financials, growth opportunities, and assets — and serves as the primary marketing document for serious buyers.

Buyer Types:

- Private equity firms: Seek add-on acquisitions to existing portfolio companies

- Strategic/trade buyers: Competitors or adjacent businesses seeking expansion

- Individual owner-operators: Experienced manufacturing professionals seeking ownership

Each buyer type evaluates manufacturing businesses with different priorities, and effective marketing addresses the specific concerns of each category.

Negotiation, Due Diligence, and Closing

Letter of Intent (LOI)

The LOI establishes proposed price and key terms. Once accepted, it triggers the due diligence period during which the buyer verifies all material information.

Due Diligence

Due diligence for lower-middle-market manufacturing deals now averages 5.5 months, with the total time from engagement to close reaching 11 months. The seller's responsibility during due diligence is transparency and cooperation — disputes or surprises at this stage frequently derail transactions or force price concessions.

Purchase Agreement and Closing

The purchase agreement is the legally binding contract governing the transaction. Buyers confirm financing through SBA loans, bank financing, seller financing, or all-cash structures. Manufacturing sales often carry additional legal and environmental disclosure requirements that sellers should prepare for with appropriate legal counsel.

Common Mistakes Manufacturing Business Sellers Make

Overpricing from the Start

Listing too high—often driven by emotional attachment rather than market data—causes the business to stagnate on the market and damages credibility with buyers. Extended time on the market creates operational deterioration as employees worry about job stability, the owner diverts attention from operations, and overall company value declines.

Businesses that sit on the market for extended periods frequently sell for less than if they had been properly priced initially. A neutral, third-party valuation before listing anchors your asking price in reality—and keeps serious buyers at the table.

Neglecting Preparation and Timing

Sellers who wait too long—until retirement is imminent or the business has already begun declining—lose significant leverage. Deteriorating financials, deferred maintenance, and an unprepared management team all reduce value.

The best time to begin planning is 2-3 years before the desired exit. This runway allows owners to address value drivers systematically, build management teams, document processes, and position the business for maximum value.

Ignoring the Transition Plan

Buyers—especially private equity and strategic buyers—heavily discount businesses where the owner is the business. If the business can't run without you for two weeks, most serious buyers will walk.

When buyers perceive high owner dependency, they typically respond in one of three ways:

- Impose earn-out structures that delay the full sale price

- Require seller financing to keep the owner engaged post-close

- Walk away from the deal entirely

Building a management team that operates independently is one of the highest-leverage moves a seller can make before going to market.

Frequently Asked Questions

How to sell a small manufacturing business?

Selling a small manufacturing business follows the same core process—valuation, preparation, marketing, negotiation, and closing—but uses SDE-based valuation rather than EBITDA. Buyers tend to be individual operators or small private equity firms, and a business broker provides the qualified buyer network and guidance to reach them effectively.

How to evaluate a business worth to sell?

Manufacturing businesses are typically valued using SDE or EBITDA multiples that vary by sub-industry. A professional valuation accounts for earnings quality, growth trends, customer concentration, and asset base—not just revenue. The best starting point is a complimentary assessment from an experienced business broker who understands manufacturing sector dynamics.

What is a typical EBITDA multiple for a manufacturing business?

Most manufacturing businesses trade in the 3-5x EBITDA range as a broad average, but specific sub-categories vary significantly. Aerospace and defense manufacturers command 7.4x-10.9x EBITDA, while medical device manufacturers achieve 6.7x-10.4x EBITDA depending on size and specialization. Actual multiples depend on niche, margins, growth profile, and asset intensity.

How long does it take to sell a manufacturing business?

The typical sale process takes 6-12 months from listing to closing. Well-prepared businesses with clean financials and strong broker relationships often close faster, while underprepared businesses or those requiring SBA financing may take longer. Due diligence alone can extend 5-6 months for larger transactions.

Should I use a business broker to sell my manufacturing business?

For most manufacturing business owners, yes. A qualified broker brings buyer networks, valuation expertise, and negotiation experience that most sellers lack on their own—and that combination routinely results in higher sale prices and a greater likelihood of closing successfully.

How do I maintain confidentiality when selling my manufacturing business?

Brokers protect confidentiality through blind teasers that omit the business name, NDAs signed before any details are shared, and a staged disclosure process. Employees, customers, and competitors stay unaware until the seller chooses to announce—keeping operations and morale stable throughout.