Introduction

Every small business will eventually change hands — whether through a planned transition or an unexpected crisis. Yet most owners delay this reality until it's too late. The statistics are sobering: only 8% of business owners have a completed, written succession plan, and 92% of small business exits currently result in closure rather than a successful sale or transfer.

This guide is for small business owners who are beginning to think about how to transition or exit their business. The most important decision you can make is to start early — ideally three to five years before your planned exit. What follows covers the core steps: understanding your options, valuing your business, identifying successors or buyers, and building a plan that protects what you've built.

Key Takeaways

- Business succession planning prepares your company for ownership or leadership transfer when you exit

- Without a plan, unexpected exits destroy value and leave owners financially exposed

- A complete plan covers valuation, named successors, legal structure, and a documented timeline

- Exit paths range from inside transfers (family or employees) to outside sales to third-party buyers

- Starting three to five years early maximizes transition success and business value

What Is Business Succession Planning?

Business succession planning is the process of identifying how ownership and control of your business will be transferred when you exit — whether by choice or circumstance.

Done right, it's a strategic roadmap that answers who takes over, under what terms, and how the value you've built gets protected through the transition.

How It Differs from Internal HR Succession Planning

Many businesses have internal succession plans that focus on filling leadership roles when executives retire or leave. That's HR planning. For small business owners, succession planning is different in a critical way: it's about ownership transfer, business continuity, and maximizing exit value. You're not just replacing a manager; you're transferring the company itself.

That distinction matters most when exits happen without warning. Roughly 50% of all business exits are involuntary, triggered by what advisors call the "Five D's":

The Five D's: Why Unplanned Exits Happen

- Death — Sudden loss of the owner without a named successor

- Disability — Illness or injury that sidelines the owner indefinitely

- Divorce — Asset division that forces a sale or loss of control

- Distress — Financial pressures that make the business unsustainable

- Disagreement — Escalating conflicts between business partners

A formal succession plan addresses all five by establishing legal agreements and documented transfer procedures before any crisis forces your hand.

Why Most Small Businesses Aren't Ready

Despite the looming need, preparation remains alarmingly low. Only 30% of family businesses have a documented succession plan, and the broader small business community fares even worse.

The Real Risks of Having No Plan

Without a succession plan, owners face:

- Rushed or reactive sales that yield 30% to 50% less than market value — especially when the business is heavily dependent on the founder

- Verbal inheritance agreements that collapse into disputes, resentment, and legal battles among family members

- Operational chaos when no successor has been trained to step in

- Unnecessary estate taxes, gift taxes, and capital gains liabilities from poorly structured transfers

Why Owners Delay

Three factors drive procrastination:

- The business is tied to their identity — planning an exit feels like planning irrelevance

- Owners assume they have years left to prepare, until a health scare or sudden burnout forces an immediate decision

- The process feels overwhelming without a clear first step or roadmap

Succession planning is ultimately about protecting what you've built. Owners who start five to ten years before their exit have far more options — on price, structure, and timing — than those who start under pressure.

How to Build Your Business Succession Plan

Succession planning is a multi-year process, not a one-time event. Approach it in structured steps to maintain clarity and momentum.

Step 1: Define Your Goals and Timeline

Start by clarifying what a successful exit looks like for you personally:

- Do you want to retire fully, or stay involved part-time as an advisor?

- Is transferring to a family member or key employee your priority, or do you want the highest sale price?

- What financial outcome do you need to fund retirement, pay off debt, or support your lifestyle?

Your personal goals drive every subsequent decision. Your timeline matters just as much.

A three-to-five-year runway gives you time to increase business value, prepare successors, and structure the deal favorably. A one-year timeline forces compromises that reduce your options and negotiating power.

Step 2: Establish an Objective Business Valuation

You cannot plan an exit without knowing your business's current market value. Valuation determines:

- Whether sale proceeds will fund your retirement

- What a fair transfer price to family members should be

- Whether your business is "sellable" in its current state

The U.S. Small Business Administration recognizes three primary valuation approaches:

- Income Approach — Projects future earnings, then discounts for risk

- Market Approach — Benchmarks your business against comparable recent transactions

- Asset Approach — Values what you own minus what you owe

Valuation metrics vary by business size. "Main Street" businesses (under $2 million in value) are typically priced on Seller's Discretionary Earnings (SDE) multiples, while larger companies use EBITDA.

Median SDE multiples range from 2.0x for businesses under $500K to 3.3x for businesses valued between $1M and $2M. Knowing where your business falls on that spectrum shapes every downstream decision.

Chelsis Financial offers a Complimentary Assessment of Value as a starting point for owners who want to understand what their business is worth before committing to a specific exit path.

Step 3: Identify Successors or Qualified Buyers

Who will take over? The answer depends on your chosen exit path:

For inside transfers:

- Evaluate family members or key employees for readiness, skill gaps, and genuine interest

- Assess whether they have the financial capacity to buy you out

- Determine if they possess the leadership skills to sustain operations

For outside sales:

- Work with a business broker to access a vetted network of qualified buyers

- Identify strategic buyers (competitors or companies in adjacent markets) who may pay a premium

- Consider financial buyers (private equity firms or individual entrepreneurs) seeking acquisition opportunities

Step 4: Address Legal, Tax, and Financial Structures

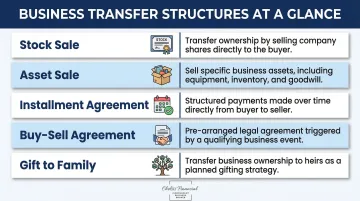

The structure of your business transfer has major tax and legal consequences. Common structures include:

- Stock sale — The buyer acquires your ownership shares and inherits the legal entity

- Asset sale — The buyer picks specific assets; liabilities typically stay with the seller

- Installment agreement — You carry part of the purchase price, paid out over a defined term

- Buy-sell agreement — A pre-negotiated contract that activates on death, disability, or departure

- Gift to family — Ownership passes without a sale, subject to estate and gift tax rules

Each structure impacts capital gains taxes, estate taxes, liability exposure, and net proceeds. Bring in an attorney, CPA, and financial advisor at this stage to optimize the outcome.

Step 5: Document the Plan and Review It Regularly

Once the professional and legal work is in place, get it on paper. A succession plan only has value if it's written down, shared with key stakeholders, and revisited annually. Your documented plan should include:

- Clear exit goals and timeline

- Current business valuation

- Named successors or buyer criteria

- Legal agreements (buy-sell, partnership, transfer documents)

- Tax and estate planning provisions

- Contingency plans for emergency departures

- A scheduled annual review to reflect changes in business value, personal goals, or family circumstances

Your Exit Options: Inside Transfers and Outside Sales

Succession planning offers two broad exit paths: inside transfers and outside sales. The right choice depends on your goals — whether that's maximizing sale price, preserving your legacy, or ensuring the business continues under people you trust.

Inside Transfers

Inside transfers involve passing ownership to someone already connected to the business:

Family succession:

- Requires early preparation and clear role definitions

- Often driven by legacy preservation rather than maximum sale price

- Must address estate planning, gift taxes, and fairness among heirs

- Only 30% of family businesses survive to the second generation, making preparation critical

Management buyouts:

- Give trusted employees ownership and control

- Often structured with seller financing to bridge capital gaps

- Preserve company culture and employee relationships

Employee Stock Ownership Plans (ESOPs):

- Offer a structured way to sell to the workforce

- 6,609 ESOPs operate in the U.S., with workers in ESOPs having 92% higher median household net wealth

- Require at least 15-20 employees to be financially viable due to setup costs

Inside transfers work well when continuity matters most. When your priority shifts to maximizing value or finding a buyer outside your circle, outside sales offer a different set of options.

Outside Sales

Outside sales involve transferring ownership to a third party:

Strategic buyers:

- Competitors or companies in adjacent markets seeking synergies

- Typically pay the highest price due to operational integration value

Financial buyers:

- Private equity firms or investment groups focused on return on investment

- Often retain existing management and provide growth capital

Individual buyers:

- Entrepreneurs seeking acquisition opportunities

- Increasingly common through "search funds" and entrepreneurship-through-acquisition models

Confidentiality is critical during outside sales. Premature disclosure can unsettle employees, alarm customers, and tip off competitors — which is why qualified buyers are vetted before any sensitive details are shared.

Common Mistakes That Derail Succession Plans

Waiting Too Long to Start

The most critical mistake is delaying until burnout or crisis forces action. Advisors strongly recommend beginning succession planning three to five years before a planned transition. At minimum, financial cleanup and operational documentation must begin 12 to 18 months prior to listing. Waiting reduces your options, weakens negotiating leverage, and often leaves significant value on the table.

Vague or Undocumented Plans

Verbal agreements about who will take over, no formal valuation, and no legal structure leave businesses exposed. Without written agreements, the consequences stack up fast:

- Family members may challenge ownership transfers

- Buyers may walk away from unclear deals

- The IRS may reject valuations during estate settlements

Documentation isn't optional — it's the foundation every other part of your plan rests on.

Ignoring the Human Elements

Treating succession as purely a financial transaction is a common failure point. Owners who skip honest conversations with family members or key employees often discover too late that their chosen successor isn't interested — or isn't ready. Talk early about roles, timelines, and what the business actually requires of whoever takes over. That conversation is uncomfortable once. The alternative is a failed transition.

Conclusion

Business succession planning is not a single event but a strategic process that protects the value you've spent years building. The earlier you begin, the more options remain available — and the greater control you retain over the outcome.

Small business owners don't need to navigate this alone. Working with experienced professionals — from financial advisors and attorneys to business brokers like Chelsis Financial — ensures your transition is handled confidentially and on terms that protect your valuation and your legacy.

Whether you're planning a family transfer, a management buyout, or a third-party sale, the structure you put in place now determines what that exit actually looks like. Start the conversation early — while you still have the leverage to shape it.

Frequently Asked Questions

What is a succession plan in business?

A business succession plan is a formal strategy outlining how ownership and leadership transfer when the current owner exits. It covers who takes over, the timeline, and the legal and financial terms governing the transition.

What are the five steps in succession planning?

The core steps are:

- Define your exit goals and timeline

- Establish a business valuation

- Identify successors or buyers

- Structure the legal and financial transfer

- Document and maintain the plan

What should a succession plan include?

A complete plan covers:

- Current business valuation

- Named successors or buyer criteria

- Transition timeline

- Legal agreements (such as buy-sell agreements)

- Tax and estate planning provisions

- Contingency plans for unexpected events

How do I transfer ownership of a business to a family member?

Start with a fair valuation, then choose a transfer structure — gift, sale, or installment agreement. From there, address estate and gift tax implications and ensure the successor has the skills and authority needed to lead.

What is the most common mistake in succession planning?

The most common mistake is waiting too long to start. Delaying limits your options, reduces leverage in negotiations, and often results in a rushed transition that leaves significant value on the table.

What are examples of succession planning?

Common real-world scenarios include:

- A retail owner who trains a longtime manager to buy out the business over five years

- A family-owned manufacturer who transfers ownership to a child through a structured installment sale

- A service business owner who sells to a strategic acquirer through a business broker