Introduction

Over 80% of business owners enter the market without a formal exit plan, and poor financial preparation is the leading reason deals under $5M fail. The sell-side M&A auction process is a structured, competitive approach a business owner uses (typically with an advisor) to market their company to multiple potential buyers and drive the highest possible offer.

For owners planning an exit — whether for retirement, succession, or strategic reasons — the auction process directly determines how much leverage you hold and how much value you walk away with. Structured auctions consistently yield premiums 5 to 15 percentage points higher than one-on-one negotiated sales, because competitive tension forces buyers to bid their maximum.

This guide covers:

- What the sell-side auction process is and how it works

- Why a structured auction produces stronger outcomes than direct negotiation

- The key stages and timeline from preparation to closing

- How to position your business to attract qualified buyers

Key Takeaways

- The sell-side M&A auction creates competitive tension among buyers to maximize sale price and deal terms

- Four structures exist—broad, limited, targeted auction, and exclusive negotiation—each balancing price against confidentiality differently

- The full process runs 18–26 weeks across four stages: preparation, Round 1 outreach, Round 2 due diligence, and closing negotiations

- Choosing the right auction type depends on your business size, buyer universe, and whether you prioritize maximum price or strict confidentiality

- An experienced advisor manages the process and protects your negotiating leverage throughout

What Is the Sell-Side M&A Auction Process?

The sell-side M&A auction process is a seller-controlled sequence of steps in which the owner and their advisor market the business to multiple prospective buyers, manage competitive bidding, and negotiate toward a closing. Unlike a bilateral negotiation — where a single buyer is engaged from the start — the auction keeps multiple parties competing until a deal closes.

The process is designed to achieve a specific outcome: maximizing sale price and deal terms by creating competitive tension. Rather than accepting a single buyer's opening offer, the auction ensures competition sets the price. When bidders know they must compete to win, they submit stronger offers — often including the full synergy value they expect to capture.

The seller controls three levers that buyers in a bilateral deal never touch:

- Timeline — the seller sets deadlines for each bid round

- Information flow — access to financials and data room is staged and managed

- Buyer selection — the seller chooses who advances and who doesn't

This stands in direct contrast to the buy-side M&A process, where an acquirer drives the agenda — identifying targets, setting terms, and controlling the pace. In an auction, that power shifts entirely to the seller.

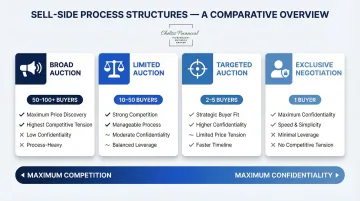

The Four Types of Sell-Side Auction Processes

Sellers have four main ways to structure their deal process, each representing a different point on the spectrum between maximum competition (broad auction) and maximum confidentiality (exclusive negotiation). The right choice depends on company size, buyer universe, and seller priorities.

Broad Auction

A broad auction casts the widest net, reaching out to a large pool of potential buyers—often 50 to 100+ parties—to maximize competitive tension and purchase price. This approach is most appropriate for middle-market businesses under $100M in equity value where the potential buyer universe is large enough to justify it.

Key trade-off: A broad auction drives the highest probability of maximum price and satisfies fiduciary obligations. It is also the hardest to keep confidential and the most resource-intensive for both seller and advisor. Information leakage can cause employees to panic, customers to switch providers, and competitors to poach clients.

Limited Auction

A limited auction targets a curated list of likely buyers, typically 10 to 50 participants, balancing competitive tension with greater confidentiality and less disruption. This structure is better suited for mid-to-large companies with a smaller but well-defined buyer universe.

Narrowing outreach to credible, qualified buyers reduces broad market exposure while maintaining enough competition to drive strong bids.

Key trade-off: Confidentiality improves significantly compared to a broad auction, but the seller accepts slightly less price discovery. This structure works best when the advisor has a strong network of pre-qualified buyers in the relevant industry.

Targeted Auction

The targeted auction involves outreach to a very small, hand-selected group—typically 2 to 5 buyers—considered the most logical acquirers. This is common for larger companies where only a handful of credible buyers exist. For example, when Microsoft acquired LinkedIn, the process was highly targeted due to the limited number of acquirers with the strategic fit and financial capacity to complete the transaction.

Key risk: Limiting outreach means the seller may leave value on the table if an excluded buyer would have offered more. Speed and strategic fit take priority over maximum price discovery.

Exclusive Negotiation

Exclusive negotiation skips the competitive process entirely — the seller engages with a single buyer, often following an unsolicited approach. The advantages include speed, confidentiality, and minimal business disruption. The disadvantages are significant: lowest negotiating leverage, higher risk of underpricing, and no competitive pressure to improve terms.

In practice, sellers who receive an unsolicited offer can choose to negotiate exclusively or use that offer as a trigger to hire an advisor and run a formal auction process. Running a competitive process after an unsolicited approach often yields meaningfully better terms — the presence of other buyers forces the initial suitor to improve their bid.

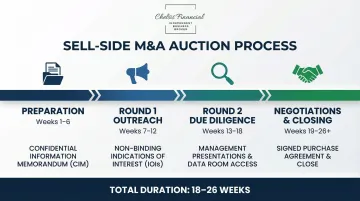

The Sell-Side M&A Auction Timeline, Stage by Stage

A typical structured sell-side auction runs approximately 18 to 26 weeks from preparation to signing, though negotiation complexity, deal size, and due diligence scope can extend this. Delays at any stage can erode buyer interest and deal momentum, so maintaining a disciplined timeline is critical.

Stage 1: Preparation (Weeks 1–6)

The preparation stage is the most critical phase. Sellers who skip or rush this step face longer due diligence, price reductions, and higher deal failure rates. During preparation, the seller assembles an advisory team, defines the sale strategy and auction type, and conducts reverse (sell-side) due diligence to surface issues before buyers find them.

Key deliverables developed during this stage:

- Teaser: A one-page anonymous summary distributed pre-NDA to gauge buyer interest

- Confidential Information Memorandum (CIM): The primary document buyers use to evaluate the business and form their first bids

The CIM is critical. A well-prepared CIM that presents clean financials, a clear growth story, and compelling projections directly affects the quality of first-round bids received. Sellers who engage advisors early for a sell-side Quality of Earnings (QoE) report achieve average EBITDA multiples of 7.4x, compared to 7.0x for those who skip this step.

Stage 2: Round 1 — Initial Buyer Outreach (Weeks 7–12)

In Round 1, the advisor contacts the buyer list, distributes the teaser, exchanges NDAs with interested parties, provides the CIM to qualifying buyers, and collects non-binding Indications of Interest (IOIs). The seller uses these initial bids to narrow the field to the most credible acquirers.

Reputable advisors use anonymous teasers and staged information disclosure to control what each buyer knows and when. NDAs protect seller confidentiality throughout. The advisor's network quality directly affects how many serious IOIs come in—firms with strong buyer relationships, like Chelsis Financial, draw on established connections to generate more competitive first-round bids.

Stage 3: Round 2 — Due Diligence and Final Bids (Weeks 13–18)

Shortlisted buyers gain access to the virtual data room (VDR) for deeper due diligence, attend management presentations, and submit final binding Letters of Intent (LOIs). This is where buyers validate their initial interest and form final pricing positions.

Sellers should be ready for:

- A high volume of data requests from multiple buyers simultaneously

- Site visits and facility walkthroughs

- Detailed management Q&A sessions on financials, operations, and strategy

Being organized and responsive here prevents delays and maintains buyer confidence. Notably, the average time deals spend in a virtual data room has stretched from 6.9 months in 2021 to 10.2 months in 2024 — a reflection of heightened buyer scrutiny that sellers need to anticipate.

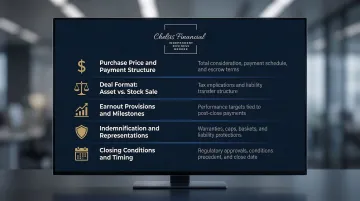

Stage 4: Negotiations and Closing (Weeks 19–26+)

In the final stage, the seller selects a preferred buyer, enters into an exclusivity agreement (typically 30 to 60 days), and negotiates the Definitive Purchase Agreement. Key terms covered include:

- Purchase price and payment structure

- Deal format (asset vs. stock sale)

- Earnout provisions and performance milestones

- Indemnification terms and representations

- Closing conditions and timing

Signing and closing are two distinct events. Signing is when all parties execute the agreement; closing is when funds transfer and ownership formally changes hands. Regulatory approvals or third-party consents may add time between these two milestones, extending the overall timeline beyond 26 weeks in complex transactions.

Key Factors That Shape the Auction Process and Outcome

Several variables directly determine how smoothly an auction runs and how favorable the final terms are. Business owners should address these considerations before and during the process.

Business Size and Buyer Universe

The number of credible potential buyers shapes which auction type is feasible. Smaller companies often have more buyers to approach (making broad auctions viable), while larger companies have a narrower universe of qualified acquirers (making limited or targeted auctions more appropriate).

Quality and Cleanliness of Financials

Buyers scrutinize historical financials intensely. Inconsistencies, restatements, or unclear accounting slow due diligence and reduce buyer confidence. Clean books accelerate the process and support stronger valuations. Poor financials are consistently cited as a leading reason deals under $5M fail to close.

Seller Preparedness

Sellers who address key issues before going to market enter the process in a stronger position and face fewer surprises. Pre-sale preparation typically includes:

- Resolving known legal issues or pending disputes

- Documenting key processes and operational procedures

- Reducing customer concentration risk

Proactive disclosure of any remaining issues before signing an LOI builds buyer trust and prevents unexpected problems from derailing the deal during diligence.

Market Conditions and Timing

Industry M&A activity levels, interest rate environments, and buyer appetite cycles all affect how many bids are received and at what multiples. Elevated interest rates have forced buyers to rely on alternative financing, with seller financing now comprising up to 14% to 15% of total consideration in lower-middle-market deals. Sellers demanding all-cash deals in a tight credit market risk alienating buyers or accepting lower overall valuations.

Advisor Quality and Buyer Network

The advisor's relationships, process management, and ability to run a competitive timeline directly influence both the number of bids and the final price. A well-connected advisor brings a qualified buyer network and manages process momentum — both of which translate directly into better outcomes. For business owners considering a sale, a preliminary valuation assessment is a practical first step to understand where the business stands before engaging a formal process.

Common Mistakes and Misconceptions About the Sell-Side Auction Process

Misconception: Auctions Always Mean the Highest Price

In practice, a poorly managed auction with too many unqualified buyers lowers buyer seriousness and produces weaker bids than a well-run limited auction would. Quality of buyer outreach matters more than quantity.

Misconception: Confidentiality Is Automatically Compromised in an Auction

Experienced advisors use NDAs, anonymous teasers, and staged information disclosure to control what each buyer knows and when. Sellers who avoid running any formal process out of confidentiality fears often leave significant value on the table. Targeted auctions involving fewer than 5 buyers accounted for 31% of take-private deals in 2024— a structure designed precisely to balance price discovery with confidentiality.

Common Error: Poor Timing

Many sellers initiate the process when they are emotionally or financially pressured to sell quickly, which reduces their negotiating leverage. The best outcomes come from sellers who enter the process from a position of strength, with time on their side and a well-prepared business.

The numbers reveal how common this gap is:

- Over 90% of recent sellers were first-time sellers

- More than 80% had no written exit strategy before engaging an advisor

- Both factors directly compress final sale value by limiting the seller's options at the negotiating table

Frequently Asked Questions

What is sell-side M&A?

Sell-side M&A refers to the process from the perspective of the business owner or company selling. It covers preparation, marketing to buyers, negotiating terms, and closing the deal.

What is the difference between buy-side and sell-side M&A?

Sell-side M&A is managed by the seller and their advisors with the goal of maximizing sale value, while buy-side M&A is led by the acquirer seeking to identify, evaluate, and purchase a target at the best possible terms for the buyer. Every transaction involves both sides simultaneously, though each operates with opposing objectives.

What are the 4 types of M&A?

The four structural types of mergers and acquisitions are:

- Horizontal — between direct competitors in the same market

- Vertical — between companies in the same supply chain

- Conglomerate — between unrelated businesses in different industries

- Congeneric/Concentric — between companies in related but non-competing industries

How long does the sell-side M&A auction process typically take?

A structured auction typically runs 18–26 weeks from preparation to signing across four stages: preparation, Round 1 outreach, Round 2 due diligence, and negotiations. Deal complexity, regulatory requirements, and negotiation dynamics can extend the timeline beyond six months.

What is a broad auction in M&A?

A broad auction is the most competitive sell-side process structure, in which the seller's advisor reaches out to a large pool of potential buyers (often 50+) to maximize competitive tension and achieve the highest possible purchase price. Middle-market businesses with diverse buyer appeal — across strategic and financial acquirers — typically benefit most from this structure.