Introduction

Many business acquisitions stall not because of bad fundamentals, but because of a financing gap the bank won't bridge. Seller financing fills that gap: the seller holds a promissory note and receives regular payments, with interest, directly from the buyer instead of requiring full payment at closing. For both sides of the table, it can make or break deals that would otherwise fall apart.

Despite how common seller financing is in M&A conversations, most parties enter negotiations without a clear understanding of how terms are structured or what obligations each side carries. According to recent market data, 62.3% of buyers consider seller financing essential to their acquisition strategy, yet only 22.8% of sellers plan to offer it.

That expectation gap derails otherwise viable transactions more often than it should.

Key Takeaways

- Seller financing allows the seller to extend a loan covering part of the purchase price, repaid with interest via a promissory note

- 48% of private business sales involve seller financing, making it a mainstream deal structure

- Buyers gain easier qualification, preserved cash, and faster closings

- Sellers access a broader buyer pool, potential price premiums, and tax deferral benefits

- Typical terms range from 10–25% seller-financed, with 5–7 year repayment periods and interest rates of 6–10%

- Works best with demonstrable cash flow, mutual trust, and a genuine funding gap—not for distressed sales

What Is Seller Financing in a Business Acquisition?

Seller financing (also called owner financing or a seller note) is a private lending arrangement where the seller defers a portion of the sale price, collecting it over time through scheduled payments from the buyer. Unlike traditional financing, no third-party lender is involved — the seller and buyer negotiate terms directly. That flexibility speeds up deals, but it also means both parties bear full responsibility for structuring the agreement soundly. A poorly drafted arrangement can leave the seller exposed to default with limited recourse.

The promissory note formalizes the agreement and governs the entire relationship until the balance is paid. A complete note covers:

- Principal amount financed

- Interest rate and compounding method

- Repayment schedule (monthly, quarterly, balloon)

- Collateral securing the debt

- Consequences of default and cure periods

Most seller notes in small to mid-market acquisitions run three to seven years, with interest rates typically ranging from 6% to 10%.

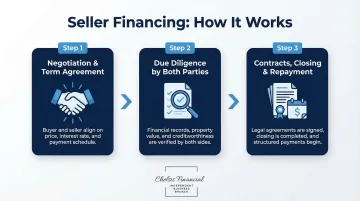

How Seller Financing Works: A Step-by-Step Breakdown

The seller financing process follows a clear sequence: buyer and seller agree on terms, execute legal agreements, and close with a down payment. From there, the buyer repays the seller note over the agreed term, with both parties carrying obligations until the loan is satisfied.

Step 1: Negotiation and Term Agreement

Once both parties express interest, the seller typically requests the buyer's financial documents, credit history, and business plan to assess creditworthiness. The process is similar to what a bank would require, but with considerably more room to negotiate terms directly.

Key negotiation points include:

- Percentage of purchase price to be financed

- Interest rate and repayment term

- Down payment amount

- Collateral requirements

- Personal guarantee provisions

Chelsis Financial helps sellers pre-screen and vet qualified buyers before term negotiations begin, reducing the risk of deals falling apart late in the process.

Step 2: Due Diligence by Both Parties

Sellers verify:

- Buyer's credit score and financial statements

- Relevant industry experience

- Ability to sustain loan payments from projected cash flow

- Business plan viability

Buyers verify:

- Seller's financial records (profit and loss statements, tax returns, balance sheet)

- Existing liabilities and encumbrances

- Whether the business generates enough income to fund operations and debt repayment simultaneously

- Accuracy of represented revenue and cash flow

Step 3: Contracts, Closing, and Repayment

Closing requires two key documents:

- Purchase agreement — defines the parties, purchase price, and all deal terms

- Promissory note — governs repayment terms and default consequences

Once both are signed, the buyer takes ownership, makes the down payment, and begins scheduled payments. The seller retains a security interest in the business assets until the note is paid in full.

Key Terms and Structure of a Seller Financing Agreement

Loan Amount

Sellers typically finance between 10% and 25% of the total asking price in most transactions. In rare cases where seller financing is the primary funding source, sellers may finance up to 60% of the purchase price with a substantial down payment. The percentage financed depends on buyer creditworthiness, business cash flow stability, and whether the seller note is combined with bank or SBA financing.

Interest Rate and Term Length

Interest rates generally range from 6–10%, and repayment terms typically run 5–7 years. These rates compare favorably to SBA 7(a) loans, which carry variable rates capped at the base rate plus 3.0% to 6.5% depending on loan size. Rates are negotiated based on buyer risk profile, deal size, and current market conditions.

Down Payment

Buyer down payments typically range from 10–25% of the total purchase price (not the loan amount). A higher down payment reduces the seller's risk and can improve the interest rate offered. When combined with SBA financing, buyers must meet a minimum 10% equity injection requirement.

Collateral and Personal Guarantee

The seller commonly requires a lien on business assets as collateral, subordinate to any senior bank or SBA financing. Many sellers also require a personal guarantee from the buyer, meaning the seller can pursue the buyer's personal assets in the event of default.

Balloon Payments and Special Clauses

A balloon payment is a lump-sum amount due at the end of the loan term, covering any remaining principal balance. Sellers use them to maintain higher monthly cash flow during the repayment period while ensuring full principal recovery by a fixed date.

Three additional clauses commonly appear in seller notes:

- Prepayment penalties — fees charged if the buyer pays off the note early

- Subordination clauses — required when combining with SBA financing; the seller note ranks below the senior lender's claim

- Full standby provisions — under SBA deals, the seller note may be frozen (no payments made) for the entire life of the SBA loan

Pros and Cons of Seller Financing: Buyers vs. Sellers

For Buyers: Benefits

Easier qualification and faster closing: Sellers evaluate buyers using their own criteria rather than rigid bank underwriting standards. This makes financing accessible to first-time buyers or those with strong business acumen but imperfect credit history. Deals also close faster without institutional approval queues—often 30–60 days faster than bank-financed transactions.

Preserved liquidity: The buyer retains more working capital for post-acquisition operations, which is critical during the transition period. A seller willing to carry a note also signals genuine confidence in the business's cash flow under new ownership—giving buyers more confidence in the deal.

For Buyers: Risks and Drawbacks

Higher overall purchase price and balloon obligations: Seller-financed deals often carry a total price 10–15% higher than straight cash sales to compensate the seller for assuming lending risk. Balloon payments at term end can create refinancing pressure if the business underperforms, forcing buyers to secure alternative financing or risk default.

For Sellers: Benefits

Expanded buyer pool and higher sale price: Financing a portion of the deal opens acquisition opportunities to buyers who cannot secure full traditional financing, increasing competition and potentially driving up the final price. Research shows seller-financed deals command an average 15.84% price premium compared to all-cash transactions.

The interest earned on the note also generates income beyond the principal—an ongoing return that straight cash sales don't provide.

Tax deferral through installment sale treatment: Under IRS installment sale rules (IRC Section 453), sellers who receive payments over time may only owe taxes on the portion of the gain received each year, potentially reducing annual tax liability.

Note that depreciation recapture must still be reported as ordinary income in the year of sale. Consult a tax professional to structure this correctly for your situation.

For Sellers: Risks and Drawbacks

Carrying a note introduces two risks sellers should weigh carefully:

- Default exposure — if the buyer stops paying, reclaiming the business through collections or foreclosure can take months or years and is rarely cheap

- Illiquid capital — funds tied up in the note aren't available for retirement, estate settlement, or other investments until the term ends

Neither risk is disqualifying, but both are worth stress-testing before agreeing to carry a large portion of the deal.

When Seller Financing Makes Sense — and When It Doesn't

Scenarios Where It Fits Well

- Funding gap exists: A qualified buyer faces a financing shortfall that SBA or bank financing can't bridge, typically 10-30% of the purchase price

- Seller motivation and trust: The seller is motivated to close quickly and trusts the buyer's ability to run the business based on experience and financial review

- Demonstrable cash flow: The business has consistent, verifiable cash flow that comfortably supports ongoing debt payments plus operational expenses

Scenarios Where It Is a Poor Fit

- Immediate capital needs: The seller needs full sale proceeds immediately for estate settlement, retirement income requirements, or debt obligations

- Buyer creditworthiness concerns: The buyer's financial profile raises genuine repayment concerns, including poor credit history, insufficient liquidity, or lack of relevant experience

- Unreliable cash flow: The business lacks reliable cash flow history, making it difficult to predict whether the buyer can service the note

Combining Seller Financing with Other Funding Methods

Seller financing rarely covers the full purchase price on its own. Most buyers layer it with one or more of the following:

- SBA 7(a) loans — the most common pairing for acquisitions up to $5M

- Traditional bank loans — used when the buyer has strong collateral and credit history

- Retirement fund rollovers (ROBS) — allows buyers to deploy 401(k) funds without early withdrawal penalties

When combining with an SBA 7(a) loan, the seller note faces strict limits. Under current SBA SOP 50 10 8 guidelines, seller notes can only cover up to 50% of the buyer's required 10% equity injection — meaning 5% of total project costs — and must remain on full standby with no principal or interest payments for the life of the SBA loan.

Common Misconceptions About Seller Financing

Three misconceptions consistently lead buyers and sellers to leave value on the table. Here's what the data and deal experience actually show.

"Seller financing means the business couldn't attract real buyers"

Seller financing is a deliberate strategic tool used in the majority of small business transactions. A seller offering financing typically signals confidence in the business's performance, not desperation. With 48% of private business sales involving seller notes, it has become a mainstream deal structure that sophisticated buyers and sellers use to optimize transaction value and terms.

"Terms are non-negotiable once proposed"

Unlike institutional lenders, seller financing terms are entirely negotiable. Interest rate, repayment schedule, collateral requirements, and the financed percentage can all shift based on mutual agreement and due diligence findings. Every element stays open until both parties sign.

"Seller financing eliminates the need for formal due diligence"

Both parties must still conduct thorough financial and legal review. The buyer needs to verify true cash flow and business value; the seller needs to assess the buyer's creditworthiness and capacity to repay.

Skipping due diligence raises default risk for the seller and overpayment risk for the buyer. Professional advisors should review financial statements, tax returns, and legal documents regardless of the financing structure.

Frequently Asked Questions

What are typical terms for seller financing in a business acquisition?

Standard seller financing terms include 10–25% of the purchase price financed, interest rates of 6–10%, repayment terms of 5–7 years, and down payments of 10–25% of the total purchase price. All terms are negotiable between buyer and seller based on the specific transaction dynamics and risk profile.

How do you structure a seller-financed business acquisition?

Structure begins with agreeing on financing terms and down payment, then executing a purchase agreement and promissory note that define collateral and default consequences. The repayment schedule should align with the business's expected cash flow so the buyer can meet obligations without depleting working capital.

Is seller financing a good idea for the buyer?

Seller financing can be advantageous for buyers who face financing gaps, want faster closings, or need to preserve liquidity for post-acquisition operations. However, buyers should weigh the potentially higher purchase price (typically 10-15% premium) and balloon payment risks before committing. The arrangement works best when the business has strong, predictable cash flow.

Is seller financing a good idea for the seller?

Seller financing expands the buyer pool and can increase the sale price by an average of 15.84%, with installment-based tax treatment that defers capital gains recognition. The tradeoff is default risk and capital tied up over the note's term — it works best for sellers who don't need immediate access to full proceeds.

Does seller financing help avoid or defer capital gains tax on a business sale?

Under IRS installment sale rules (IRC Section 453), sellers defer recognizing capital gains to the years payments are received, which can reduce annual tax burden. Note that depreciation recapture must still be reported as ordinary income in the year of sale, regardless of payment timing.

What is the three-and-12 rule in seller financing?

The "3-and-12 rule" applies exclusively to residential real estate under Dodd-Frank — it allows individuals to seller-finance three or fewer residential properties in a 12-month period without mortgage loan originator licensing. It has no application to commercial business acquisitions, asset sales, or stock sales.