What Is Strategic Exit Planning (and Why Most Business Owners Get It Wrong)

For most business owners, the company they built is their retirement plan. Every decision, sacrifice, and reinvested dollar has been tied to that single asset — which makes the exit often the single largest financial transaction of their lives.

Yet according to the Exit Planning Institute, only 32% of business owners have a documented exit plan. That means the majority are running toward retirement with no roadmap for the most important financial transaction of their lives.

Exit planning isn't simply "selling the business." It's a coordinated strategy that integrates business readiness, personal financial security, legacy goals, and ownership transition, and it works best when started years before any transaction begins.

Getting that strategy right is exactly what this guide addresses. Here's what you'll find inside:

- Which exit strategy fits your goals and timeline

- How to prepare your business for a higher valuation

- A phased roadmap from planning to closing

- Financial readiness benchmarks to hit before you list

- The planning mistakes that erode sale value

Key Takeaways

- Exit planning is a multi-year process — EPI recommends starting 3–5 years before your intended transition at minimum

- There is no single best exit path; the right strategy depends on your financial goals, timeline, and personal priorities post-exit

- Business value is built before you go to market — buyers pay for transferable, owner-independent cash flow

- Your sale price is not a guaranteed retirement fund — only 20–30% of businesses listed for sale actually close

- Working with a specialized business broker, your CPA, and legal counsel isn't optional; it's how you protect your outcome

Why Exit Planning Cannot Wait

The Numbers Behind the Urgency

Most owners aren't ready. EPI research shows 53% of business owners lack a written, formal transition plan — and nearly half of all exits aren't voluntary.

The Exit Planning Institute identifies five triggers — death, disability, divorce, disagreement, and distress — that force roughly 50% of all owner exits before the owner is prepared. Together, these five triggers are the leading cause of unplanned ownership transfers — not outliers, but a pattern that plays out regularly across small and mid-market businesses.

When an exit is forced, options shrink fast. There's no time to clean up financials, reduce owner dependence, or position the business attractively. The result is typically a discounted sale price, a thin buyer pool — or no transaction at all.

The Compounding Cost of Waiting

Forced exits are the most dramatic consequence of poor timing, but delay costs owners even when nothing goes wrong. Every year without a plan removes options:

- Fewer viable exit strategies — some paths (ESOPs, family succession, MBOs) require years of setup

- Less time to build business value — transferable systems, leadership depth, and financial documentation take time to develop

- Greater financial vulnerability — if 80% of an owner's wealth is tied up in the business (per EPI research), an unplanned exit can devastate retirement security

Owners who start early don't do so because they want out sooner. They do it because having a plan gives them the leverage to choose their timing, their buyer, and their terms.

Types of Exit Strategies: Which Path Fits Your Goals?

No two exits look alike. Your timeline, post-sale involvement, cultural legacy, and liquidity needs all shape which path actually fits — and the wrong choice can cost you more than money.

Third-Party Sale

Selling to an external buyer — whether a strategic acquirer or financial buyer like a private equity firm — generally delivers the highest upfront liquidity with a defined transaction timeline.

PE buyers represented roughly 20% of lower-middle-market acquisitions in Q4 2025, per IBBA/M&A Source data. They move with discipline, but their focus on short-term profitability and add-on integration often means real operational or cultural changes post-sale.

Strategic buyers may pay a premium for synergies. Either way, a third-party sale usually means a clean break — which suits owners prioritizing liquidity over legacy continuity.

Management Buyout (MBO) or Key Employee Sale

An MBO transfers ownership to trusted insiders who already know the business. Culture stays intact, customer relationships are protected, and the transition is smoother operationally than most external deals.

The trade-off: the owner usually provides seller financing, which spreads proceeds over time and introduces some payment risk. The exit timeline is longer, and the sale price may be lower than what an external buyer would pay. For owners who care deeply about what happens after they leave, that trade-off is often worth it.

Employee Stock Ownership Plan (ESOP)

Where an MBO puts ownership in the hands of a few key insiders, an ESOP distributes it broadly — transferring ownership to employees through a trust structure. The tax advantages can be substantial — under Section 1042 of the U.S. tax code, qualifying sellers can defer capital gains if the ESOP owns at least 30% of the company post-transaction.

But ESOPs aren't simple. NCEO data suggests installation costs start around $125,000, and the structure works best for businesses with stable cash flow, strong internal leadership, and at least 15–20 employees. As of 2023, there were roughly 6,609 ESOPs across the U.S. — viable but not a default option.

Family Succession

Passing the business to a family member preserves legacy in the most direct way. It also requires the most planning. Successor grooming takes five or more years, and unresolved family dynamics — unclear roles, competing expectations, governance gaps — can derail even well-intentioned transitions.

Clear documentation, defined timelines, and outside governance — an advisory board, for instance — are often non-negotiable for family succession to work.

Orderly Wind-Down

When a business is highly owner-dependent and a sale isn't realistic, a planned wind-down is a legitimate exit. Done deliberately — honoring contracts, transitioning customers, retaining key employees as long as viable — it recovers far more residual value than a forced closure. Owners who plan the wind-down early, rather than letting the business simply fade, preserve more value and exit with more control.

How to Prepare Your Business for a Successful Sale

Buyers purchase future cash flows, not past effort. What that means practically: a business must demonstrate consistent, transferable performance that doesn't depend on the owner showing up every day.

Business Valuation: Know Your Number Before You Go to Market

Getting a formal valuation early does several things at once — it sets realistic price expectations, identifies the gap between current value and retirement needs, and informs tax and estate planning. Owners who skip this step often price themselves out of deals or accept offers that don't actually fund their retirement.

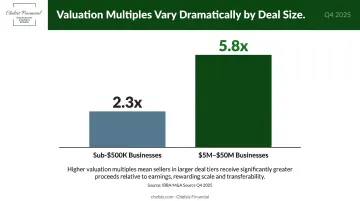

Valuation benchmarks vary significantly by size. IBBA/M&A Source Q4 2025 data shows $5M–$50M deals trading at 5.8x EBITDA, while sub-$500K businesses average closer to 2.3x. Understanding where your business falls in that range can shift your planning horizon by years.

Chelsis Financial offers a Complimentary Assessment of Value for owners who want a realistic baseline before committing to a sale process — covering financial performance, market comparables, and industry benchmarks to establish a defensible asking price.

Reducing Owner Dependence

Owner dependence is one of the most common reasons buyers discount — or walk away from — otherwise attractive businesses. Steps that make a real difference:

- Document key processes so operations don't live in one person's head

- Build leadership depth so client relationships survive the owner's departure

- Reduce customer concentration — a single customer at 30%+ of revenue is a red flag in every due diligence process

- Consider bringing in a COO or CFO if scale justifies it, or a professional manager if it doesn't

Financial Clarity and Clean Records

Buyers and their lenders want at least three years of organized financial history. The SBA requires it for acquisition financing. That means:

- Separating personal expenses from business accounts

- Normalizing earnings to reflect true business performance

- Working with your accountant to present an accurate, defensible picture of profitability

Disorganized or inconsistent financials are the most common reason deals stall — more frequent than any dramatic operational failure.

Operational Documentation and Risk Management

Clean financials buy credibility; clean operations protect it. Before going to market, address anything that could surface in due diligence and reduce your price:

- Written operating procedures for key functions

- Current contracts, leases, and IP protections

- Outstanding compliance, tax, or cybersecurity issues resolved or disclosed

Proactive disclosure keeps deals moving — surprises at the due diligence stage are far more damaging than the issues themselves.

A Step-by-Step Exit Planning Roadmap

Successful exits are built over years, not assembled in weeks — and each phase demands a different focus.

Phase 1 (3–5 Years Out): Define Goals and Build Value

Start here to preserve the most flexibility on buyer type, deal structure, and tax strategy:

- Clarify personal financial needs — what do you actually need from this sale to fund your retirement?

- Set a target valuation — and identify the gap between where you are and where you need to be

- Assemble your advisory team — financial advisor, CPA, attorney, and business broker

- Start implementing value-building improvements — leadership development, systems documentation, customer diversification

Starting here keeps strategic alternatives open — whether that's a third-party sale, management buyout, or phased ownership transfer.

Phase 2 (1–3 Years Out): Strengthen, Document, and Explore

- Strengthen and normalize financials across at least three fiscal years

- Reduce owner dependence — management transitions take time

- Get a formal business valuation

- Begin exploring which exit strategy aligns with personal and financial goals

- Address any operational, legal, or compliance gaps

Phase 3 (6–18 Months Out): Execute the Transition

- Formally engage a business broker to confidentially market the business

- Qualify buyers before any sensitive information is shared

- Negotiate deal structure — not just price

- Finalize tax strategy with legal and financial counsel

- Manage leadership transition and operational handoff planning

Understanding Deal Structure vs. Sale Price

A high headline number means very little without understanding how it's paid. Most deals include:

| Component | What It Means for the Seller |

|---|---|

| Upfront cash | Received at closing; cleanest form of proceeds |

| Seller financing | Paid over time; introduces payment risk |

| Earn-outs | Tied to future performance; requires staying involved |

| Retained equity | Participation in future upside; requires trust in buyer |

Chelsis Financial evaluates deal structure alongside price from the first conversation — because a lower offer paid entirely in upfront cash can net more than a higher offer loaded with earn-outs and seller financing.

Financial Readiness: Don't Depend Entirely on the Sale Price

Consider this: only 20–30% of businesses that go to market actually sell. Building a retirement plan entirely around a transaction with a 70–80% failure rate is a significant financial risk.

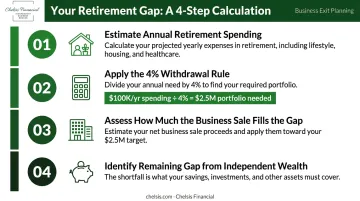

The Retirement Gap Calculation

Owners should work through this math well before listing:

- Estimate annual retirement spending — what lifestyle do you actually want?

- Apply the 4% withdrawal guideline (from Bengen's foundational research) to back into a required portfolio size — e.g., $100K/year in spending requires roughly $2.5M in investable assets

- Assess how much of that gap the business sale realistically fills at a conservative valuation

- Identify the remaining gap that must come from independent wealth built during the business's operating years

That gap calculation often reveals an uncomfortable reality — which is why building wealth outside the business matters as much as building the business itself.

Diversifying Wealth Outside the Business

If 80% of your net worth is tied to a single illiquid asset, your financial security is fragile. Building wealth outside the business throughout ownership — in real estate, equity accounts, retirement vehicles — reduces your dependence on a single transaction going perfectly.

The goal: the business sale becomes a meaningful financial event, not the defining one. Owners who reach their exit with diversified wealth carry more negotiating flexibility, more patience in deal selection, and more resilience when deals fall through.

Common Exit Planning Mistakes to Avoid

Starting Too Late

Most owners wait until they're emotionally ready to leave before thinking about exit planning. By that point, years of value-building time are gone, and many exit strategies are no longer viable. The optimal starting point is 3–5 years out — earlier if the business has structural issues that need addressing.

Overvaluing the Business

Axial's 2026 lower-middle-market outlook identifies valuation expectation gaps as the leading cause of failed deals, cited by 28.3% of respondents. Diligence findings came second at 24.5%.

Owners who price based on emotional attachment rather than market comparables spend months on market, attract fewer serious buyers, and often end up accepting less than they would have with realistic initial pricing. A formal valuation from an independent professional gives you a defensible number — one that opens serious conversations rather than scaring buyers off before negotiations begin.

Going It Alone

Exit planning touches multiple disciplines at once:

- Tax law and deal structure

- Business valuation

- Legal documentation and closing mechanics

- Personal financial planning post-sale

- Buyer negotiation and process management

No single advisor covers all of these. Owners who rely on a generalist accountant or try to manage the process themselves frequently leave money on the table or face expensive surprises at closing.

A coordinated team — a financial advisor, CPA, attorney, and specialized business broker — prevents those gaps from becoming costly. Chelsis Financial works with Midwest business owners through each stage of this process, from initial valuation through closing, with direct access to a network of qualified buyers across manufacturing, distribution, service, and technology sectors.

Frequently Asked Questions

What are the 4 pillars of retirement planning?

The four pillars are income planning (reliable cash flow in retirement), investment management (growing and protecting assets), tax planning (minimizing tax burden), and estate planning (distributing wealth per the owner's wishes). For business owners, a successful exit strategy must integrate with all four simultaneously.

When should a business owner start exit planning?

Begin at least 3–5 years before your intended transition. Earlier is better — the more lead time you have, the more exit options are viable and the more business value you can build before going to market.

What is the difference between exit planning and succession planning?

Succession planning focuses on who will lead or own the business after the current owner. Exit planning is broader — it encompasses valuation, deal structure, tax optimization, retirement income planning, and the owner's personal goals post-exit.

How long does it typically take to sell a business?

Most business sales take 6–18 months from formally engaging a broker to closing, depending on business size, industry, and market conditions. That timeline doesn't include preparation — which is why planning must start well before the owner is ready to list.

How do I know what my business is worth?

Business value is determined through a valuation process considering financial performance, industry multiples, growth trajectory, customer concentration, and operational independence from the owner. Get a professional valuation well before initiating a sale — not after.

What happens if a deal falls through?

Roughly 1 in 3 signed LOIs don't reach closing, so contingency planning matters. Maintain strong operations, keep financials current, and work with a broker who has access to multiple qualified buyers — sellers who've done the preparation work can re-engage the market quickly.