The stakes are real. Employees who learn the business is for sale may start updating their résumés. Customers might slow renewals or test alternative suppliers. A competitor posing as a buyer can extract pricing and client data without any genuine acquisition intent. Each of these outcomes can damage the very business a buyer is evaluating — and every one of them can happen months before a letter of intent is signed.

BizBuySell reported 9,586 closed small-business transactions in 2025, with a median time to close of 170 days. That's nearly six months of sustained confidentiality management — not a one-time document signing event.

This guide covers the tools that protect a confidential sale, how to manage disclosure at each stage of the process, and how to handle the people most affected when the stakes are highest.

Key Takeaways

- Confidentiality in M&A requires a structured, staged process — not just an NDA

- Blind teasers, buyer screening, NDAs, and virtual data rooms only work when used together

- Most confidentiality failures come from weak process control, not formal legal disputes

- Protecting the business and keeping qualified buyers moving forward aren't mutually exclusive

- A business broker manages the full confidential process — sellers never engage the market directly

Why Confidentiality Matters in a Business Sale

Premature disclosure doesn't arrive as a legal notice. It shows up in your P&L.

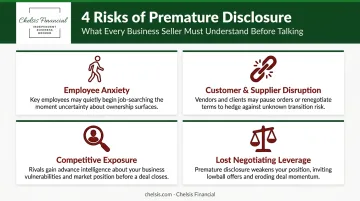

There are four core risks every seller faces once word gets out:

- Employee anxiety: Key staff — the exact people a buyer is paying for — may leave before closing rather than wait out uncertainty about their jobs and compensation

- Customer and supplier disruption: Customers may slow purchasing decisions or test alternatives; suppliers may tighten payment terms or flag lease assignment concerns before the deal closes

- Competitive exposure: Pricing structures, customer concentration, and operational margins shared too early can benefit a competitor whether or not they ever intend to buy

- Lost negotiating leverage: A buyer who senses internal disruption — turnover, nervous management, distracted ownership — has justification to reprice or add deal protections

Project Equity estimates 2.3 million small businesses are owned by aging baby boomers, employing 24.7 million people, and fewer than 15% are expected to pass to family members. That means most will go to market. With the median sale taking 170 days to close, confidentiality isn't a single moment — it's a discipline that has to hold across months.

Sellers frequently focus on external secrecy and overlook the internal side: controlling which parties — staff, vendors, advisors — have access to sale-related information, and exactly when they get it.

The Core Tools for Protecting M&A Confidentiality

No single tool is sufficient on its own. The following four work together as a system.

The Blind Teaser

A blind teaser is a one-page anonymous summary describing the business by category, general region, revenue range, and business model — without naming the company, its location, its branding, or any identifying operational detail.

An effective teaser attracts qualified interest while ensuring that a competitor, vendor, or current employee couldn't identify the seller from reading it. It's the first filter in the process, not a marketing brochure.

The Non-Disclosure Agreement

An NDA creates legal accountability, but only if it's structured correctly. A well-drafted M&A NDA should include:

- A broad definition of confidential information, covering business data, transaction terms, and the existence of negotiations themselves

- Restrictions on use — limiting the buyer to evaluating a potential transaction only

- A defined list of permitted representatives (attorneys, lenders, advisors) who may access information

- Non-solicitation provisions covering employees and customers, typically for 12 to 24 months

- Requirements to return or destroy materials if negotiations end

- Defined duration, with trade-secret obligations surviving until the information loses that status

That said, an NDA creates a legal remedy after a breach — not before. It cannot undo the operational damage that may already have occurred: the employee who left, the customer who paused their contract.

Virtual Data Rooms

A virtual data room (VDR) is a secure online environment for sharing due diligence documents. For sellers managing a 170-day process with multiple potential buyers, a VDR provides controls that email and shared drives cannot offer:

- Role-based access by buyer, stage, and document category

- Encryption and restrictions on printing or downloading

- Access logs showing exactly who viewed what and when

- The ability to revoke access immediately if a buyer withdraws

The audit trail alone is valuable. If a confidentiality concern arises post-process, access logs establish what was actually viewed and by whom.

A Business Broker as Process Manager

The most practical confidentiality tool isn't a document — it's an intermediary. A qualified broker builds anonymous listings, manages outreach through pre-screened contacts, and runs buyer qualification before any information is released. This creates a controlled buffer between the seller and the market.

Chelsis Financial manages this entire process — from building the blind teaser through final buyer qualification — so business owners never have to expose the company's identity directly to the market.

Before an NDA is even presented, serious brokers require prospective buyers to confirm:

- Acquisition intent and target timeline

- Relevant industry or operational experience

- Demonstrated financial capacity

This pre-qualification step filters out unqualified interest before any sensitive disclosure begins.

Managing Confidentiality at Each Stage of the Sale Process

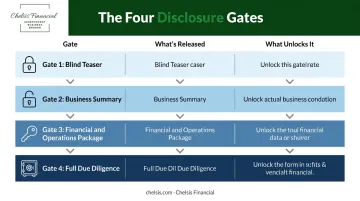

The Four Disclosure Gates

Information should move in layers, unlocked only as a buyer demonstrates greater commitment and qualification.

| Gate | What's Released | What Unlocks It |

|---|---|---|

| 1 — Blind Teaser | Category, region, revenue range, business model | Responding to marketing outreach |

| 2 — Business Summary | Industry detail, financial overview, operational highlights | Signed NDA |

| 3 — Financial & Operations Package | 3-year financials, EBITDA detail, key contracts overview | Buyer screening confirms financial capacity and intent |

| 4 — Full Due Diligence | Tax returns, named contracts, employee data, customer schedules | Letter of Intent signed |

This staged structure protects the seller at every point without creating unnecessary friction for genuinely qualified buyers. Knowing which details to hold back — and when — is just as important as understanding when to release them.

What to Withhold at Each Stage

- Withhold company name, exact location, and specific customer names during early marketing

- Keep named customer accounts, individual employee compensation, and full unredacted contracts off the table until after LOI

- Aggregate or redact personally identifiable employee data throughout the entire process

Managing Internal Confidentiality

The internal side is where many sellers underestimate risk. Practical controls include:

- Limiting knowledge of the sale to the owner and a small, necessary group of advisors

- Designating one person to approve all information releases

- Using neutral subject lines and file names for sale-related communications

- Keeping sale materials off shared company drives and out of shared calendar invites

Sellers working with Chelsis Financial can request a complimentary Assessment of Value as a confidential first step. The assessment reviews three to four years of financial statements and evaluates tangible assets, establishing a realistic price range and sale-readiness picture before any buyer interaction begins.

Handling Employees, Customers, and Competitors During the Sale

Employees: Timing Is Everything

Most employees should not know the business is for sale during early marketing. The people a buyer values most — top performers, managers with deep client relationships — are also the most mobile. Uncertainty about ownership changes triggers exactly the kind of voluntary departures that erode deal value.

Key managers typically need to be involved only when their participation is essential for due diligence or transition planning. When that conversation happens, it should be direct: explain their role in the process, what it means for their position, and why their continued presence matters to both the current owner and the incoming buyer.

Customers and Suppliers

Delay naming accounts or sharing contract details until a buyer has demonstrated serious intent. Use anonymized revenue concentration schedules and customer summaries in early diligence rather than named client files.

Early awareness among suppliers and landlords creates specific deal risks:

- A landlord who learns a lease assignment is coming may renegotiate terms before closing

- A supplier uncertain about future ownership may tighten payment requirements or shorten credit windows

Competitor Buyers: A Higher-Risk Category

A competitor pursuing acquisition may use the diligence process to gather competitive intelligence — whether intentionally or not. The FTC has specifically flagged that pre-merger due diligence between competitors can create antitrust risk and recommends safeguards such as third-party consultants or clean teams when competitively sensitive information must be exchanged.

Practical steps when a competitor proceeds as a legitimate buyer:

- Apply a stricter NDA with more explicit use restrictions

- Use staggered disclosure — antitrust-sensitive information (pricing, customer data, supplier terms) released last

- Consider a clean-team arrangement where only designated advisors access the most sensitive materials

- Screen carefully during qualification: ask about their acquisition rationale and decision timeline

Personally Identifiable Employee Data

Employee Social Security numbers, direct-deposit records, and other PII should be excluded or redacted from buyer documents throughout diligence. Unnecessary disclosure creates breach-notification exposure under state law — separate from and in addition to the confidentiality obligations in your NDA.

Before sharing any personnel records, confirm your obligations under applicable state law. Practical defaults to apply regardless of jurisdiction:

- Redact SSNs, banking details, and benefit enrollment data from all buyer-facing documents

- Provide headcount and compensation summaries in aggregate form during early diligence

- Reserve individual employee records for post-LOI, with legal counsel reviewing scope before release

What Happens When Confidentiality Is Breached

Operational Consequences

The immediate effects hit the business itself:

- Employees who hear about a sale through the rumor mill often leave before closing, taking with them the human capital a buyer was counting on

- Customers may slow renewals, test alternatives, or ask uncomfortable questions that surface during the buyer's own diligence

- Suppliers may tighten payment terms or become less flexible on contract assignments

A 2025 case study from IBG Fox & Fin documented a situation where a competitor refused to sign an NDA and obtained sensitive information anyway. The competitor poached key sales staff and misled customers about the company's stability. The deal collapsed, and the business spent years recovering.

Deal-Level Consequences

A buyer who learns that information has been circulating loosely rarely shrugs it off. Loose process discipline reads as a management quality signal. Common responses include:

- Requesting broader or deeper diligence to assess actual damage

- Proposing a price reduction to account for perceived operational disruption

- Adding reps, warranties, or indemnification protections to the purchase agreement

- Withdrawing entirely

Legal Remedies: What to Expect

When deal consequences materialize, sellers naturally look to their NDA for relief. NDAs do provide legal recourse — sellers can pursue injunctive relief and financial damages for losses caused by a breach. Non-solicitation provisions covering employees and customers typically run 12 to 24 months and can be enforced through the courts.

Enforcement, however, is slow, expensive, and rarely adequate to reverse the practical damage already done. By the time an injunction is granted, the employee has left. The customer has already shifted purchasing behavior.

Prevention through staged disclosure and process discipline is more effective than any legal remedy.

Frequently Asked Questions

How do I sell my business discreetly?

Use a blind marketing summary that describes the business without identifying it, work with an experienced business broker to manage buyer outreach through a pre-screened network, and require a signed NDA before sharing any identifying details. Information should only reach buyers who have been qualified on financial capacity and acquisition intent.

What should be included in a business sale NDA?

A well-structured NDA should address:

- Definition of confidential information

- Restrictions limiting use to transaction evaluation only

- Prohibition on disclosing the existence of the sale

- Requirements to return or destroy materials

- Non-solicitation provisions for employees and customers

- A defined duration

Trade-secret obligations typically survive longer than general confidentiality terms.

When should employees be told the business is being sold?

Most employees should not be informed until a buyer is firmly committed and the deal is near closing. Key managers essential for due diligence or transition planning may need to be involved earlier, but only on a need-to-know basis and with a clear conversation about their role and job security.

What happens if confidentiality is breached during an M&A deal?

A breach can trigger employee departures, customer disruption, supplier term changes, and buyer repricing or withdrawal. Legal remedies exist under the NDA — injunctive relief and financial damages — but the practical business damage typically occurs before enforcement becomes possible.

Do I need a business broker to keep my sale confidential?

A broker isn't legally required, but they are one of the most effective confidentiality safeguards available. They create anonymous listings, screen buyers before any information is released, and act as a buffer between the seller and the open market. Chelsis Financial handles this process end-to-end — from blind teaser to buyer qualification.

What information should not be shared with buyers during early due diligence?

Withhold the following until after an NDA is signed and a letter of intent is in place:

- Named customer accounts

- Individual employee compensation records

- Personally identifiable data

- Proprietary pricing details

- Full unredacted contracts